Jim,

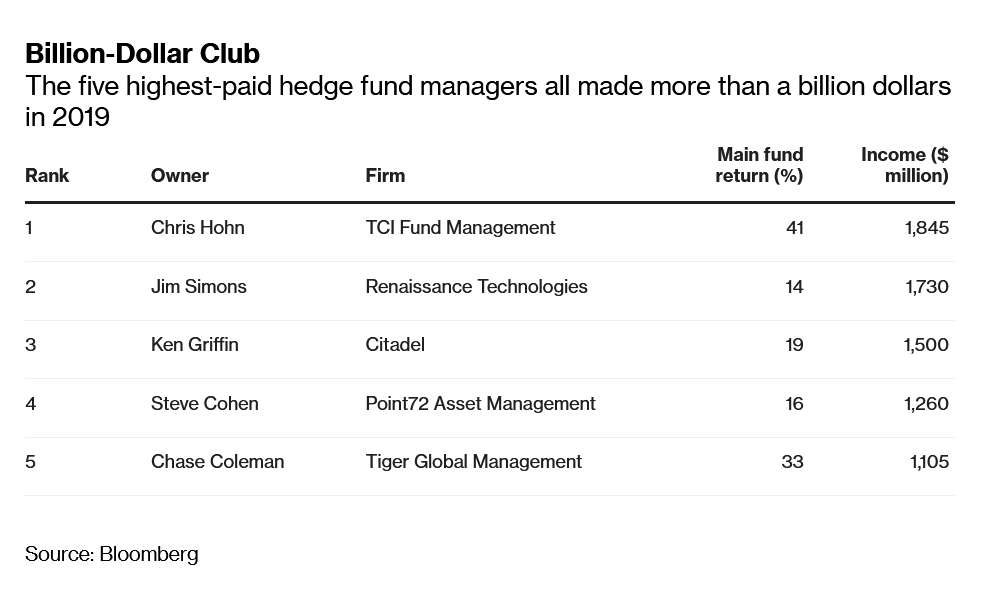

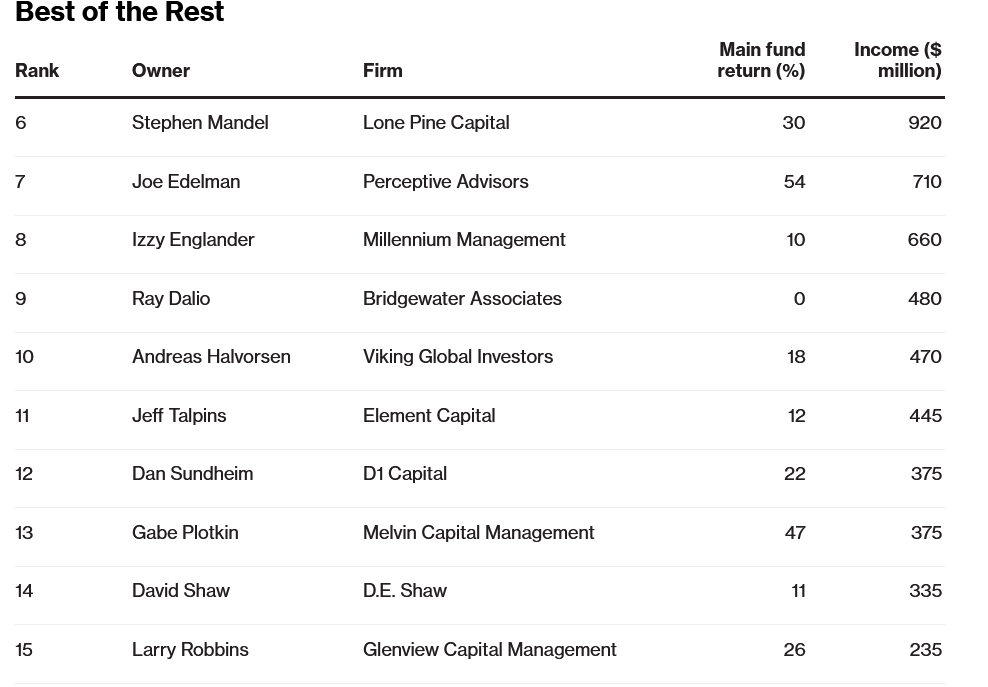

It pays amazingly well to be a top hedge fund manager.

This is how much the top 15 hedge funds managers made for 2019 and the performance of their flagship funds.

Regards

James

Jim,

It pays amazingly well to be a top hedge fund manager.

This is how much the top 15 hedge funds managers made for 2019 and the performance of their flagship funds.

Regards

James

James,

And much of that income is taxed at the capital gains rate using the carried interest tax advantage.

What I find most interesting in what you present about the hedge funds is that the top 2 funds–Bridgewater Associates and RT–make VERY HEAVY use of stock correlations.

A topic you are interest in. I can see why.

Best,

Jim

Jim,

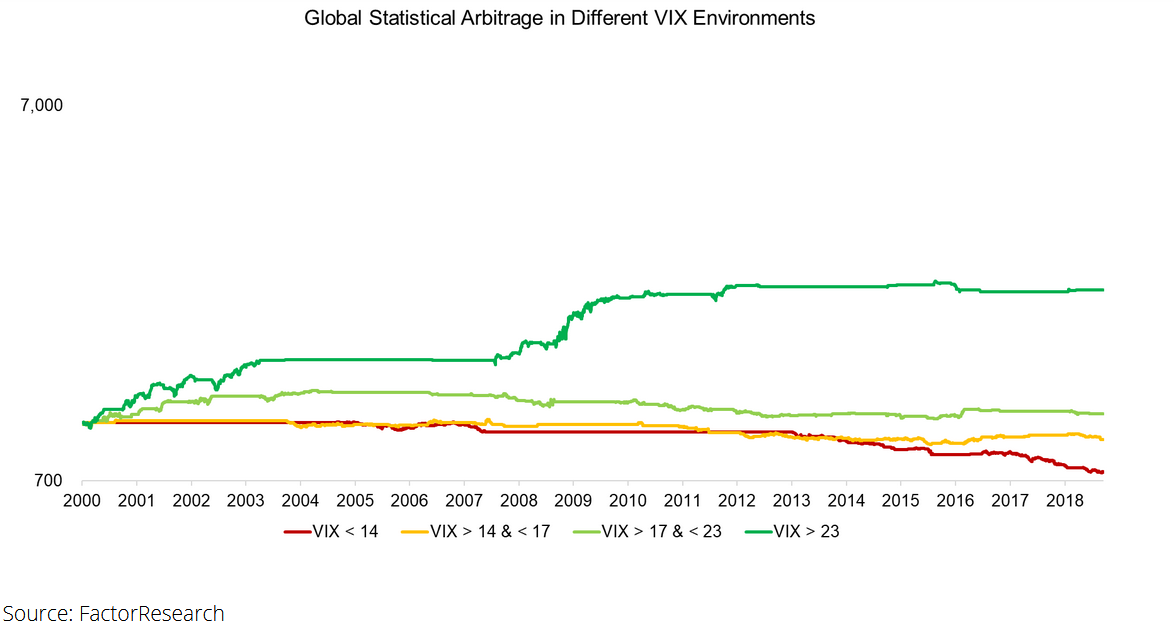

In order to understand how the Medallion Fund racked up 152% return during the financial crisis in 2008 when S&P plunged 37%, I run a check of their Stat Arb (pair trading) operations which makes up the majority of the fund’s return and found the followings :

The profitability of pairs trading strategies: distance, cointegration and copula methods

Abstract

We perform an extensive and robust study of the performance of three different pairs trading strategies—the distance, cointegration and copula methods—on the entire US equity market from 1962 to 2014 with time-varying trading costs. For the cointegration and copula methods, we design a computationally efficient two-step pairs trading strategy. In terms of economic outcomes, the distance, cointegration and copula methods show a mean monthly excess return of 91, 85 and 43 bps (38, 33 and 5 bps) before transaction costs (after transaction costs), respectively. In terms of continued profitability, from 2009, the frequency of trading opportunities via the distance and cointegration methods is reduced considerably, whereas this frequency remains stable for the copula method. Further, the copula method shows better performance for its unconverged trades compared to those of the other methods. While the liquidity factor is negatively correlated to all strategies’ returns, we find no evidence of their correlation to market excess returns. All strategies show positive and significant alphas after accounting for various risk-factors. We also find that in addition to all strategies performing better during periods of significant volatility, the cointegration method is the superior strategy during turbulent market conditions.

Apparently, there is a strong positive relationship between stat arb (pairs trading) profitability and market volatility. If we differentiate market volatility by VIX quartiles. Given that the VIX is mean-reversionary in nature, there is no significant look-ahead bias in this analysis. It was observed that statistical arbitrage generated only positive returns when the VIX was above 17 and most profitable when VIX is above 23, which represents high levels of market volatility.

Due to the high level of VIX we are experiencing now (almost 50), it is really a good time to try out Stat Arb/Pair Trading. Unfortunately as I have mentioned before, stat arb it is extremely mathematical including python/coding and I can’t do it myself.

I hope you will re-consider investing in this strategy so that I can join in :-).

Regards

James

James,

To invest in pairs I would have to invest using money my wife and I have in the bank.

Interestingly, I was talking to my wife about it (in a casual not planning manner) and she instantly got it!

My wife usually understands nothing about what I do but she immediately said: “Why don’t you do that?” She understood pairs trading.

I will definitely think about it but I think it is unlikely that we could realistically invest much time or money in this project now.

Thank you for your confidence.

Best regards,

Jim

Jim,

I don’t need to check with my wife on this but my intention is to start small in the beginning with the stat arb/pair trading project. I don’t expect to make a huge amount from Day1.

However iIf you are really confident, I can re-allocate some of my investments which is now fully invested in GLD/TLT (50/50) as I have mentioned before.

Regards

James