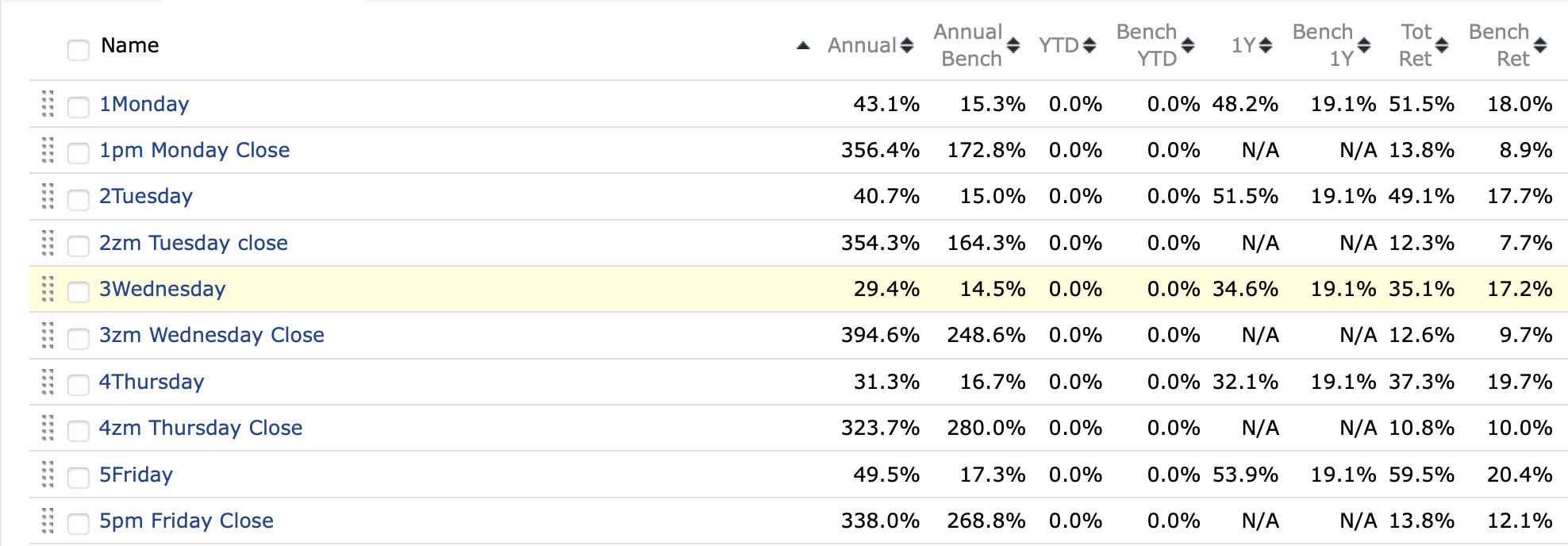

All,

Here are all of my stock ports with no survivorship bias meaning I did not start any other stock ports during this period (I do an ETF port that I have not included for diversity). I have been trading during the day. I added a port at the close for liquidity reasons as the close has the higherst trading volume of the day (generally) with little out-of-sample performance but included it to avoid any survivorship bias.

While generally consistent my port has been evolving (probably a better port now than when I started last year). The bench was the SP1500 Pure Value Index as my sim has a 0.78 correlation with this index:

.

No optimizer. All statistics and machine learning except sims were used to adjust the sell rule (i.e., RankPos > X) and to find the optimal number of stocks to hold (using time-series cross-validation).

My out of sample results are consistent with my walk-forward validation of this port (including a walk-forward validation of the feature selection). Suggesting this can be a useful way to select a port and get some idea of the expected out-of-sample performance. More out-of-sample data will be necessary to drawn any definite conclusions about this.

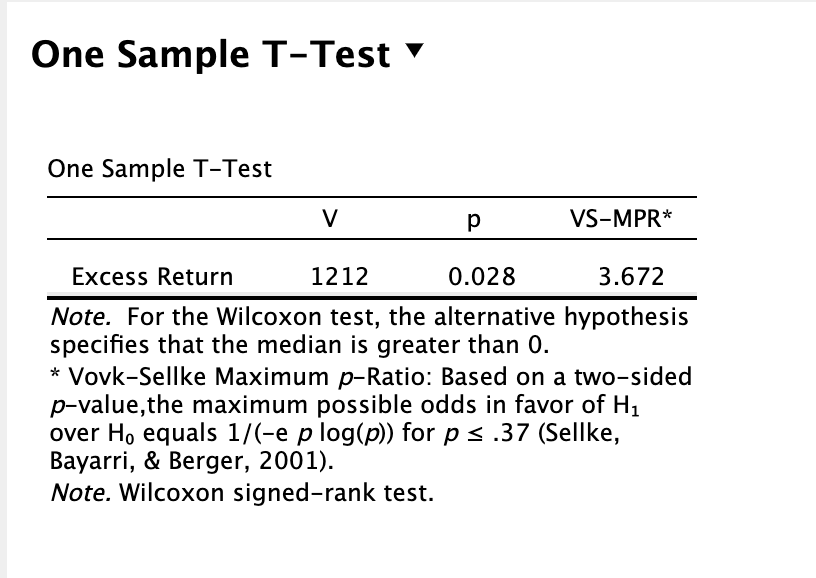

My median port (Tuesday) has the following level of statistical significance for excess returns relative to the benchmark:

I am for whatever works and I am happy for everyone’s success. Machine learning and statistics can work. I intend to fully support @Marco in his efforts to bring machine learning to this platform (see above for support of his plan).

Jim