I have created 100x RS, that I want to test in Dataminer and the screenbacktest.

How do I create a input for the 100 backtest screens with different RS inputs? Just duplicate the input and change the RS “Ranking” name? :

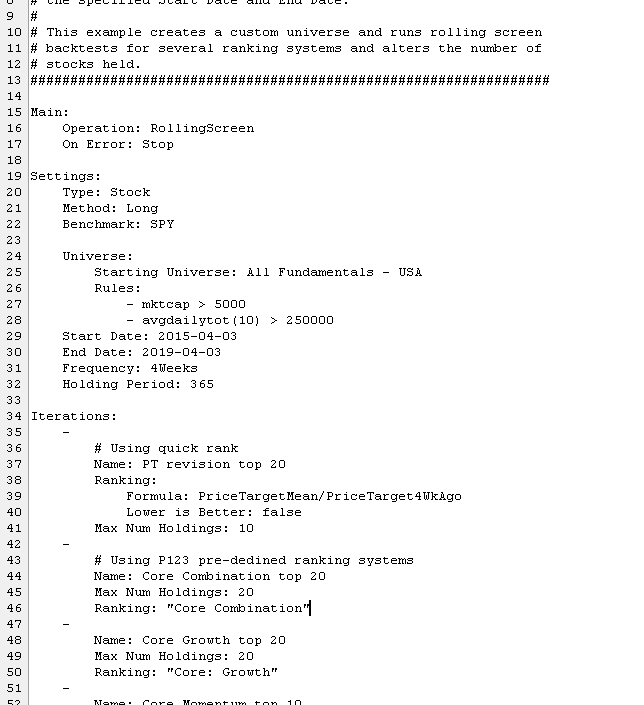

####################################################################################

The ScreenBacktest operation is basically the same as the ScreenRun operation

except that the screen is executed multiple times at the intervals set by the

Rebalance Frequency parameter for the period defined by the Start Data and End Date

and the returns are calculated for the screen’s holdings.

Below is an example of a screen backtest which will:

- Start with the US All Fundamentals universe.

- Buy the top 20 microcap value stocks which are showing strong momentum.

- Run the test for the past 10 years and rebalance every 4 weeks.

- Set the price of the stock to the average of the high and low price on the

buy/sell date and add .25% ‘slippage’ cost to the transaction.

####################################################################################

Main:

Operation: ScreenBacktest

On Error: Stop

Settings:

Start Date: 2006-01-01

End Date: 2023-05-01

Rebalance Frequency: 4Weeks

Slippage: .25

Ranking: ‘1’

Universe: 1. Pareto - US CANADA volumfilter

Max Pos Pct: 25

Max Num Holdings: 25

Benchmark: IWM

Trans Price: AvgHiLow

Rules:

- MedianDailyTot(91) >( 70000) and price > 0.5

Main:

Operation: ScreenBacktest

On Error: Stop

Settings:

Start Date: 2006-01-01

End Date: 2023-05-01

Rebalance Frequency: 4Weeks

Slippage: .25

Ranking: ‘1 - Copy’

Universe: 1. Pareto - US CANADA volumfilter

Max Pos Pct: 25

Max Num Holdings: 25

Benchmark: IWM

Trans Price: AvgHiLow

Rules:

- MedianDailyTot(91) >( 70000) and price > 0.5