Rod, very good questions indeed.

I don’t avoid optimization. For a while I tried not optimizing, but I gave up. I optimize by necessity. I just do it as robustly as I can. I have a ranking system that functions as a library–it has well over a hundred nodes. I try different combinations (weighting nodes by multiples of 2%) and test them over different time periods on different universes. Right now I have six different universes and six different time periods I test on. I take the ranking systems that perform best on each combination of universe and time period (36 combinations) and average the weights of them all.

Yuval,

I agree.

It is also my opinion that there is no need to avoid optimization. Optimization is not the same as overfitting. Your methods are similar (if not the same) as many widely used methods to avoid overfitting even while optimizing, I believe.

Not only do I agree but I do some things that I think are similar (in my own way).

I wonder if it would attract any members to P123 to be able to automate the optimization of 36 ranking systems and universes with 100 nodes in some way.

How long does it take to develop and test 100 nodes? 100 nodes before you start to optimize the ranking system for 36 universes.

I understand that Marco is already working on attracting members (or at least one paying member) by working on this. So this is not a request. Not even a suggestions as, again, Marco is working on this (if I understand correctly).

Automated methods are already being developed at P123 and will be made available to some members. And eventual roll-out to everyone over time.

This may be true also. The designers that do not do this are having trouble beating their benchmarks.

Understandably, some are using the other excellent tools (and methods) available at P123. I, for example, am using books a lot now. I believe some methods of diversification can beat the SP500 with considerably less risk. Others use timing or fundamental analysis.

Best,

Jim

Yuval and Jrinne

Thank you for your helpful responses.

With my plan I can only test rankings for about the last three years. I can test screens (thankfully) back to 1999. It seems I would need to upgrade to try to replicate such work Yuval. I am grandfathered into an old price plan so that would be a big extra chunk financially:)

Thanks and regards

Rod

Hi Yuval

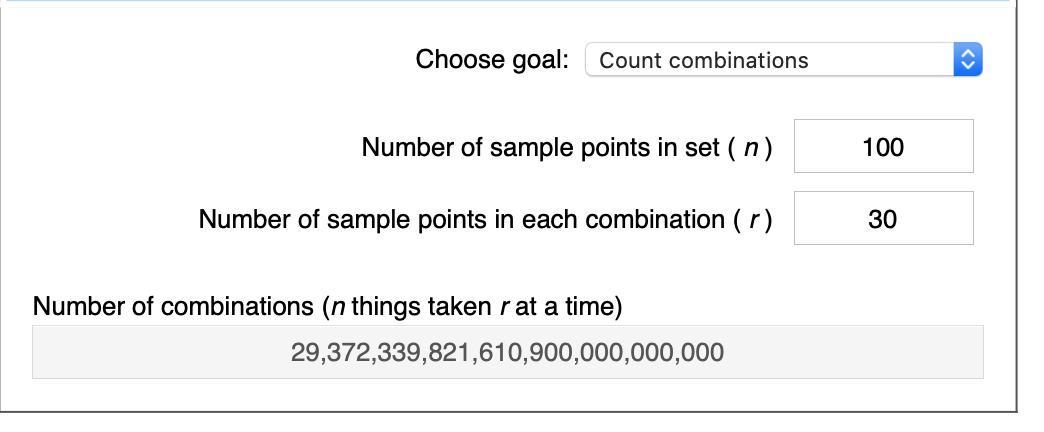

Can you please give me a hint as to how you optimise weighting nodes by multiples of 2%? If you have 5 nodes, and there are say 45 potential 2% levels (0 - 90%) then that ends up at 1.2 million combinations using my high school math. How do you do it?

Thanks and regards

Rod

Sticking with high school algebra and just the numbers:

29,372,339,821,610,900,000,000,000 combinations

If you select 30 nodes out of 100 there are 29,372,339,821,610,900,000,000,000 ways to do that or combinations of nodes.

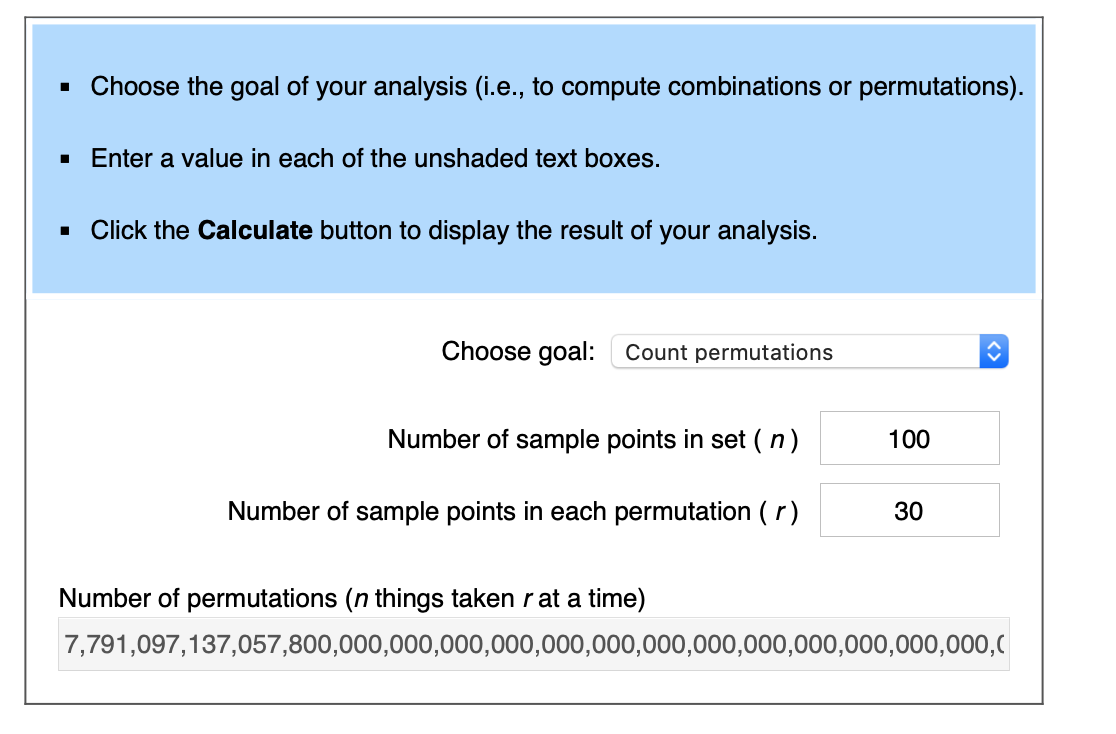

If the nodes have an order like highest weight to lowest weight you would be interested in the number of permutations:

7,791,097,137,057,800,000,000,000,000,000,000,000,000,000,000,000,000,000,000 permutations.

Computer time to solve this problem using Principle Component Analysis: 500 milliseconds.

Somebody has been self-isolating too long ![]()

Hi SteveA,

Do you mean me or are you saying it is taking you a while to do this with spreadsheets;-)

Best,

Jim

Two ways:

Iterative approach. Take some combination I already know works OK, tweak it, test it, repeat, repeat, repeat, repeat, repeat.

Combinatorial approach. Take a bunch of combinations I have already tested (and they work) and then randomly combine bits of them into new combinations (with variations) and test those.

I’ve been opting for the combinatorial approach lately.

It’s all about building on what you’ve already tested, not about trying something brand new.

- Yuval

I think you have too much time on your hands! Cheers.

SteveA,

I think Rodney has a serious point and question. Namely, that a purely iterative approach does take some time.

Judging from your designer models you could probably provide some serious suggestions for narrowing the number of factors and functions for consideration in a ranking system (if that is a method you use).

My serious suggestion was that some of this can be automated (with PCA as a provided example). I didn’t (and won’t) expand on that as I think this is probably not a method of interest to Rodney.

But I think it is a serious question that we all have to address one way or another—as Rodney points out so simply and elegantly.

Best,

Jim

Jim - thanks for noticing!

It comes down to choosing industries that you think will prosper, then optimize your ranking system based on the industry.

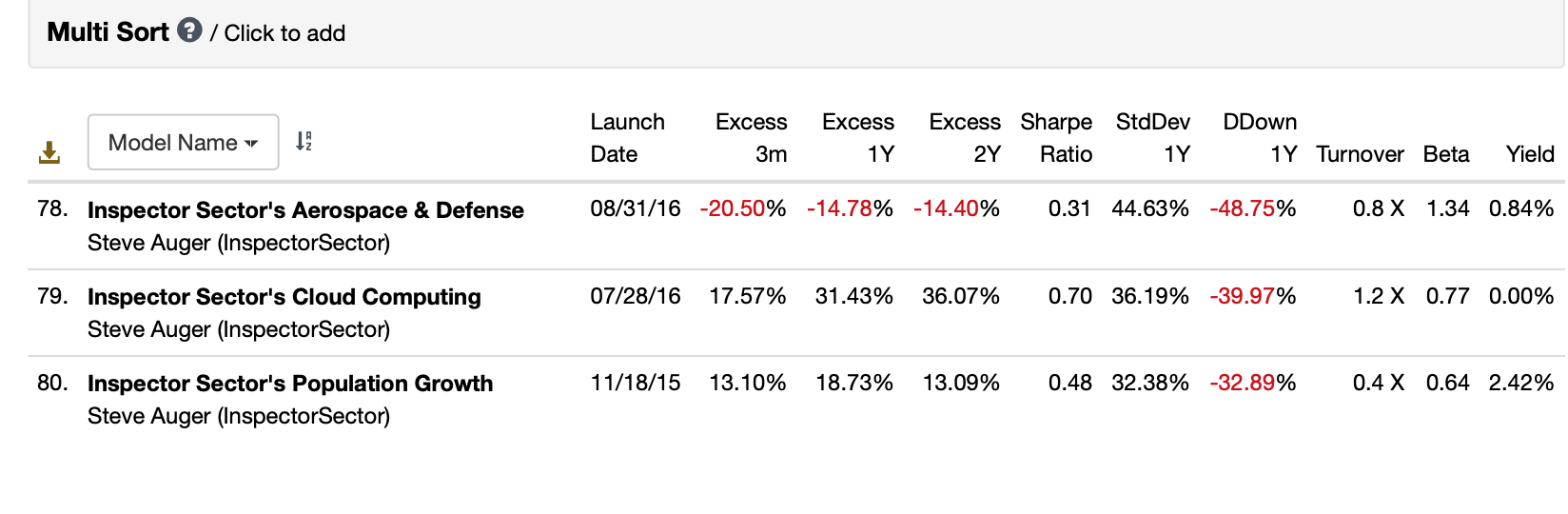

Unfortunately, Aerospace & Defense suffered from the Boeing 737 Max debacle followed by the pandemic which is a disaster for the aerospace industry. This has resulted in very poor results for that particular DM.

Cloud computing, on the other hand, is benefiting dramatically from the pandemic as there is a seismic shift to work-from-home and online retail.

Once you have chosen a particular industry then RS optimization comes into play. If you believe that intelligence wins out here then simply choose the factors you believe in and run with it. For the rest of us, RS optimization is a lengthy process if you want it to be. Or you can simply choose the P123 ranking system that gives you the best results. Usually that is GreenBlatt by the way.

In the case of cloud computing, revenue growth is the most important factor. Forget value factors and earnings.

Take care

SteveA

Thanks Yuval, Steve and Jim.

Interesting Steve. So are you making a curated universe in this case, or are you piggy backing off some ETF holdings? (for say, the cloud model?)

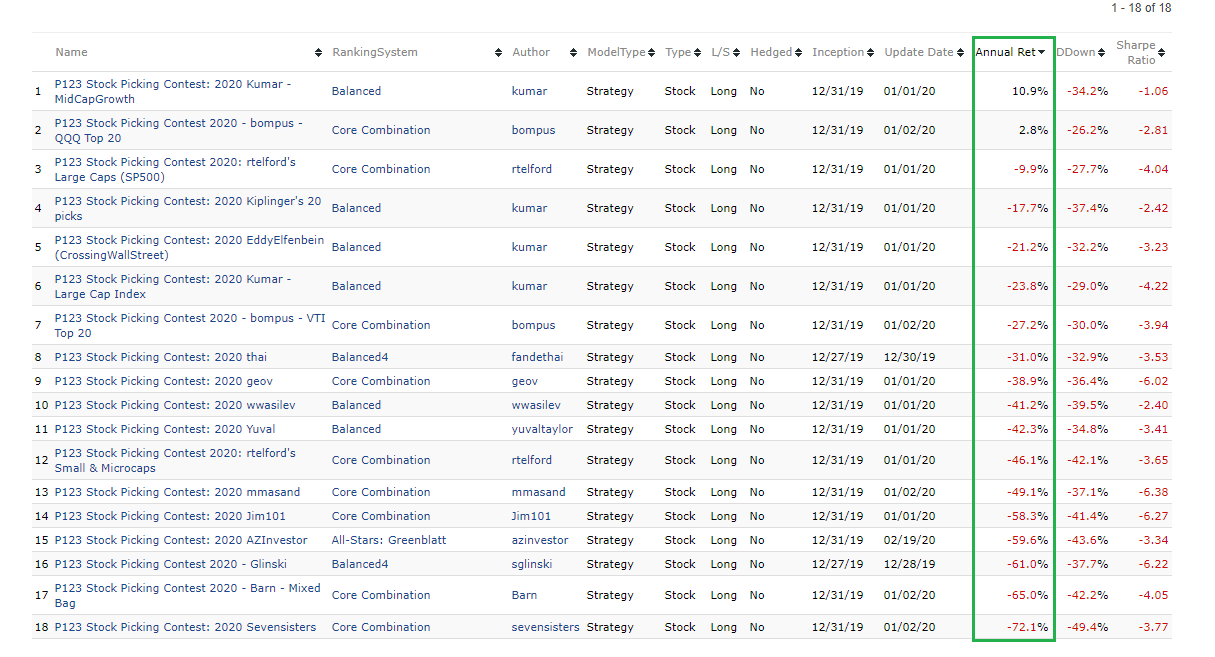

Here, 2 of the models are positive for 2020. Being 12 months holding model; It looks good.

Thanks,

Kumar

for those who never had chance to see this public portfolio.

This is competition started by YuvalTaylor since 2016.

to access to these public portfolio.

this are the steps.

-

click this link

https://www.portfolio123.com/app/opener/PTF/search -

follow the attached screen.

Thanks,

Kumar

I use the constituents of SKYY ETF which are X-as-a-Service stocks. I periodically load the constituents into an InList which is used as the custom universe.

Guessing the market is hard. Raise your hand if you predicted in late March that IWC would be up about 43% in the next 30 sessions.

Hi Steve,

can you tell us where you can find the constituents for ETFs ? I have a hard time finding them. Yahoo Finance has only 10 stocks of each ETF listed. Is there a site that has this data?

Thanks.

Werner

https://etfdb.com/etf/QQQ/#holdings

www.morningstar.com free membership will list top 25 holdings.

for premium member it will list all the current holdings.

As individual investor top 25 holdings are good enough. It will be accounted for more 60% allocation.

Thanks,

Kumar

Werner - you have to go to the ETF manufacturer web page. They have to provide the holdings by law. For example:

https://www.ftportfolios.com/Retail/Etf/EtfHoldings.aspx?Ticker=SKYY

SteveA