That’s what I think too.

In addition, even with a single factor, unoptimized, that performs particularly well, there is likely to be some element of luck and that factor will also regress to the mean (usually); albeit to a lesser extent.

That’s what I think too.

In addition, even with a single factor, unoptimized, that performs particularly well, there is likely to be some element of luck and that factor will also regress to the mean (usually); albeit to a lesser extent.

I’ve made that mistake in the past - trying to live off trading profits. It doesn’t work very well, because you cannot take an average 20% CAGR as being equivalent to a $20k income- it is an average, some years will be more, some years will be less. If you are drawing down on your portfolio for your living expenses, it massively magnifies the effects of drawdowns, as percentage wise you are taking out a higher percentage of the investment when the portfolio is at a low, quite the opposite of what you “should” be doing.

E.g. portfolio draws down 50% (worst case), now you have $50k. Draw out $20k for living expenses, now you have $30k remaining, you need to make over 300% to get back to your starting point.

Another problem is that if your portfolio does very well one year, up 50%, human nature is to take that as given and go out and spend the profits, rather than tucking it away for a rainy day.

Unless you really have a lot of money (millions plus) and are really disciplined about spending, I think it is better not to contemplate spending your trading profits.

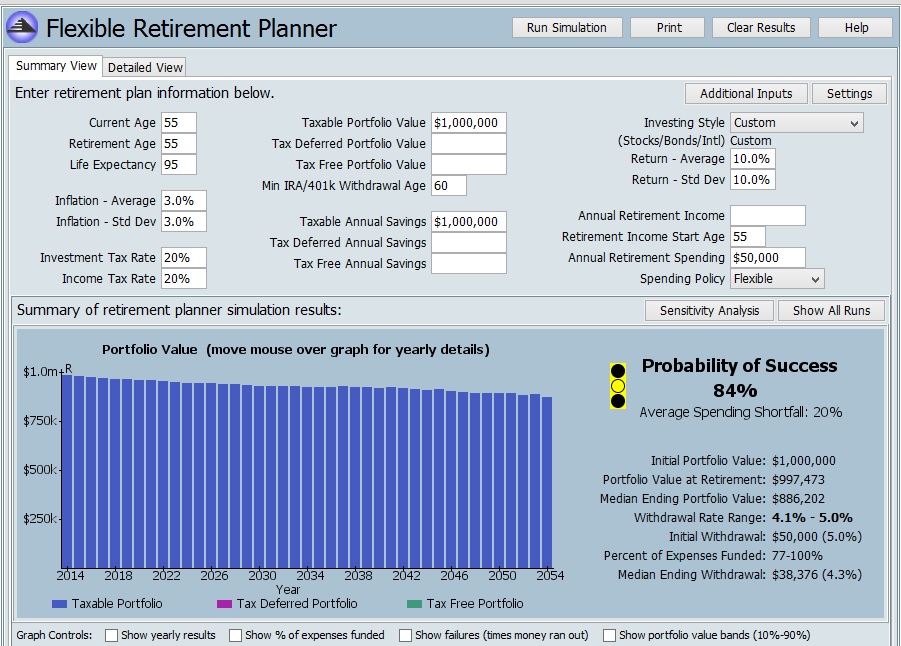

Well at some point many of us will retire and many of us will expect a significant portion of their income to come from trading. There is a lot of research around safe withdrawal rates. The amount that can safely be withdrawn is based not just on return, but also on volatility. There is an excellent tool for demonstrating the impact of volatility here: Planner Launch Page | The Flexible Retirement Planner

In the example below I assumed a person retiring at 55 with a 40 year life expectancy, a $1M taxable portfolio, and a $50,000 annual income need. That is a 5% starting withdrawal rate which is notably higher than the 4% rule of thumb. Assuming 10% annual returns I changed only the standard deviation of those returns, using 20%, 15%, and then 10% which is shown below. The corresponding probability of success calculation was 53%, 67%, and 84%. Avoiding large drawdowns is not only helpful in sleeping at night, it can allow a higher withdrawal rate in retirement. To replicate my test (or another variation), just go to the website, enter the fields and click run simulation at the top of the page.

Don

Jason Zweig recently had an article stating that there is near 100% of reaching your retirement goals if you accumulate 22 times your expected retirement income (so $100,000 yr requires 2.2 million).

I expect my ports to underperform my sims due to optimization (all other investors have the same rate limiting step) but hope that this is minimal. Multiple strategies with low correlation reduces this risk on a short term basis.

Consider reducing your repeated monthly expenses as some others have suggested. Saving a dollar may be twice as valuable as earning a dollar due to taxes, and taxes in California where some of you reside, are quite painful.

Scott

Keeping your day job as long as you can is the best ‘retirement’ investment plan.

Good point.

While I plan to trade for several years after retiring, I know from looking a relatives that I will likely live for many years after I’ve lost the interest or ability to trade stocks. Hence my plan is to start retirement with a minimum of 5 years living expenses in cash and have that cash bank account increase signficantly during the first half of my retirement. Ideally I’d like to put three times as much into the cash retirement account each year as I plan to draw out for living expenses. So if I were to retire at 65, and actively trade to 75, there should be sufficient cash in the savings account to cover me until 100.

So I don’t plan to retire until I have both of the following in place:

a minimum of 5 years living expense in a savings account outside of my brokerage accounts (I’m thinking about 350k but that target might change).

my brokerage account to the size where it can reasonably be expected to generate on average 3x living expense needs per year. I’m currently targetting brokerage account total of 800k and once that is achieved, future profits will not be reinvested but transferred to the saving account until it passes the 5 years of expenses.

Only a few more years - unless there’s a major correction which would push things out 1 or 2 additional years.

Oh, I’ve got some other income (real estate, etc.) not counted in the above, so please don’t assume that the above (800k + 350k), by itself, would be a prudent retirement plan. I think that would be on the low end. The risk of running out of money during the 2nd half of retirement is very real for those that retire with just the minimum.

Brian

My wife and I spend over $20k per year right now on health care and insurance. We are not on Medicare yet but even when we are, we will still have health expenses. This is our biggest expense now. If you have a good employer, as I did previously then it is a big chunk you don’t have to worry about. A million used to be considered a large amount but no more.

There are two main components to accumulating an adequate quantity of wealth, generating profits and expense reduction. Consider reviewing and cutting your expenses via the following framework (the figures below are based on US dollars and US prices)

High cost(can save well over $1000/month): Move to a smaller place or a less expensive area. Send your child to public rather than private school.

Moderate cost(can save up to $1000 or more a month): Reassess your larger recurrent expenses including insurance (shop for lower cost health, life, disability and homeowners insurance plans), cars (drive your car longer, buy a less expensive car, own fewer cars, and avoid car leasing unless it is a business expense), and decrease your food expenses (shop in a discount supermarket, eat out less, or eat out at less expensive restaurants).

Lower cost (can save up to several hundred dollars a month): Reassess you smaller recurrent expenses including cell phone plans, cable, home phone, internet provider, …

If you are going to splurge then let it be on activities. Experiences statistically have a greater impact on ones happiness than material items.

Many of you may find after a complete expense review that you can save more to invest and/or need a smaller nest egg to retire.

I should also note that this site is well worth the subscription fee.

Scott

I think saving money by living well within your means may be more important. Working without saving doesn’t help. Scott has excellent advise in the prior post.