Yury - I’m not experienced in this matter but R2G probably doesn’t give you the track record that you need. A hedge fund would need to see actual execution prices for your entire trading account going back a couple of years

So you do have a system! Perhaps I am not too far off the mark. Telling everyone there is nothing out there that satisfies your needs, then by the way, I happen to have one that does and I’m offering it on R2G…

They were and they are. But they don’t command subscriber interest when they are shown eye-popping sims for low liquidity models.

One dimensional thinking.

Rolling backtest doesn’t demonstrate “the system”, it demonstrates that the designer is capable of optimization and the ranking system / screen function, not the entirety of the system. I’ve made this comment in past threads. One is really testing the startup, not the ongoing activity. And unfortunately, like sims, it is marketing/promotional material, not results.

It sounds like you are changing the rules of the game. i.e. liquidity. Before you get too confident, try actual trading through a bull market. The period from July to present wasn’t. And stocks not available will affect your results, one way or the other, either through less trading, or choosing weaker positions.

[quote]

The difference between 5 stock system and 50 stock system is in st dev primarily. And it is main concern. If you want attract real money you should minimize it.

Second, 5 stock OOS performance is completely unpredictable and even worse because of extreme backtest optimization already mentioned.

[/quote]You are missing the best value for 5 stock ports. You are correct that there are many 5 stock Ports that are over optimized and not worth investing in. I suggest that you consider this approach: Take your best ten 20+ stock ports that use different approaches and are relatively uncorrelated with each other. Make sure that they are not over optimized and are Ports that you think are worth investing in. Rerun them as 5 stock Ports with no other changes. The 5 stock versions should have higher performance than their 20+ stock versions, but the SD will be much higher (at least ALL of mine do). Now add the ten 5 stock Ports to a book. I submit that you now have 50 stocks to trade and the performance, Max DD, SD will all be better than any of the original 20 stock Sims.

I hope that you no longer consider ALL 5 stock ports “completely unpredictable”.

“The 5 stock versions should have higher performance than their 20+ stock versions, but the SD will be much higher (at least ALL of mine do)”

Not necessary. For the non over-optimized ports most likely we see 5 stock performance is worse than 20+ (perhaps in terms of sharpe ratio and st. dev for sure as you confirmed, for my ports it is true in both terms). Also the book comprising 10 20+ ticker ports will have at least 4 times higher liquidity than 5 stock port book. Besides if you combine 10 5 stock long ports (uncorrelated to each other and to the market, correlation let’s say <0.5) you ll get 50 stock book correlated to SPY more than 0.75 anyway.

If you capture your alpha by a some specific way more likely it exists not only in 5 stocks, but maybe more. You extract your alpha from bigger number of stocks thereby lowering risks not to get your alpha at all (as it can be in a 5 stock case). Much more important it becomes then your have $50M in capital rather than $100K. Alpha is limited and you extract it from all possible sources to make it bigger in absolute terms.

You have made many claims in your last post that have been unsupported with facts. You obviously still haven’t tested a book of 10, 5 stock ports, or you would not have made those statements. You come back with 10, 20 stock ports trading 200 stocks. 200 stocks! Really? isn’t that approximately equal to an index? I trade 50+ carefully selected stocks in order to have a possibility of doing better than an index.

You have been a member of P123 for 1 year and I have been a member for 10 years. I have 10 years experience with live trading many uncorrelated 5 stock Ports, and I was able to retire early because it works. You started this thread asking for help and many members have tried to help, but you have shot down all their ideas without even trying to test them to see if there may be some useful information in them.

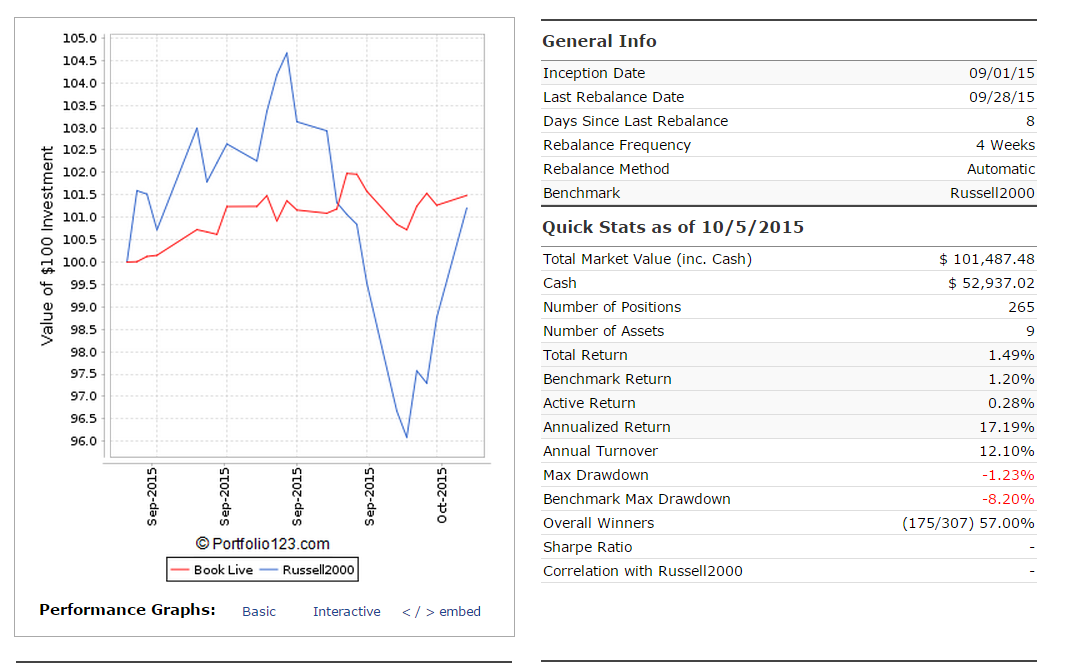

The fact is attached. This is the first gen of my live book with 250+ unique holdings including ETFs. I don’t have 10 years live history but it captured the recent second drawdown. As you can see it doesn’t seem to be an any index.

If you claim that 5 stock port books perform much better then show us. Not a simulated book but live of course, especially if you have 10 years track record.

“You started this thread asking for help and many members have tried to help, but you have shot down all their ideas without even trying to test them to see if there may be some useful information in them.”

The reason I started this theme is that to understand if anybody engaged in developing investment grade systems instead of trying their luck in 5 stoсk ports. I already tested 5 stock systems based on logical and robust ranking systems consisting almost all available factors and tools in P123 and results (lets say sharpe ratio for simplicity) were worse than in 20-50 stock ports (of course not taking into account cherry selection optimization process that comprises 95% of R2G). If you have an evidence of opposite view then show it. Nobody showed live book or real trading account yet except Tom for the small period.

Sry, I don’t know how to delete wrong pictures from the post:)

Yury - let me assure you that your $200K Dollar-Volume short system for which a fair number of the selections can’t be borrowed is not an “investment grade system”. The Stitts Wealth Management system is fully described and out there for your criticism. Your 250+ combination of securities isn’t. Put up a full description of each and every one of the systems in your book so we have the ability to criticize your endeavor.

On a final note, here is a 50 stock system called “Stitts 50 Titans” which ran on R2G in the beginning. The bottom 20% liquidity was > $37M. I pulled it down due to lack of interest. If you want a true institutional grade system then you can buy it from me, but it won’t be cheap, you’ll have to be a fund manager to afford it.

It has sharpe about 0.9 I think on annual basis. But uses MT again. (My long only 100 ticker system shows the same sharpe without any hedging or MT).

But I didn’t understand is it a simulation or out-of-sample simulation (presume you build it several years ago)?

It is a great pity that nobody interests in such systems. It is difficult to manage 20+ ticker system for ordinary user, it is the main problem besides potentially higher trading comissions. Cause if they want increase their return that seems not enough for them they can use low cost leverage in IB, liquidity is enough for limitless leverage:)

I think there is a potential solution. Link subscriber accounts to an advisery account and trade one large system for many client suppose prorata shares allocation. It will be convenient and cost efficient structure. What do you think?

Having a system that meets/exceeds those conditions is not too complicated, but what is the incentive to share it instead of using it for oneself? The key question to ask here is why was standard deviation used at all? Surely all knowledgeable enough would agree this metric is quite flawed (in this context). Seems to me you are imposing a limitation on yourself for no good reason.

Something like this was tried several years ago. Everyone thought it was a great idea but in the end there was insufficient interest. For the most part, this site consists of DIY investors.