Yuval, the odds you quote are correct.

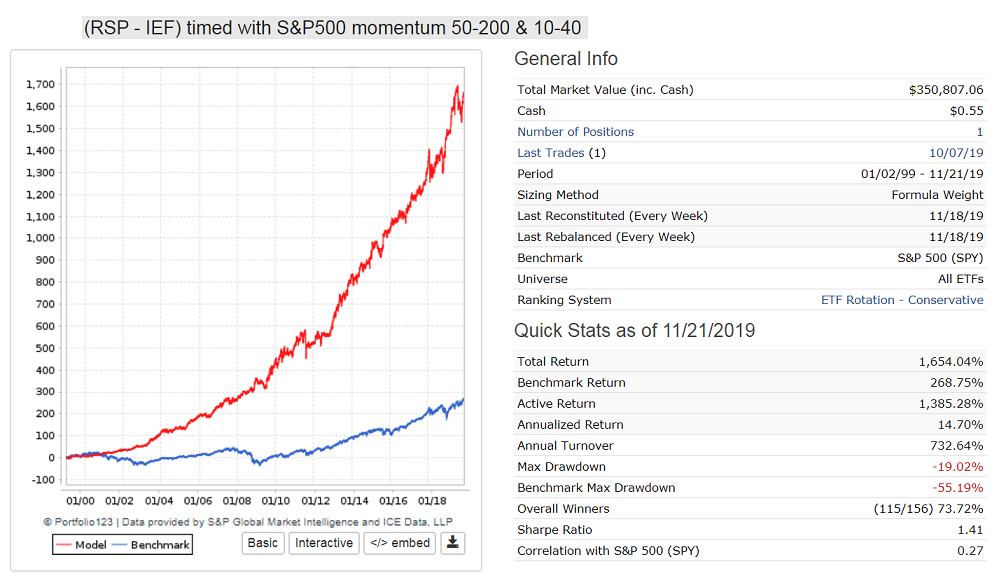

But for people who are not too greedy they can follow a simple S&P500 momentum strategy with equity (RSP) and fixed income (IEF). Nothing spectacular or unknown here. Everybody is familiar with the 50-200 golden cross, and I have added a shorter term 10-40 momentum as well.

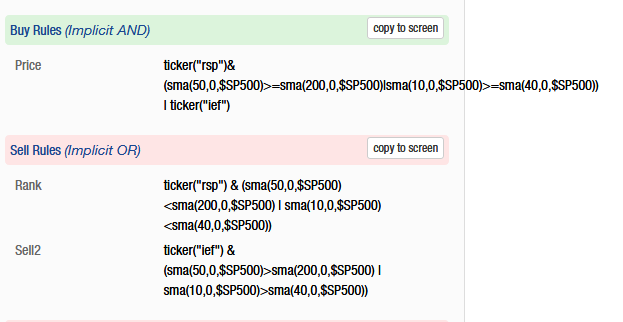

Buy1: ticker(“rsp”)&(sma(50,0,$SP500)>=sma(200,0,$SP500)|sma(10,0,$SP500)>=sma(40,0,$SP500)) | ticker(“ief”)

Sell1: ticker(“rsp”) & (sma(50,0,$SP500)<sma(200,0,$SP500) | sma(10,0,$SP500)<sma(40,0,$SP500))

Sell2: ticker(“ief”) & (sma(50,0,$SP500)>sma(200,0,$SP500) | sma(10,0,$SP500)>sma(40,0,$SP500))

P123 ranking system: ETF Rotation - Conservative

Variable slippage

reconstitution and rebalancing weekly

Weight formula = 1

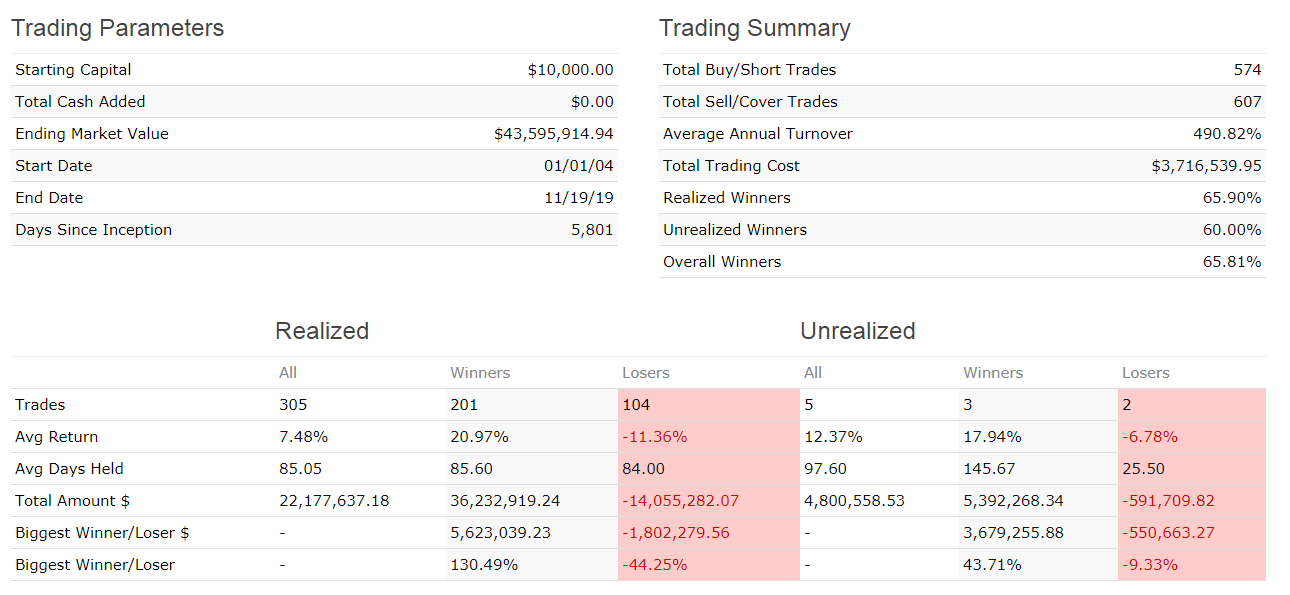

From Jan-99 to Nov-2019 this model shows an annualized return of 14.70% with a max D/D= -19.0% and Sharpe= 1.41.

Standard Deviation 8.73% vs 14.40% for SPY.

It would never have had a loss over any of the 20 calendar years. If one ran a fund based on this simple model you would have made a lot of money, because I don’t know of any fund manager doing better than this. Also there were only a total of 155 realized trades in this 20-year period.

That is why I don’t share the opinion of many that market timing does not work. You can add this model to your Portfolio123 Models lineup, if you wish - it will not disappoint, a lot less riskier than stock-picking.

year … return %

1999 … 6.27

2000 … 14.39

2001 … 11.26

2002 … 14.62

2003 … 39.39

2004 … 12.16

2005 … 17.94

2006 … 15.82

2007 … 10.61

2008 … 24.90

2009 … 16.65

2010 … 13.52

2011 … 3.46

2012 … 11.79

2013 … 33.48

2014 … 8.26

2015 … 11.34

2016 … 8.84

2017 … 15.36

2018 … 11.62

2019 … 11.04