I should add that designer models all use the variable slippage setting, which is extremely harsh on microcaps. If the daily dollar volume is less than $50,000, the slippage is a whopping 5% per transaction, and if it’s between $50,000 and $100,000, it’s 1.5%.

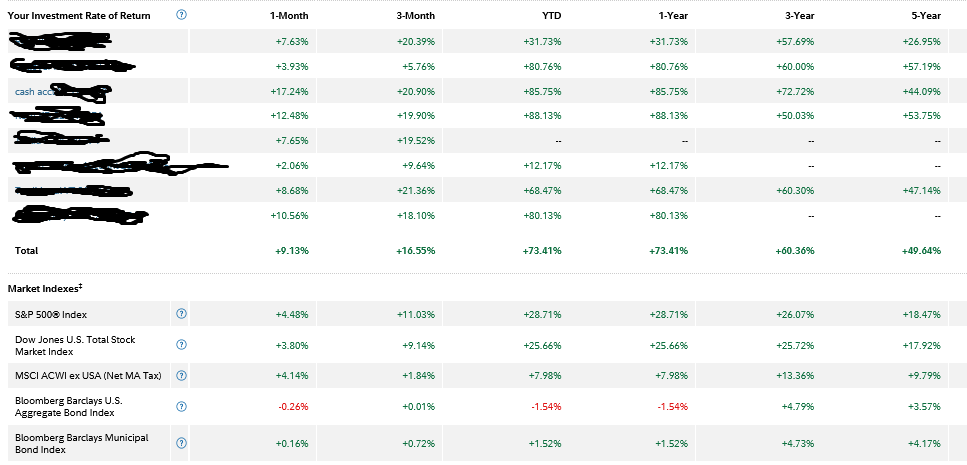

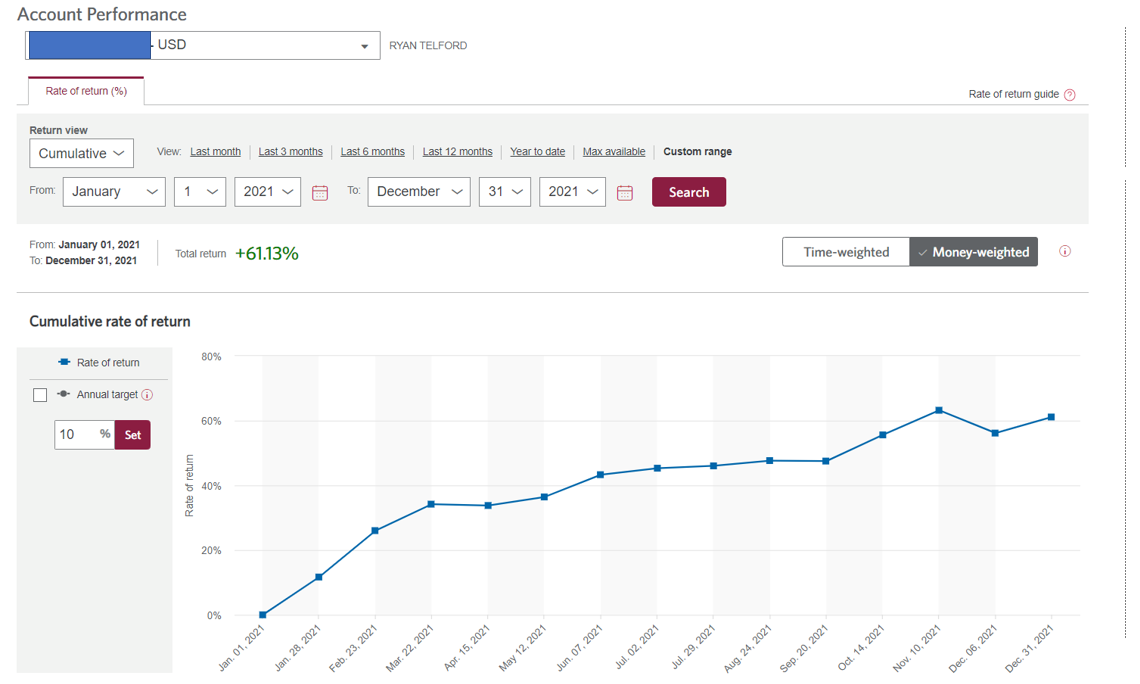

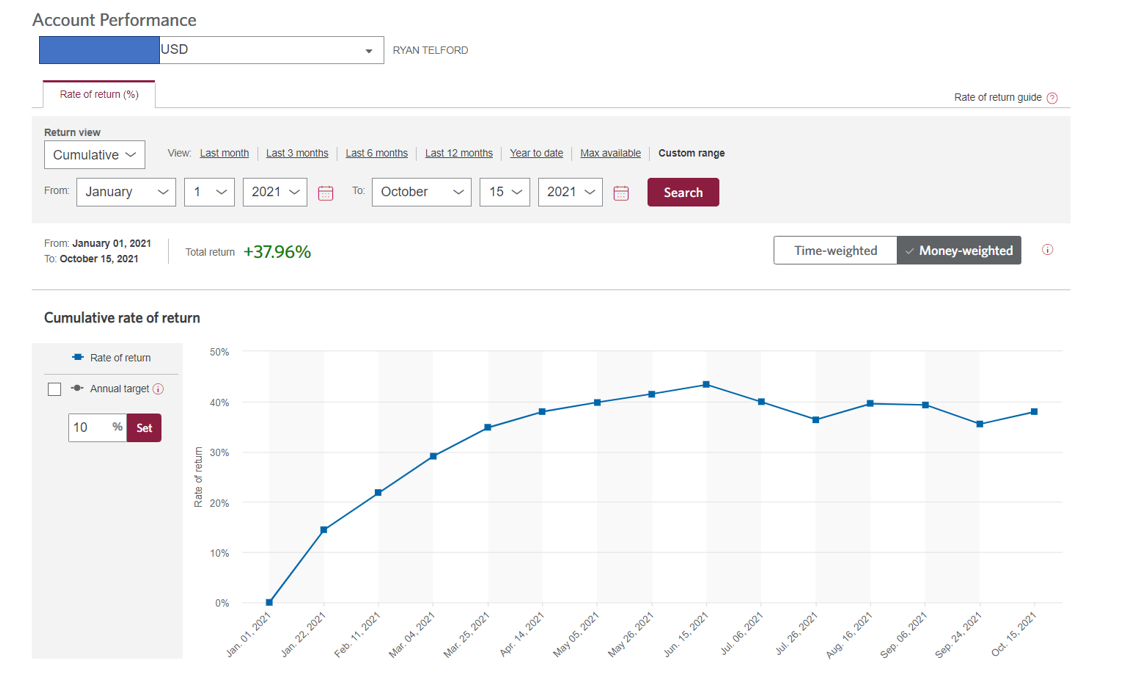

How’s this for “proof”? It’s a screenshot from Fidelity with the account numbers blacked out. All the figures are as of 12/31/21 and are annualized. The “Total” line is the pertinent one. Also I use some margin in the cash account. My margin debt right now is 14.5% of my total funds.

Yuval, Dan and Azouz too,

Thank you for the very significant amount of additional, good data.

Best,

Jim

Yuval,

Thanks for the screenshot and letting us know you trade in margin.

Without leverage, the return is closer 60% from my calculation. (the return is similar to your “crazy return microcap designer model”)

This is still 1/3 lower than the 100%+ return that was stated from trading small caps/microcaps with P123.

I will highlight again that there are hedge funds, mutual funds and actively managed ETFs that play in this space.

Regards

James

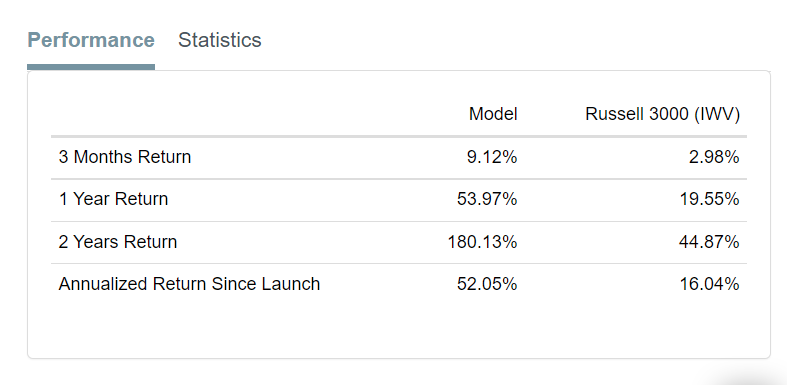

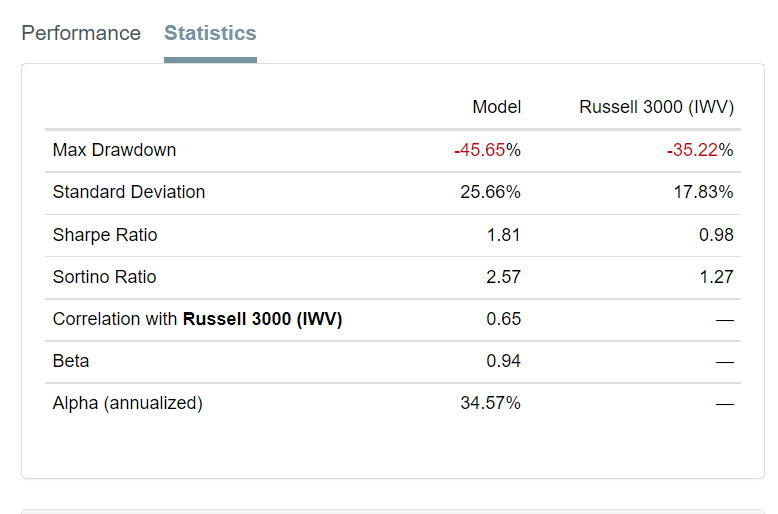

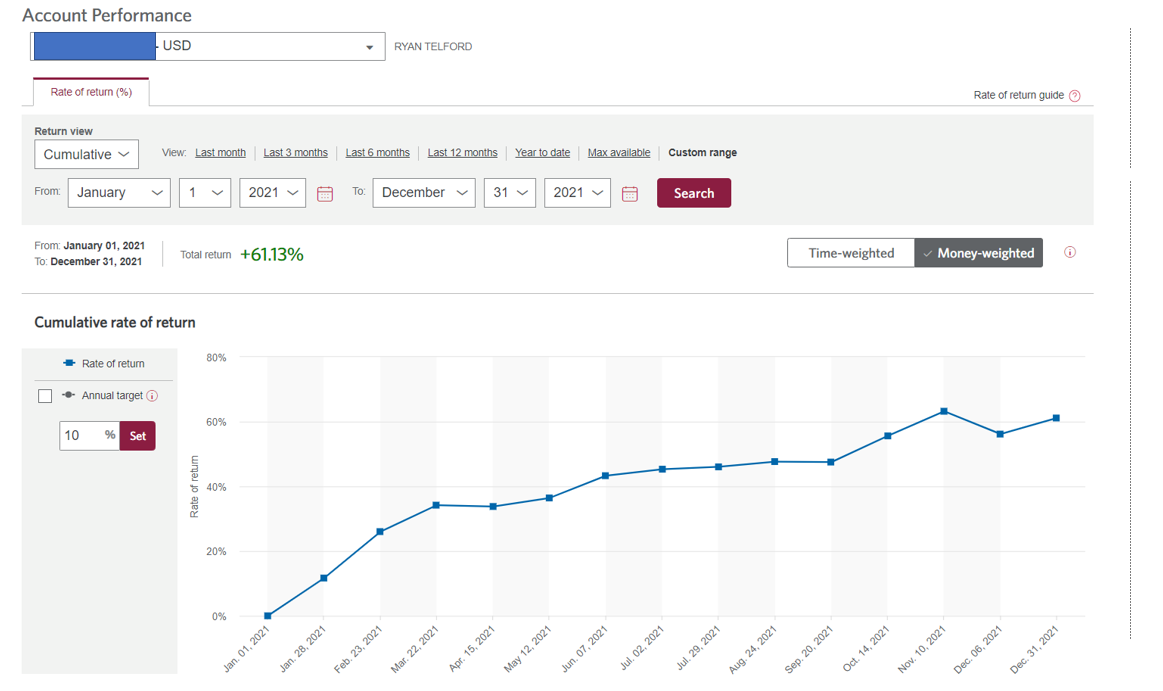

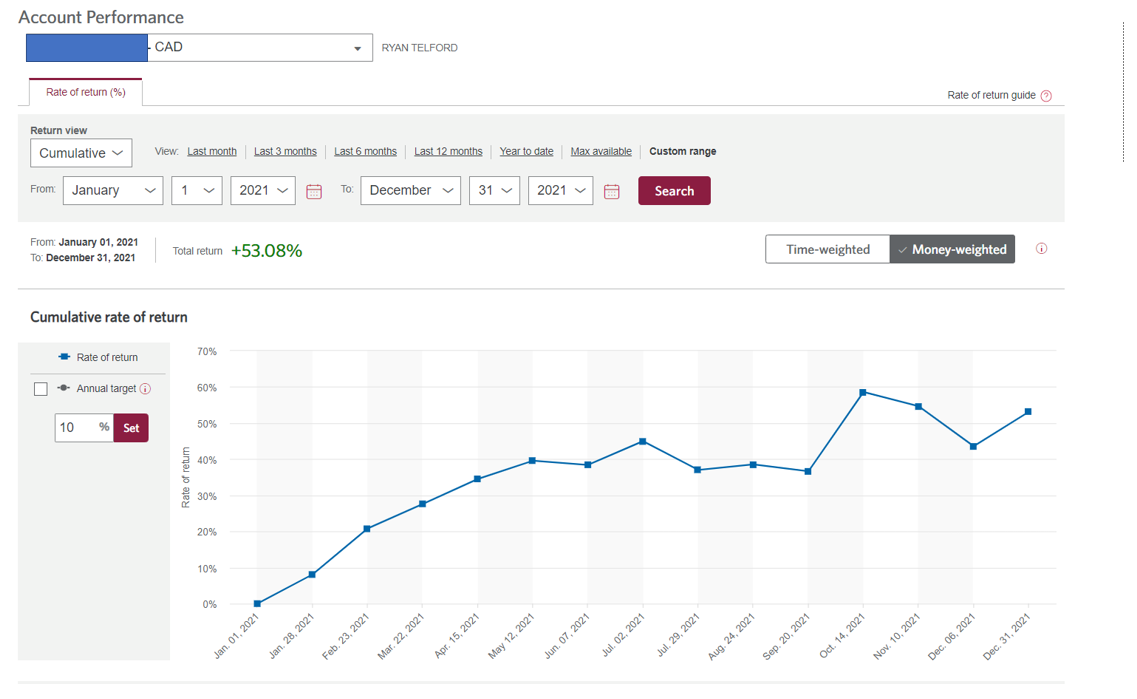

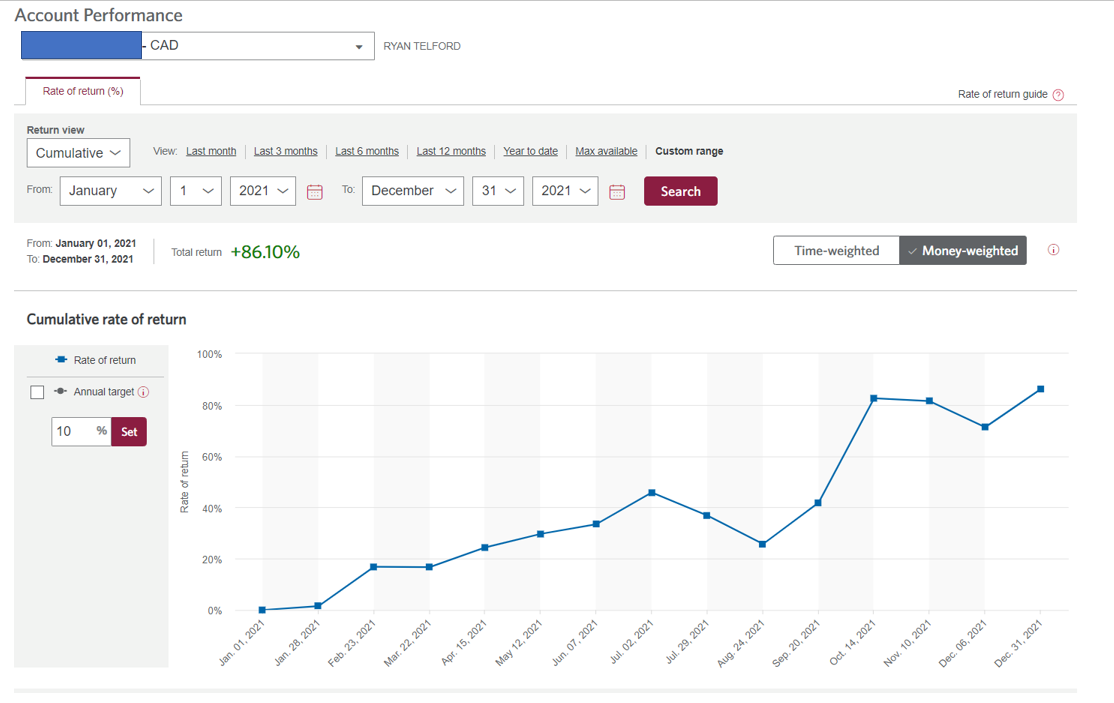

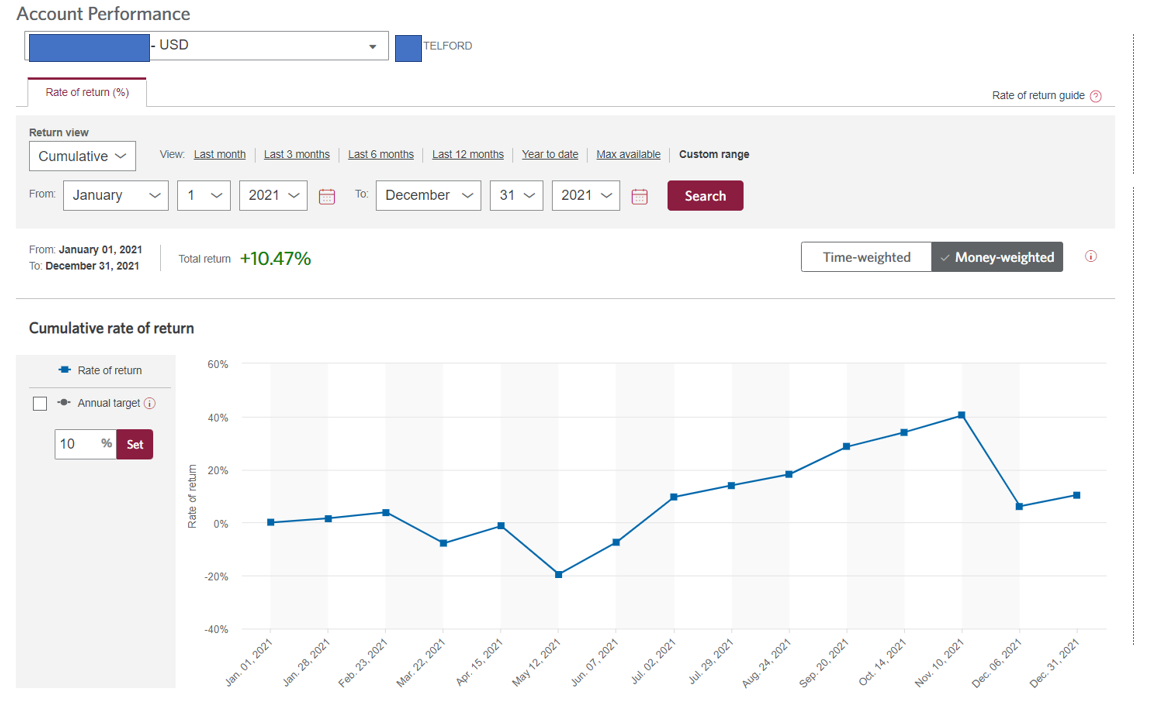

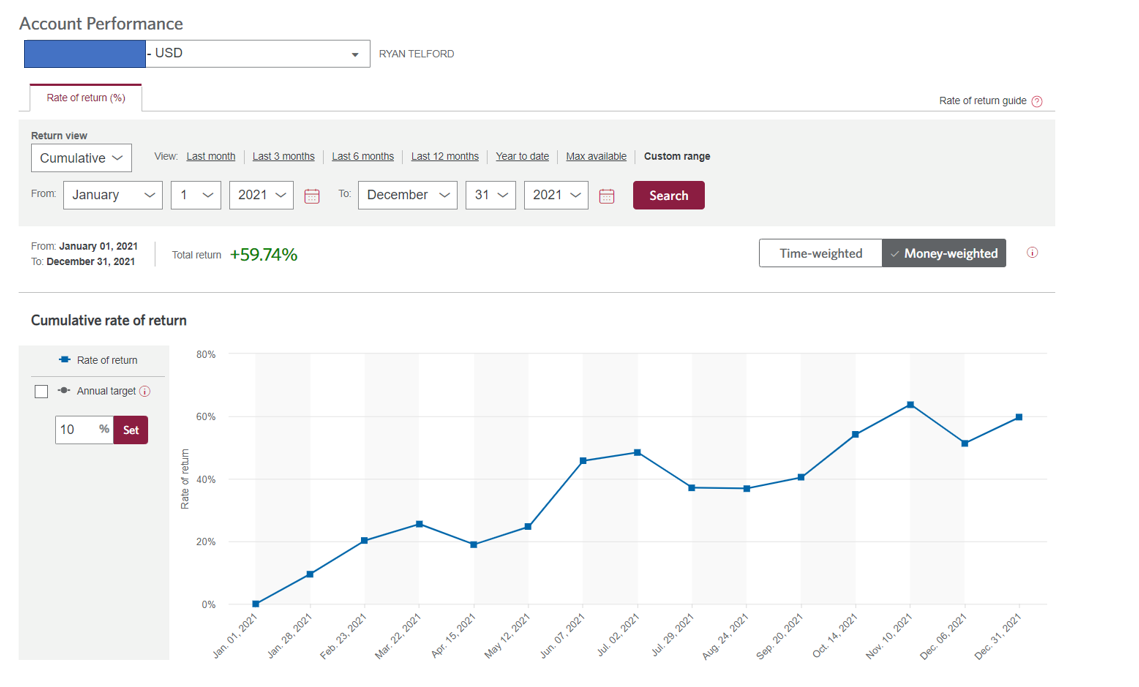

OK, here is performance from my bank(s) as well. Descriptions of each account/strategy in the pic filename. Blue rectangles hide account numbers. ** EDIT - first pic is incorrect, but cannot delete. Correct pic added at bottom.***

No. The return on my positions alone–without considering leverage or cash–was 70% in 2021. I never said it was over 100% in 2021. It was over 100% in 2020. I have never misrepresented my returns to anyone. I underperformed the market significantly in 2019 and have never hidden that fact.

I don’t want to rain on anybody’s parade and perhaps the results quoted here are real. But the stock-picking contest is the only mechanism other DMs that are truly verifiable. Someone can correct me if I’m wrong but there were close to 20 stock-picking entries in 2021, of which 9 were still around by the end of the year. The results are shown below (to today’s date).

These are the returns from last year Steve. I was the lucky winner

https://www.portfolio123.com/mvnforum/viewthread_thread,12652_offset,70

I appreciate Yuval, Azouz, Ryan and others sharing their brokerage statement proofs. None of them were obligated to. Maybe we can all learn from them ![]()

I appreciate all of the new data. As far as pure volume of data nothing comes close to what Dan presented.

Before that we had the Designer models only (with some anecdotal stories). BTW Marc’s median model is performing at the benchmark he selected (with serious survivorship bias). Likewise, Yuval’s median model is performing at his benchmark. The average designer is doing worse.

Another fact that has been proven beyond any doubt whatsoever by the Designer Models is that, for the average user, in-sample sim results are negatively correlated with out-of-sample port results. For most situations, sims cannot be used to support a strategy. Not in isolation anyway.

That is the objective evidence we had up until now.

Surely there must have been other hard evidence upon which to make a decision about where to place your retirement funds? Well, P123 has a pop-up ad that suggests you can earn $1,000,000 at P123.

I totally agree that no one should have to show their brokerage account. But no one forced P123 to make a pop-up ad a very large part of the argument to join P123, either.

One could even say that a pop-up ad was THE SOLE BASIS for P123’s argument to join until now considering the Designer Model’s performance.

Now, I have new data that probably changes my opinion. I was probably going to leave in April before I got some new data in this thread. That was uncertain but it is absolutely true that I have no funded P123 models to share in this thread.

If I stay it will be largely because of the volume of data that Dan presented. BTW, he did that with no one asking him to and he obviously has an understanding of what constitutes real evidence. He has no pop-up ad that he might want to consider documenting.

IMHO, there is nothing wrong if anyone wants to see documentation of what has been almost the sole argument for joining P123 up until now. No one forced P123 to use a pop-up ad. Considering that they decided to go with the ad the only surprising thing is that they did not present some evidence for that a long time ago.

And some profession sites might have chosen to present something like Azouz did with volatility metrics and a Sharpe ratio if they were going to advertise a portfolio in a pop-up ad.

IMHO, it would not have to involve personal accounts but P123 might consider continuing to make a serious (professional) case for joining (and staying at) P123 as Dan has done in this thread. I do understand that when they were started, some thought the designer models would serve that purpose.

While not a shining example of how it should be, Zacks does make an attempt to validate its claims about Zacks rank without trying to imply they should not have to do so. But it would be true: They don’t have to do it. I don’t think there would be a Zacks today if that had been their approach, however. Certainly, I would not have visited their site more than once (if at all). As it is, Zack have gotten some money from me over the years. Largely based on some documented out-of-sample evidence.

Uh… Maybe that is an exaggeration. Zacks also markets to professionals and maybe the professionals funding Zacks operation don’t want to see any objective evidence that using Zacks’ data has the potential to improve their bottom line. Could be just me but I do not think so.

Best,

Jim

You are right on many points, Jim.

And many of us who have had some middling success with P123 do not know if the OOS results are going to last, so do not share. Also, AFAIK IBKR may be the only broker to compute Sharpe’s and Sortino’s on individual accounts.

For me P123 is also a data source to look at fundamental data, Not just a simulation engine. But equally good data is now available on many sites like TIKR or ROIC.AI. I wish we had more line items for marketing, SB comp etc.

To be fair, sites like Validea.com which also run algorithmic models have had marginal success with their strategies. Maybe there is value add in P123 adding such models?

Congrats to you and those that enjoyed great results last year. Value strategies are the place to be right now. I remember a year ago everyone here was lamenting that quant and value were dead. What a difference a year makes! Unfortunately, growth stocks (my specialty) are in a severe bear market and will probably remain that way for quite some time.

Inspector Sector,

Respectfully, you omitted at least one entry in the stock picking contest of 2021 (myself) as documented here, with a return of 18% and a sharpe of 1.33: (Probably because I named my port “Yearly Contest…”)

https://www.portfolio123.com/app/screen/summary/191518?st=1&mt=1

Incidentally, this proves that at least one value strategy was not “dead.” (More specifically, my strategy combined Low-Volatility and Reliable Dividends)…

Steve G

Hi Steve G - It doesn’t look like you followed the conventions that were asked for, and screens are easily modifiable ![]() But anyways, 18% is a good achievement, so congratulations on a good year.

But anyways, 18% is a good achievement, so congratulations on a good year.

deleted.

All,

To be clear I think Cary is not talking about me. I was nothing but complimentary about Azouz’s results for example. I could rightly be accused of being a Gushing Fan-boy but not of questioning his data. I have had the opportunity to email Azouz in the past and I have nothing but admiration and respect for him. I was similarly complimentary of Dan sharing his results I believe. Yuval’s results have been well verified in my opinion. And to be completely clear, I believe them.

Cherry-picked and anecdotal results can be factually correct but misleading. Unless you can read minds you never know what is intentional.

Unless they tell you what they were thinking that is. Let me confine the rest of this to the honorable profession of medicine.

There is a famous ophthalmologist that you probably could be reminded of from TV or the news whom I worked with at one of the Universities. He has published (and been on TV and in the news).

I would not describe it as admitting to cherry-pricking but rather as simple bragging. And a big joke among colleagues in the know. I am still not able to mind read but perhaps I got a glimpse of his possible intentions through his words

His published paper described a “continuous series” of n patients and their surgical results.

His brag was about how the now blind n + 1 patient in the series had done (and his leaving that out). He had purposely selected the series he published. He was well aware of the poor result for the n +1 patient. His paper was accurate.

I could give endless examples of p-hacking (intentional or unintentional). But adding to the sample until the results are “statistical” is like making coffee in the morning for some. Part of the job if you want to keep your NIH grant and become a full professor at the Universty.

You might look at the Science Paper with my name on it (I was a student at the time). There is removal of data in that paper and a big debate about the removal occurred at the time. I am honestly unclear of some of the details except that that PhD thought that the data should not be removed. Needless to say he did not get a humanitarian award for sticking to what he thought was ethical. He was fired instead.

Could someone please check whether the statute of limitations is up on that? BTW, I am taking a cold medicine and my thinking may not be clear as I write this. Seriously, I forget some of the details and there could have been a footnote about the data being removed and the reasons for it for all I know (or remember). But I am sure that there was at least a hint of p-hacking that the PhD did not like and he wanted to withdraw the paper before publication. But I cannot say whether he or the lead investigator was right at the end to the day. I just wanted my name on a Science paper for my CV and I was probably looking at the lab-tech when much of this occurred.

Not that I think that kind of thing ever occurs in finance.

I do see a lot of survivorship bias in the Designer Model. I am not claiming this is an ethical issue as I would remove models that were found to s*@k out-of-sample myself. Hmmmm…I have work in medicine as a doctor and a researcher (with an NIH grant). You might question any series of returns I present to you in the future. Just saying.

Best,

Jim

Jim - I think you are safe ![]() I’m sure the medical profession has bigger things to worry about when it comes to research studies.

I’m sure the medical profession has bigger things to worry about when it comes to research studies.

https://www.cbc.ca/news/health/covid-19-vaccine-study-omicron-anti-vaxxers-1.6315890

Steve,

Thank you. That is clearly what one does (whether it can be justified or not). Keep adding data until it shows what you want. Then stop if the next set of data muddies the picture you want to present for your next grant (p-hacking).

That is what the NIH was paying us to do (sometimes). I do not want to hide data myself. There was a researcher (MD, PhD) who would have me call patients long after the study was over to make sure their condition had not changed. And would have withdrawn any study in a heartbeat with any new information.

But thinking abut it, we had an animal study where one group (of mice) died after 2 weeks due to a GI infection that went through the facility. Solution, switch to study of a 2 weeks study and keep those mice in the study. That is technically p-hacking.

BTW, I can absolutely guarantee that no herpes virus samples ever escaped from that lab. The infection control was perfect.

Best,

Jim

Jim - I have turned into a cynic in my old age. That is why I brought up the 2021 stock-picking contest results. As for Covid, I am pretty much a cynic about big pharma and the push for patentable vaccines. (At last count, there have been 40 billionaires that made their fortune on vaccines and testing.) There is some evidence out there (I’m struggling to find it now) that suggests that too many vaccines against a certain virus cause something called “vaccine mapping” where the immune system believes a mutation is the same as the virus originally vaccinated against and is not effective against the mutation. I know back during the swine flu there were rumors that the people dying were those that had the seasonal flu for several years. I would be wary of having too many booster shots or any for that matter. We may be doing more damage than good…

Azouz, congrats! Can you enlighten us more about your investment philosophy, and what criteria have you found to be useful in building your models? To the extent you want to share, of course.

You are on to something here, Jim. There is a serious replication crisis in factor research that is well documented. And what works may never get published too, as some prop shop/hedge fund where they found the anomaly does not want the alpha to decay.