Nisser,

Thank you again for sharing. I think everyone, Marco and Yuval included, thinks some difference between sims and the corresponding ports happens.

Keep in mind that P123 was doing a lot of changes with their data as they switched to FactSet data and these change are a type of revision of the data. A type of revision that has probably gotten much less frequent recently.

But it is just a question of magnitude. FactSet data being what we have to worry about now. Did we start using FactSet data in June?

No ports were using FactSet data before June or whenever the switchover occurred.

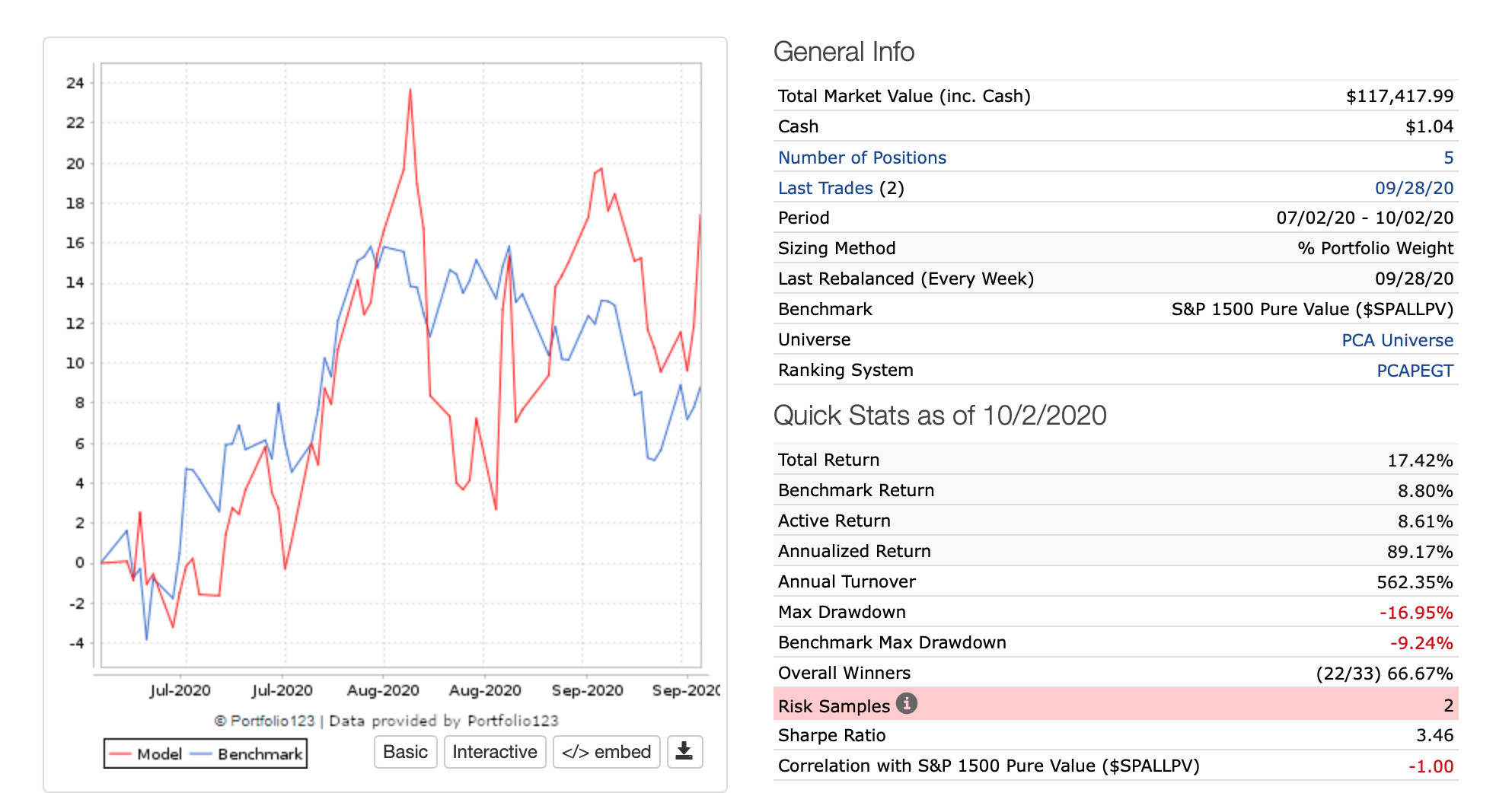

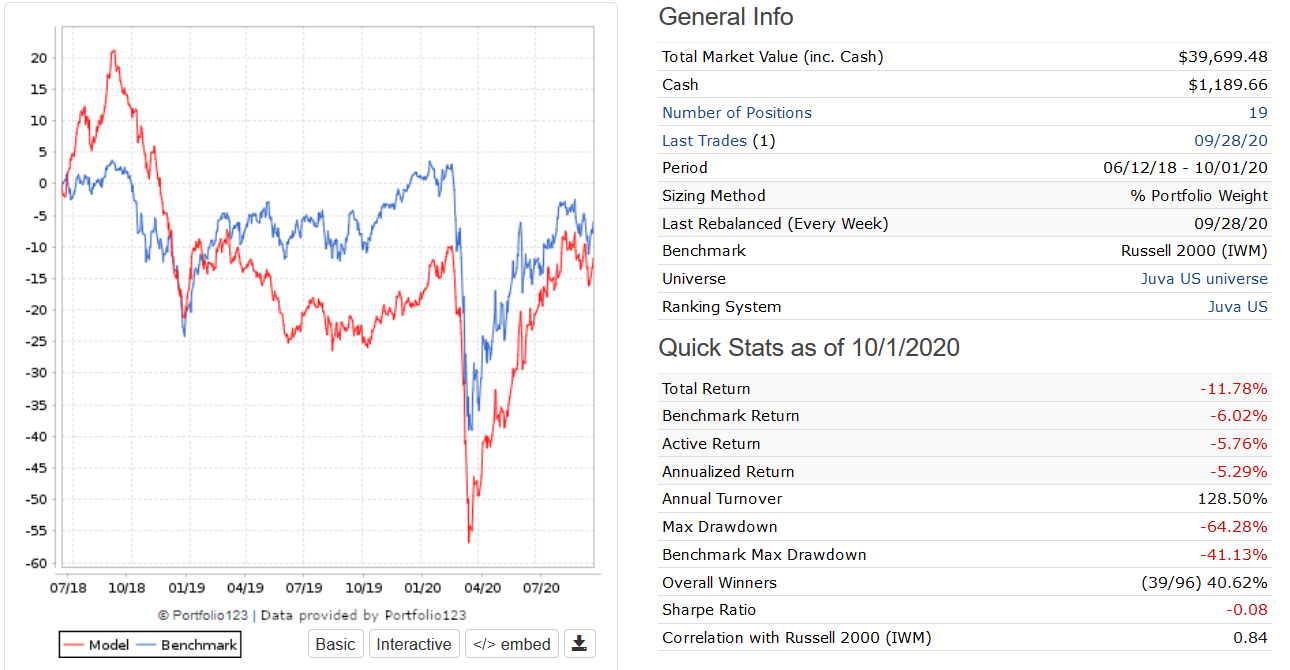

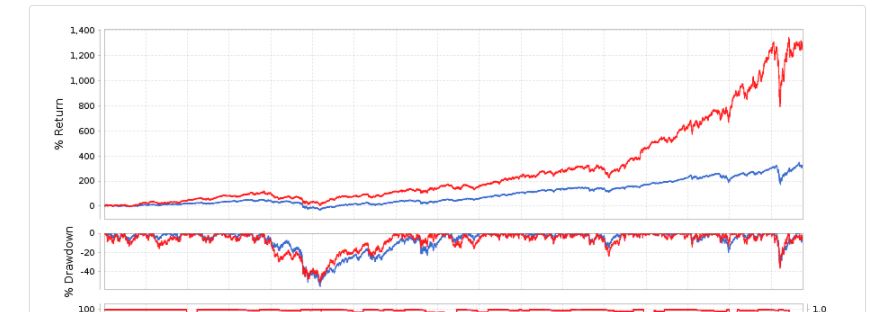

Looking at your equity curves how would you rate the difference between the sim and the port since we started using FactSet data?

By rate, I mean Bad Problem? Not too bad? Or not much data and over a period when the way P123 was handling data was changing?

Everyone should make their own judgements. It seems to me like everyone has different tolerances of how much change is acceptable. So I definitely cannot judge for anyone else.

Just deciding on what I will do with my own investing: I will not be switching to CompuStat data based on what I have seen so far. But I will be looking for more data and information.

Yuval said it could be done. If he is right about that he needs to compare Designer Models to the corresponding sims in six months. Do it over a period when the frequency of changes that P123 makes in the data has declined. Having a small difference between the sim and the port is the most basic assumption to the idea that anything we do at P123 might work.

If we are not confident in the assumption that the sims and ports are highly similar we should probably invest our money elsewhere. We should demand data on this (with regular updating) to make sure we are not making a bad assumption.

Yuval asked me to remind him so that he could implement this idea.He said he liked the idea. I have marked it on my calendar. [color=firebrick]If that will not work for P123, I think we should hear it now. Preferably there would be some explanation of why any outliers are doing what they are doing so we can avoid being an outlier with our personal ports.[/color] I do think I will still be here in 6 months and still be using FactSet data as my default position (null hypothesis) is that the data is generally okay and maybe P123 can even identify specific problems and make some improvements.

It would be a simple quality check when you get down to it.

That is DEFINITELY not to say that P123 should’t respond to other member’s ideas and concerns or that this is a settled issue (either way).

This is probably the most important thing. The sims have to have a high relationhip to the ports or the whole exercise is meaningless. The more discussion there is on this topic the better. And every incremental improvement is good.

I certainly hope we do not have to hear people at P123 tell us that look-ahead bias is actually a good thing because it randomizes the data or some such thing. Look-ahead bias is never good. Bias (of any type) is never good. Even in the workplace intelligent people seem to be able to recognize that without a lot of debate.

Best,

Jim