You can backtest gbtc on tradestation using their drag & drop technical indicators. These indicators can also be modified by opening up the code box. It looks like you can also backtest short indicators but I haven’t played around with it long enough to understand how to do this. It’s not as good as P123 (less user friendly & less options) but it’s a start until the grayscale data sets are loaded into P123. Note that ytd bitcoin is up 65% vs gbtc 15%

I was hoping that there is also bitcoin (and ethereum) price data in tradestation for backtesting.

As you mentioned, there is a large discrepancy in price between gbtc and bitcoin and it is risky to assume that a GBTC backtest will also works for bitcoin. However, it seems that is what P123 and tradestation can do at best.

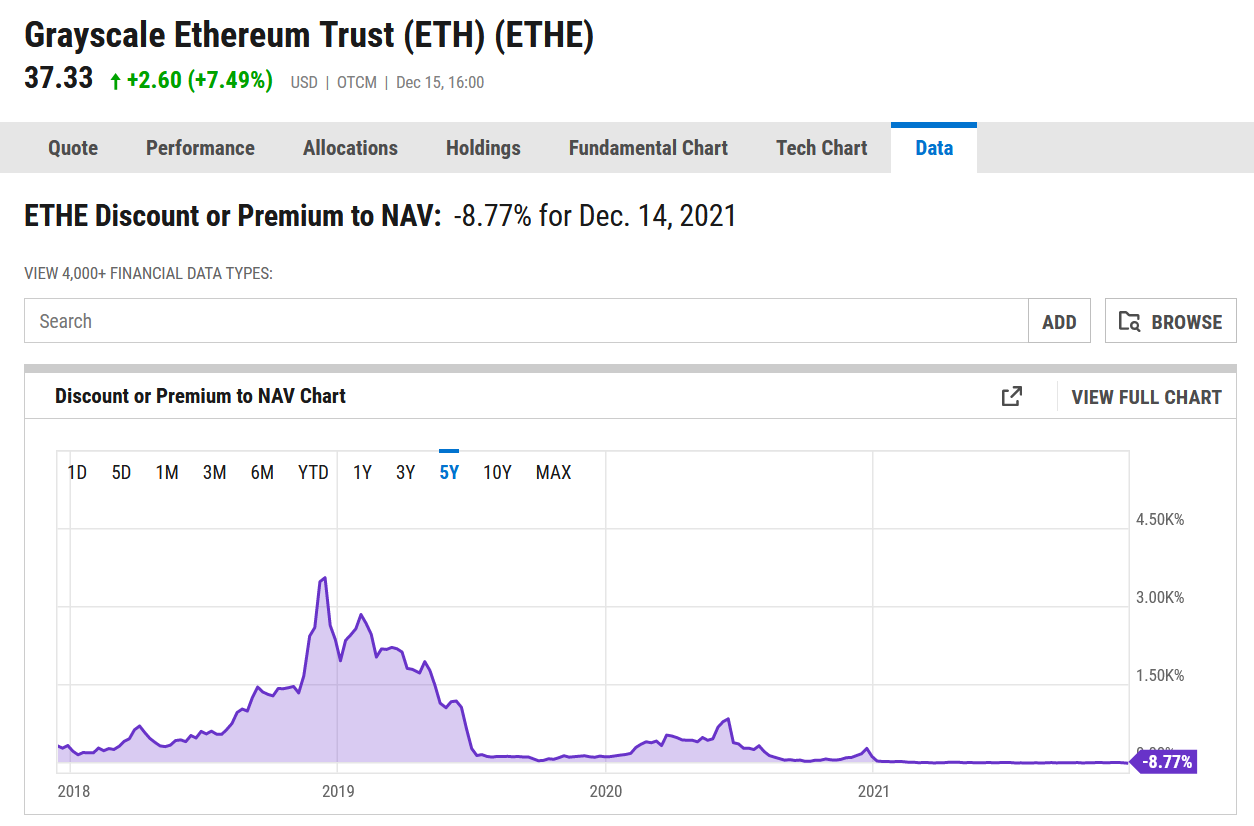

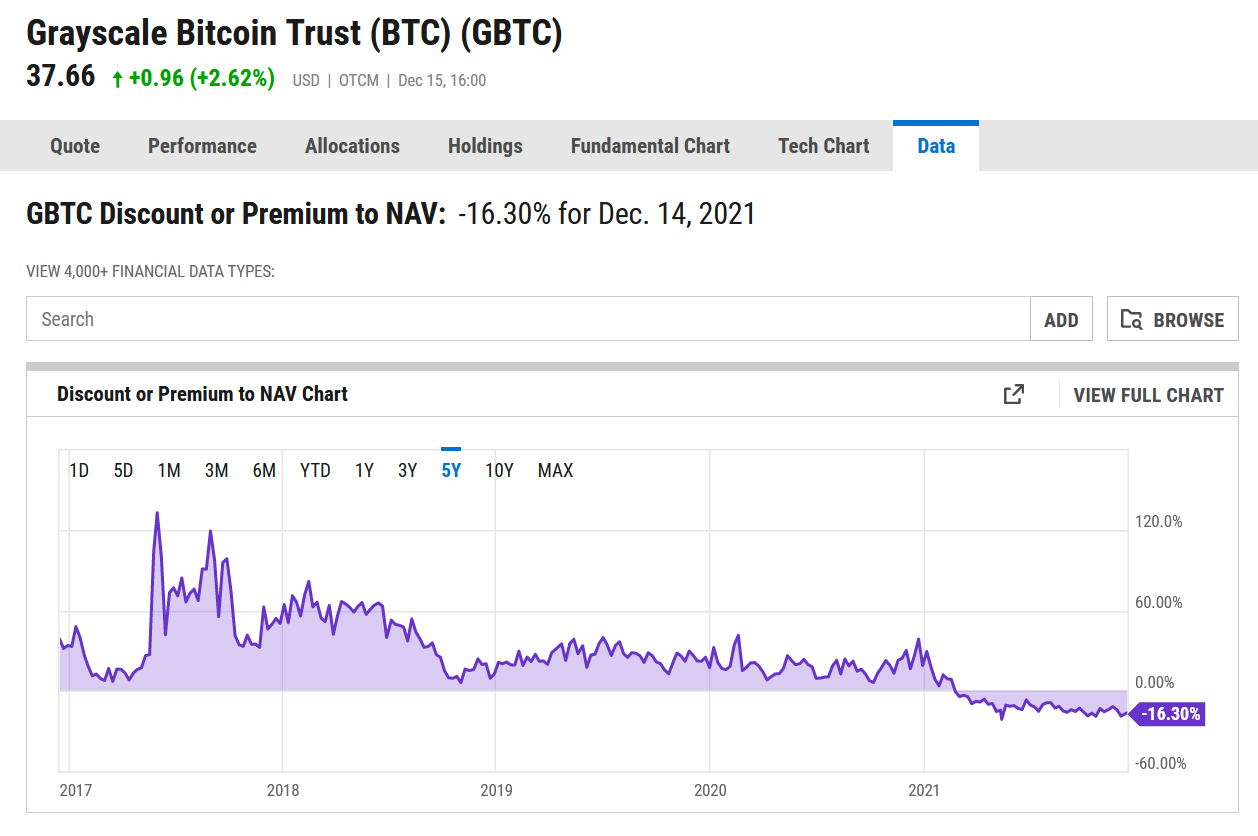

I think we can use GBTC and ETHE to approximate Bitcoin and Ether if we pay attention to the discount/premium. This hopefully will be included when the increased history is added to P123. GBTC and Bitcoin were tracking pretty closely until about a year ago when GBTC went from a 40% Premium to a 17% discount or a change of 57%.

Alternatively, you can trade BLOK instead of GBTC/ETHE and not worry about the premium/discount issue.

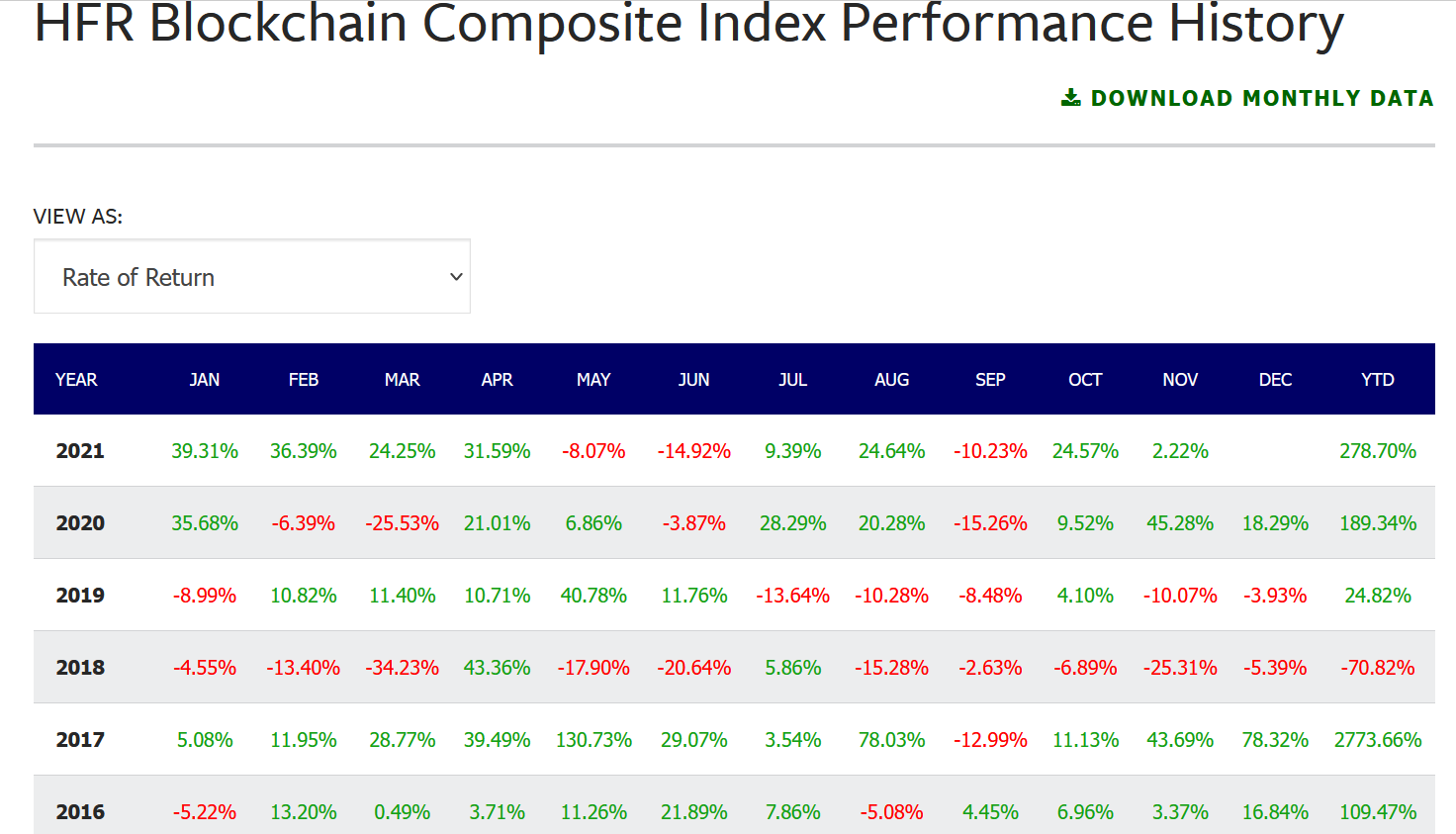

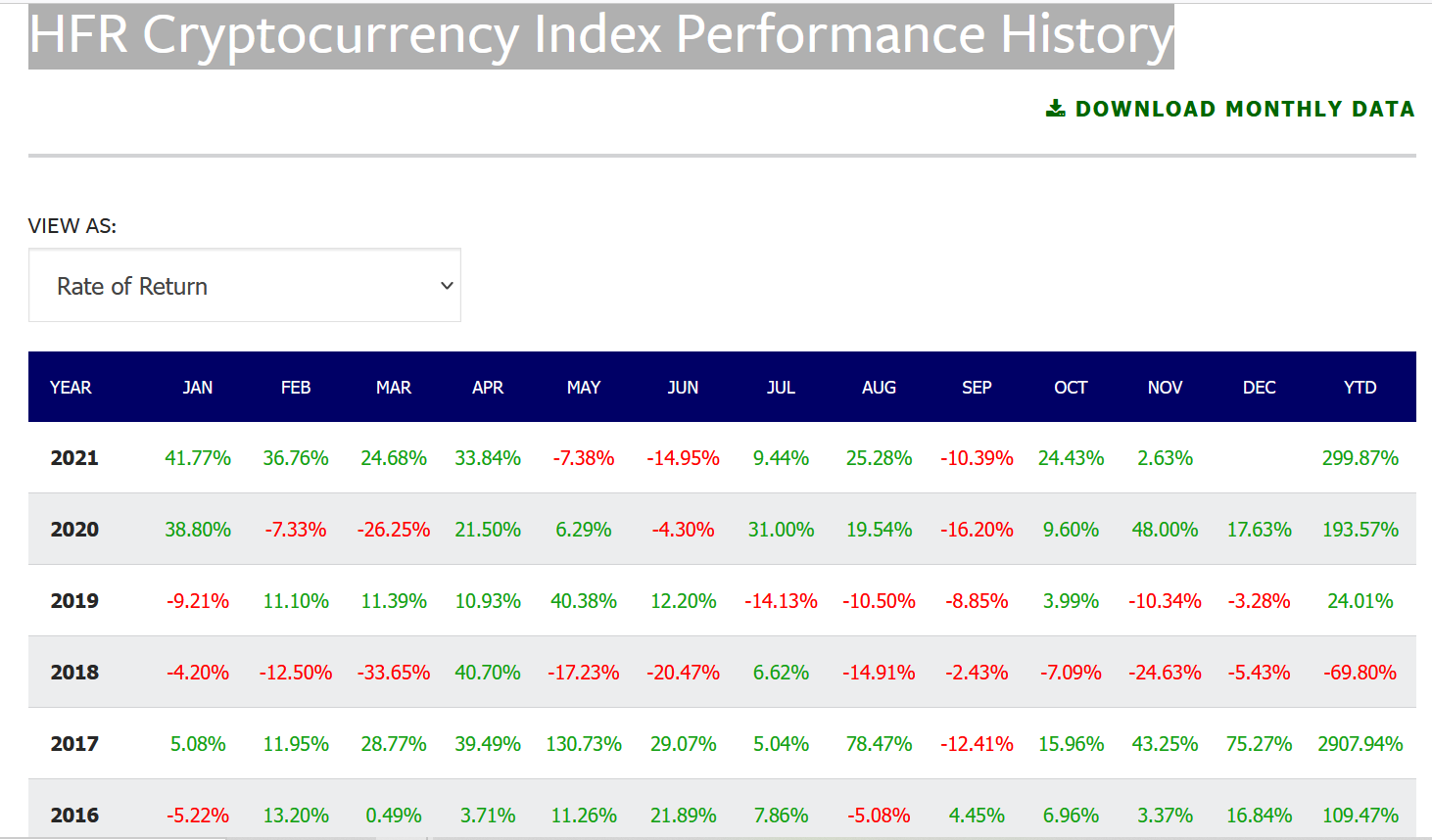

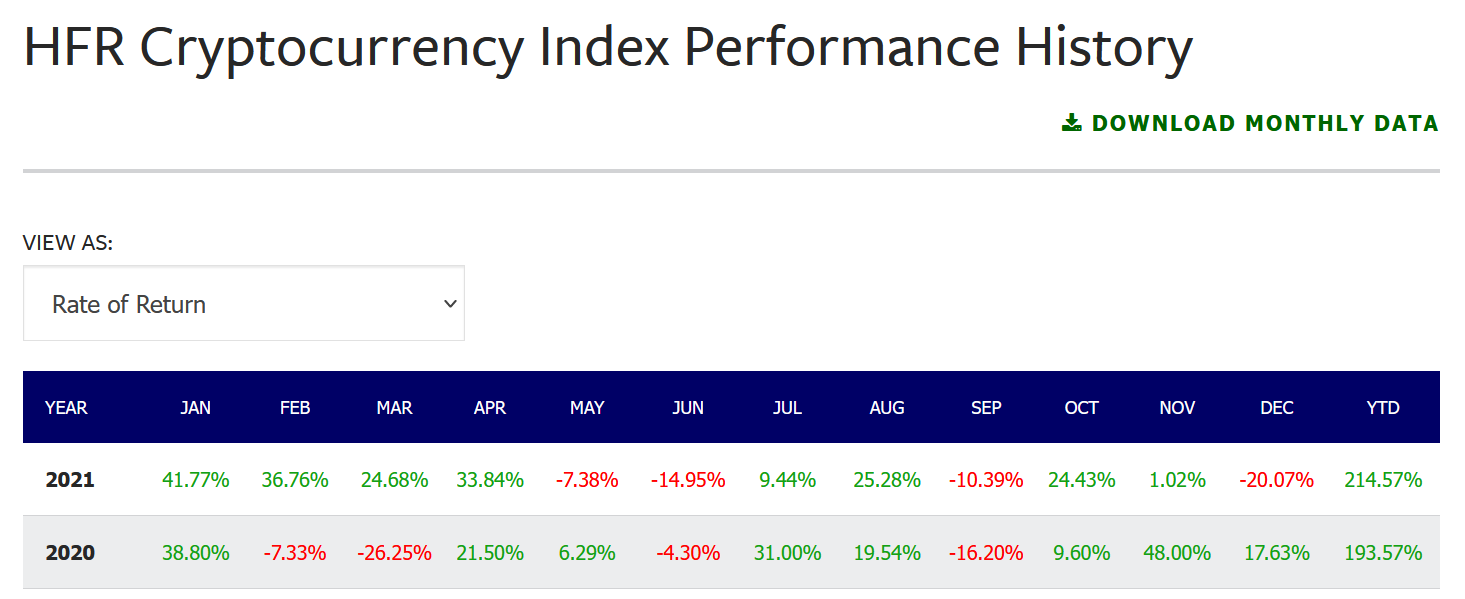

If you look at the two charts below, the performance of cryptocurrency index and blockchain companies index are almost in sync in the past few years

I think I will continue to use my manual backtesting results with Binance and use P123 to backtest BLOK.

The Premium/Discount issue can be a huge problem (when trading spot bitcoin/ethereum based on backtesting of Grayscale trusts) if you look at the 5 year history of Premium/Discount to NAV (especially for ETHE).

Good point on the correlation between bitcoin and blok (I’ve noticed that too). That premium erosion on ethe is brutal. Bitcoin has diverged (taken off) relative to Blok in returns which started a little over a year ago (The divergence between gbtc and bitcoin occurred around the same time). Sticking with Blok and Bitcoin/Ether is a good idea. I’d love to have Bitcoin and Ether here rather than the Grayscale funds.

I have a screen for BLOK and currently using it. (3 year annualized return 92% max drawdown 13%)

If you want it, I can share it with you. (just give me your email address so that I can send you the formulas or we can arrange a time via email to make it “public” so that you can download it from P123).

I am replying to your email here so that other P123 member can also benefit from our discussion.

50% annualized return and 50% drawdown is suboptimal. You can easily achieve that with a high risk stock portfolio.

You should aim for at least 75% annualized return and 33% drawdown for a successful bitcoin strategy.

In addition, I don’t think you should be over concerned about curve fitting when you are only dealing with one asset and only with TA. Overfitting is more a concern when you are picking a portfolio of stocks using lots of different factors.

Pseudo-Mathematics and Financial Charlatanism: The Effects of Back test Over fitting on Out-of-Sample Performance

From the paper, "For instance, if only five years of data are available, no more than forty-five independent model configurations should be tried. For that number of trials, the expected maximum SR IS is 1, whereas the expected SR OOS is 0. "

It is very easy (for me) to over fit when back testing a security (i.e. Bitcoin with 6+ yrs & Ether with 3+ yrs.) with a short price history, particularly when there are very few transactions and many configurations are tested. The greater the number of transactions (i.e. number of securities X frequency of re-balancing X length of history ) and the fewer the number of trials then the lower the chance of over fitting. I tested several moving averages on several cryptocurrencies as a sensitivity analysis to determine whether the concept had any merit. It does for controlling draw downs at the expense of return.

You’re much better than me as I can’t come close to making 50% returns per year out of sample on a consistent basis with a stock system

You are more concern about overfitting than me. (I don’t know whether it is a good or bad thing). The paper that you quoted from Marcos López de Prado is from a while back and I have already seen it. You can find more of his recent papers on the subject here :

I have made 50%+ annualized return out of sample for 3 years in a row, it is more about risk-off to GLD/EDV/TLT when necessary (I do daily rebalacing and may risk-off even for 1 day) AND add some volatility trades (VIXY) when market is in FEAR mode to boost return. For risk- on, I buy QQQ/XLK and occasionally BLOK (based on the screen that was sent to you earlier).

I will send you another message with more info. Pls check your email.

We started this thread by discussing 2 Bitcoin models, one of which is the stock to flow model, then started discussing over fitting of models. This is interesting as the stock to flow model looks like it may be breaking down which could be due to over fitting.

As mentioned in the email, here is the update for PlanB’s models

1)Nov98K & Dec135K miss = FLOOR MODEL FAIL According to PlanB, misses like these have not happened last 10y. He thinks that Floor model is like 200 week moving average but with geometric instead of arithmetic mean. Geometric mean never increased <4.9% per month. So he could calculate BTC Aug-Dec. However Nov was only 3.7% and Dec 2.7%

Dec100K miss (Stock to Flow model) : PlanB has said earlier that if BTC<$100K Dec2021, then S2F is “off the rails” “invalidated” “dead”. He now believes that Key is that BTC $50K is still within 1 standard deviation band of S2F model (roughly $50K-$200K). If BTC stays within 1sd band for the next 2.5 yrs, he thinks S2F model is still valid and indeed useful.

I am glad that I took profit on Bitcoin at the 53,500 level based on TA (weekly Parabolic SAR) and only take PlanB and Ben Cowen models as reference.

I want to know how you are getting along with the Tradestation backtesting.(is BTC/USD and ETH/USD available?)

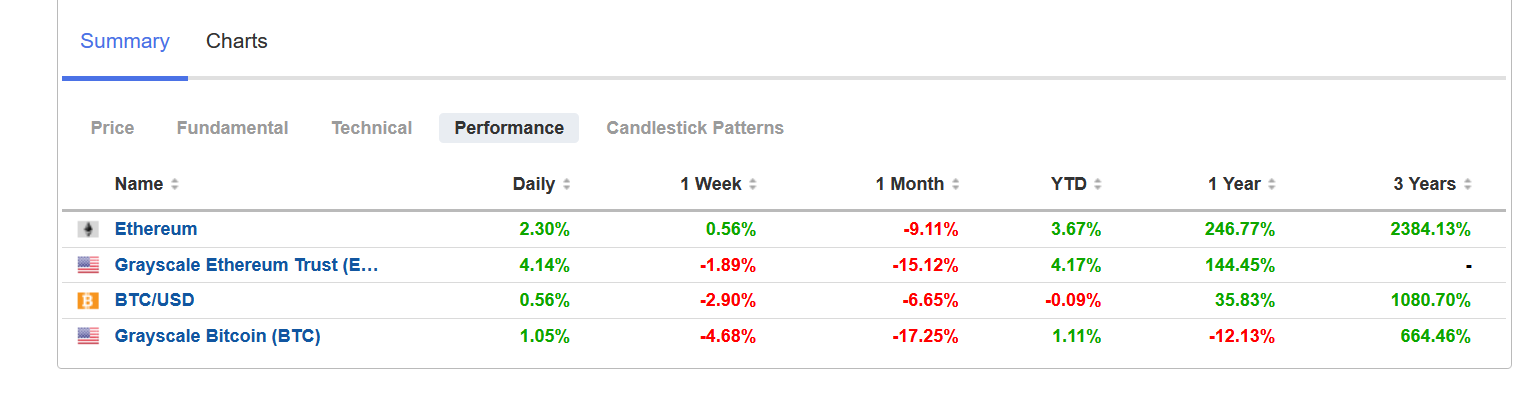

If you look at the image, there is 47% difference between GBTC and BTC/USD and 100% difference between ETHE and ETH/USD for the past year. This makes any backtesting for GBTC and ETHE on P123 platform (when their data become available) not very meaningful due to their large discount to NAV. Cleo.one is also closing down in preparation for a new site later this year.

Tradestation allows one to back test gbtc and ethe to their origin but not BTC/USD or ETH/USD. I agree that the discount/premium is a significant issue when back testing them

what do you think of this article, “The Fed move means that people who were thinking of crypto as actual currency are going to get their bubble popped,” says Chen. “Many Bitcoin types were thinking that it is a currency and that it would replace traditional currencies. Well, not if the Fed, the European Central Bank, and other central banks have anything to say about it.”

I think it will depend on the future market acceptance of DeFi, (decentralized finance) which continues to favour cryptos vs CBDC (central bank digital currency).