I’m not an expert in accounting by any means, so please don’t take what I say as gospel. But I would be very wary of considering non-debt liabilities as debt, or even as a bad thing. Here are two reasons.

An academic study from 2004 showed that the lower the ratio of net operating assets to total assets is, the better the company will do. It’s called “Do Investors Overvalue Firms with Bloated Balance Sheets,” and it concluded, “In our 1964-2002 sample, net operating assets scaled by beginning total assets is a strong negative predictor of long-run stock returns. Predictability is robust with respect to an extensive set of controls and testing methods.” Net operating assets is defined as operating assets (total assets minus cash and equivalents) minus operating liabilities (total liabilities minus debt). So net operating assets is total assets minus cash and equivalents and minus non-debt liabilities. And since the LOWER that number is, the better, therefore the higher the ratio of cash and equivalents and non-debt liabilities to total assets is, the better. I use this as one of my factors in my ranking system and it has improved results greatly. I don’t understand exactly why this works, but it does; I suspect it has something to do with the ability of companies to sustain growth.

Warren Buffett’s idea of “float” in the insurance industry is precisely tied to non-debt liabilities, which function, in that industry, much like cash for investment purposes. I do not know much about this, but I suspect that non-debt liabilities can be a very good way to fund a company’s growth–a much better way than debt.

Note that I already make use of Operating Assets. I look at what Stephan Penman (in his book “Accounting for Value”) calls “Return on Net Operating Assets”. I look at the (Net Operating Profits After Taxes) / (Net Operating Assets) ratio, which should correlate with your proposed measure of (Net Operating Assets) / (Total Assets).

As for your 2nd point, I don’t invest in financial companies as I don’t know how to value them but maybe one day I will. I don’t have too rosy views of financial companies, so I’m happy to stay on the sidelines.

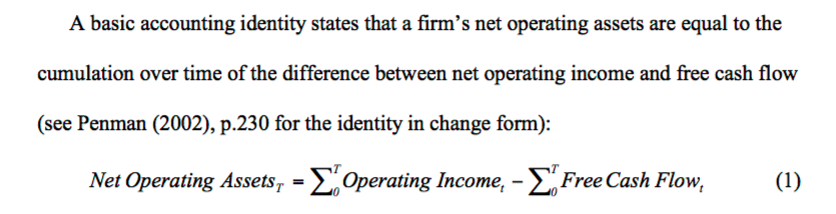

Note that I’ve started reading the paper - it seems that they have gotten the operating assets idea from Penman!

I think the authors’ thesis is that high net operating assets are indicative of high accrual earnings, which are “bad quality earnings”. Nothing here would indicate that pension liabilities are good for a company.

They seem focused on things like receivables and deferred revenue, which could indicate accumulation of accrual earnings that don’t convert into future cash-flows. See the attached screen shot.

But perhaps more to the point, I wonder if what they are measuring can be measured with an accrual-to-cashflows ratio or some similar earnings quality measure.

I thought too about the idea that when a company slowly accumulates funds for its pension that it is creating a ‘float’. But the more I thought about it, an insurance float MAY be paid out whereas a pension float MUST payout. I think that Buffet is essentially gambling that his insurance float will not have to be paid back out in a large chunk, like from a major disaster. I read somewhere that the beauty of the stability of GEICO’s float comes from what they typically underwrite. I think it is more like autos than large, expensive assets. So it is more incremental and predictable.

So having just written this, maybe a pension fund is like Buffets float. It is not all paid at once and is predictable. Except when you declare bankruptsy…and then it just goes to the Pension Benefit Guaranty Corp (if they belong).

By the way… By the way… I’m getting lost in the details here… BUT…

The paper is about how accruals such as receivables as operating/current assets or deferred revenue as operating/current liabilities might increase net operating assets. But the liabilities the paper discusses are all CURRENT.

The paper says nothing about how NON-DEBT NON-CURRENT liabilities might effect a firm - or whether these should be counted as DEBT or OPERATING liabilities. Or am I misreading something? I’ll have to read the paper more throughly to understand.

When we count NON-CURRENT NON-DEBT liabilities as OPERATING liabilities, the NET OPERATING ASSETS (NOA) decrease - therefore (NOA)/TotalAssets ratio decreases. So then the measure (NOA)/TotalAssets is likely to value more highly firms with NON-CURRENT NON-DEBT liabilities, as opposed to those who don’t have such liabilities.

I still think that there may be a merit to the view that all NON-CURRENT liabilities should count as LONG TERM DEBT.

Update: And thanks to Marc’s suggestion, I discovered that Delta has non-current other (than debt) liabilities of 17B. It’s not looking so cheap anymore. And just for reference, Delta’s long term debt is 7B. Perhaps just the fact Buffet purchased DAL is a good enough reason to buy some but if you count the debt as 17B + 7B, it may not be so cheap anymore.

One of my finance profs pointed me to this paper:

How Do Pensions Affect Corporate Capital Structure Decisions

the Society for Financial Studies

Oxford Journals

See the quote from the CEO of Boeing as well as the pointer to the 2005 Wall Street Journal article.

My professor commented “you can (and many analysts do) add pension liability (sometimes called inside debt) to general debt to calculate capital structure and EV.”

The problem is, we have no way of adding pension liabilities to EV. We can add non-current other liabilities to EV. I tried a couple of back tests doing that but the performance of [ EBITTTM/EV ] as opposed to [ EBITTTM/(EV+NonCurrentOtherLiab) ] was slightly better.

Perhaps, we could just screen out companies with unusually high non-current other liabilities. That’s also worth a try.

Anyway, for now, I’ve just noted this. I am extra careful with companies who have unusually high non-current other liabilities.