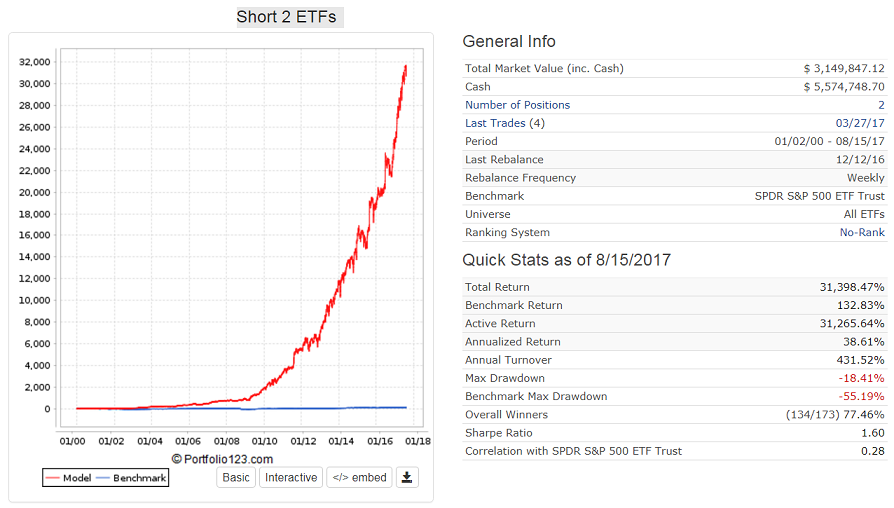

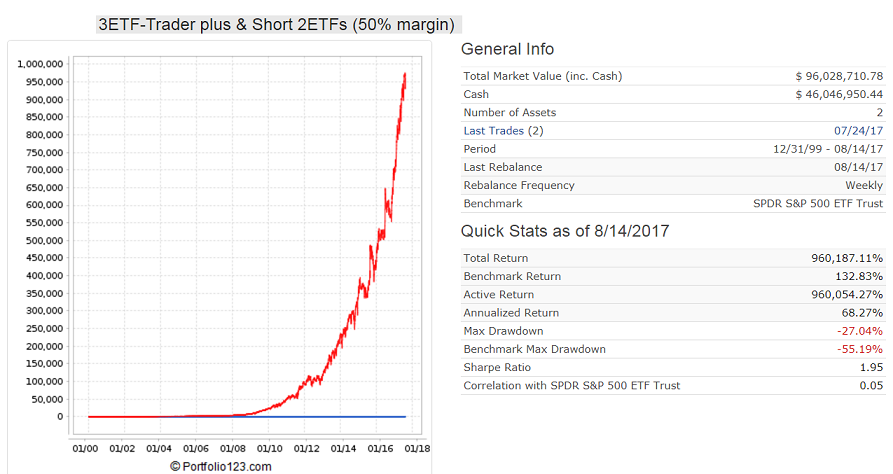

I recently ran across an article in Bloomberg titled, “The Math Behind Futility,” which includes a video interview with Rob Arnott (CEO of $161B Research Affiliates) and a discussion of why 90% of active managers have failed to beat the S&P 500 over the last 15 years.

In the video, Arnott states that the reason that benchmarks are almost impossible to beat by money managers is that there is a positive skew to market indices from a very small portion of companies in the index. It is that small number of companies that are “home runs” that skew the indices higher, not because the average stock is moving higher. If an investment manager doesn’t hold those few companies that are causing the positive skew, the manager will underperform the index. (The same thing applies to us beating our p123 portfolio benchmarks.)

Likewise, there is not a “small-cap effect,” it’s just that the few small-cap stocks that are “home runs,” tend to skew a small-cap portfolio more than a large-cap portfolio (because of the size differential of the basis). Arnott states unequivocally that the average small-cap stock does not outperform the average large-cap stock and also that there are no real “winners” in stock picking when considered as a whole.

I’ve been watching the Value Line Geometric Index ($XVG) for many years and have been fascinated by the fact that it has not set a new high in the last 19 years, even as the major market indices continue to regularly set new highs, particularly recently. The 1,675-stock Value Line Geometric Index gives equal weight to each of its components, while the S&P is market-cap weighted and the Dow is price weighted. The Value Line Geometric Index assumes an equal dollar investment in every security and is rebalanced daily. Geometric averaging provides a realistic representation of how the average stock is performing.

This chart shows the Value Line Geometric index since 1975, with overhead resistance at 510-530 for the last 19 years:

Here is a zoom into the last five years performance:

The challenge we continuously run up against, in attempting to put Portfolio123’s wealth of features to use, is that the regime of the market is constantly changing. It changes throughout the business cycle with a steady rotation of sectors that are performing well. It changes with regard to assets that are the best performing at any given time and many other market and economic factors that regularly fluctuate and greatly affect the stocks in which we have invested (to the consternation of many of us).

Individual stocks used to be the investment of choice, and the consistent selection of good companies at good prices served an investor well. It was, for example, the source of Buffett’s immense wealth. However, today that’s not the case as 70% of an individual stock’s price movements are correlated with the movements of the ETFs that hold it. You can have a sure-fire investment algorithm that is backed with logic from a Nobel laureate, but that doesn’t mean a stock it picks will go up if the ETF that holds it is in a bearish downtrend. Food for thought… and possibly the driver behind the constant flow of funds from active managers to passive ETFs these days.

For me, the recognition of these changing dynamics has meant that I am focusing more time and effort on price and macro factors, rather than fundamentals. Price is the only aspect of stocks or ETFs that is not subject to changes in investor’s focus, appetite or market regimes. An algorithm based on price is not affected by whether an investment is in a declining sector, an out-of-favor market, or any other categorization. An algorithm that works on one investment’s price will work on any investment’s price. Creating algorithms around price also do not force me to be dependent on other investors eventually noticing when the fundamentals of a company suggest its price should be higher, for me to realize a profit.

Chris