Mark. V

asset allocation is successful investment for long term. I should cultivate the discipline and mindset to stay for 5 to 10 years.

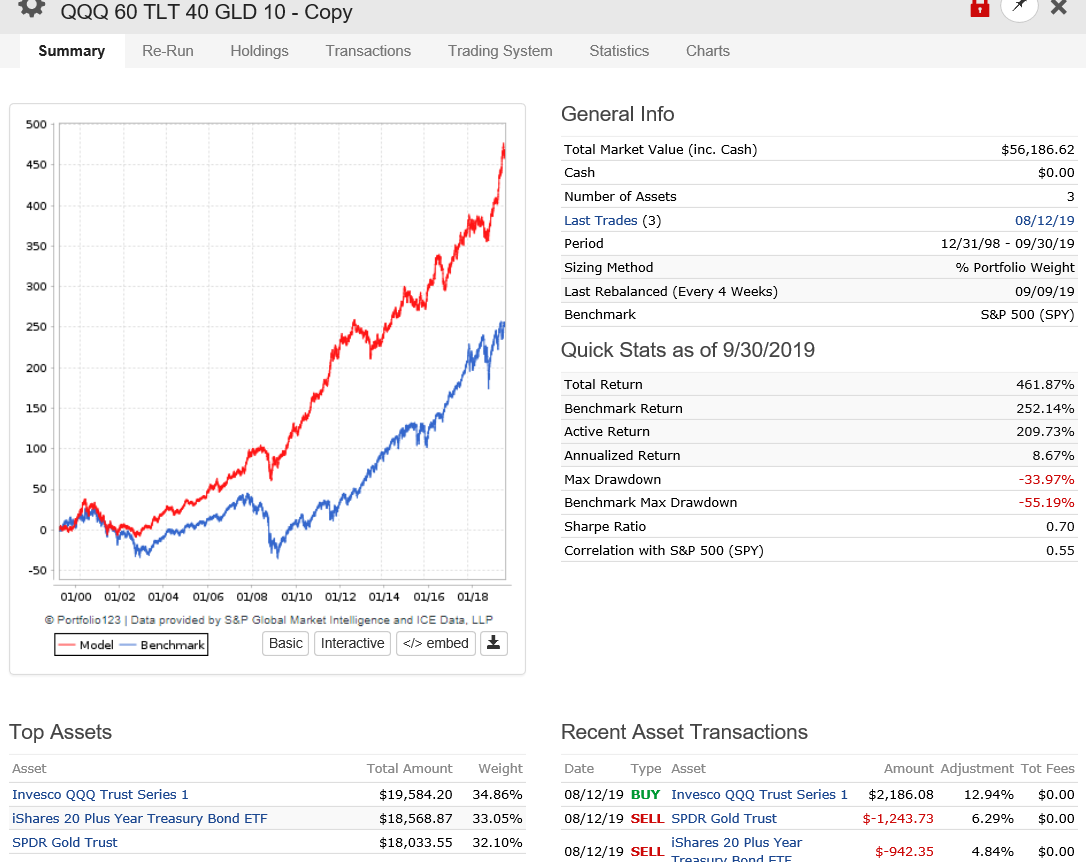

here, equiweight strategy for QQQ, TLT and GLD. these ETFs are non-corelated performance. should standout all the market cycles.

Thanks for sharing personnel investment strategy.

Please, suggest any books for asset allocation and long term investing; like multi year holding., so i can get knowledge in same lines.

Thank you for your generous helps.

Kumar ![]()