As i am in office, my recent reply was from mobile with typo error and less info, then later i have added more details with exact rules.

I am good with p123 commands. I am curious to know P123 can replicate the performance of ETFReplay.

Interestingly, If I set the sell rule as:

(1)

MonthDay>=28

MonthDay<=5

the results are significantly improved, with the returns being 316.5% and drawdown dropping to only -19%. .

(2)

If I use the sell rule as

Month Day>1 and MonthDay<7, the returns dropped to 45.38% and drawdown -26.42% (yes, not sure why the returns dropped that much).

(LastSellDays > 30) also makes a huge difference.

If I remove this rule from (2), the returns goes back to 278.39% and drawdowns dropped to -28.96%.

In contrast, if I remove this rule (LastSellDays > 30) from case 1, the returns jumped to 360.8% but drawdown decreased to -37%.

I wonder what made you come up with this (LastSellDays > 30) in the first place? If we are to choose the best performer over the 3 months, why do we exclude it even if it has been bought within the last 30days?

You don’t want buy back immediately. So the buy rule will avoid buying.

Keep it as daily rebalance and try in sell rule 28th of every month to sell.

Compare the result transaction by transaction and share the difference to help further. You can take break and continue your research by tomorrow if you prefer.

I have time over the week ends to explore your idea in P123.

===================

ETF dividends are paid into the cash account in portfolios and simulations. We adjust the prices for future dividends in screener backtests to ensure total return outputs in that tool.

Paul,

In my 401k account, I have fidelity mutual funds; the quarterly dividends are automatically re-invested.

Why that option is missing in P123 ?

Long term investors are smart, they know market will go up more than go down, why the dividend earnings need to sit CASH instead of INVEST AUTOMATICALLY WITH ADDITIONAL NUMBER OF STOCKS,

the account can make money immediately on dividend earnings.

Especially, sector investing, and 4 market caps investing need this option to get better compounding effects.

Portfolio123 is about testing the rules, not accurately reflecting histories. Technically, reinvestment of dividends is going to come at an opportunity cost for our purposes.

While this rule will result in Feb with no transaction and occasionally some months with no transaction too (if 30th and 31st are holidays), at least I can very closely produce what can be created in ETFReplay, giving me some comfort about the accuracy of either model.

The interesting conclulsion is that rebalance timing can be important.

Rebalance on month end can have much better performance than other days.

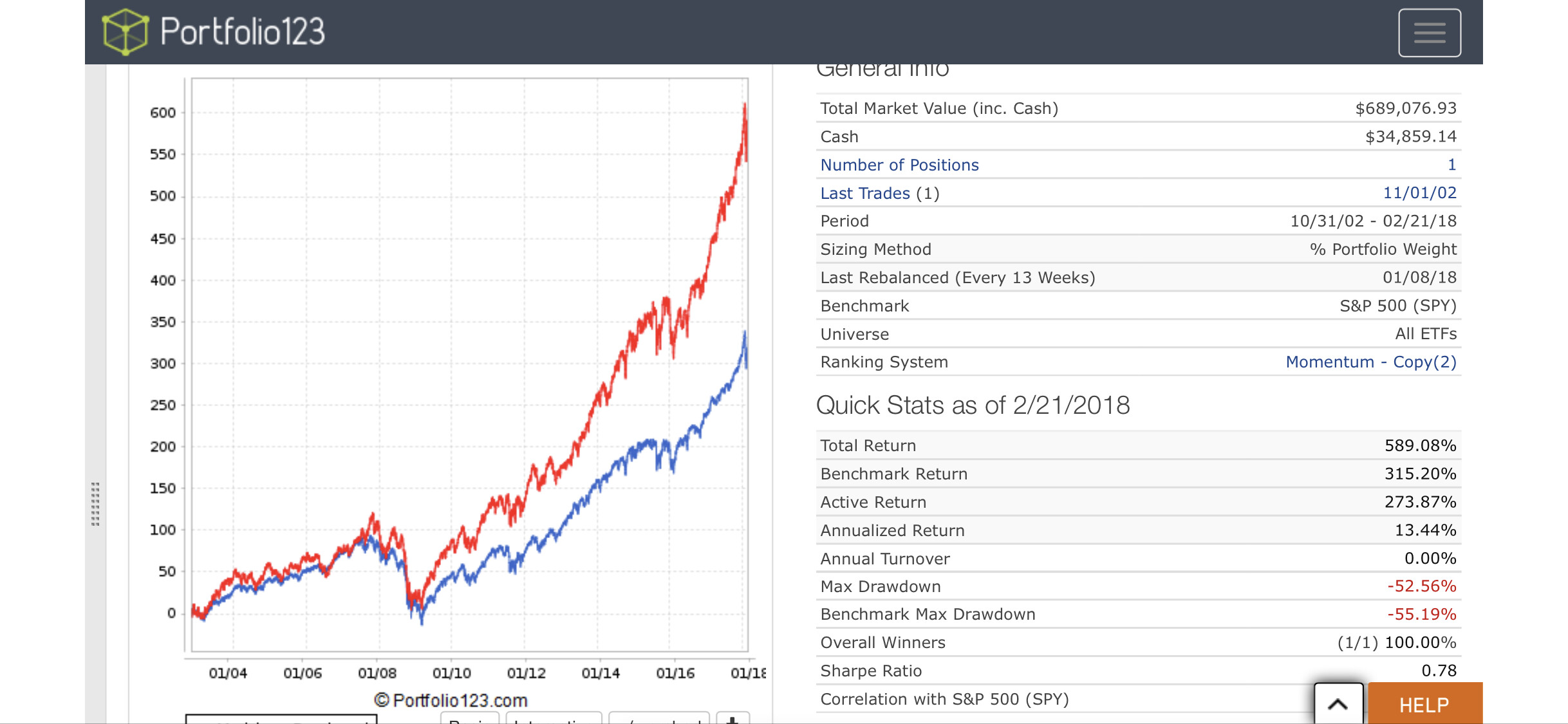

The starting date looks curve fitting for me,

Please, test with 01/01/2002 start date.

I did one testing kept only QQQ etf, it returns 600%.

If market goes-up most of the ETFs goes up. Please, use price, volume, macd and OBV in P123 to get some edge rather than using only price.

We never know, you may be a great ETFs model developer if you have spend more time with p123 and replicate the professional TA insights with ETFs.

This should not be surprising. The beginning and end of months are known to be statistically more significant and have seasonal importance. That’s one of the reasons I’m disappointed P123 has not improved date timing and bar counting functionality.