Jrinne, we snapshot the estimates every week. They cannot change.

The only difference with live rebalance is if you rebalance before the last data update on Monday morning around 4AM, like Saturday or Sunday, you will get different results than the backtest. A lot of estimate data comes in on Monday morning. Sims use that data in backtests: it’s not look-ahead, the data is available before the market opens.

Marco – I’m getting confused. Your original explanation indicated that if a company’s SEC data filed for a quarter (for example, Q3) is late getting to P123, any analyst estimates subsequently received for Q4 will be posted as NextQ until the Q3 SEC data is posted. For companies in this situation, this would mean that P123 quarterly SEC data is for Q2 and currQ analyst estimates are for Q3 (not Q4). Is this correct?

You are able to keep the misalignment and the problem with the port in the sim. That is good and I stand corrected.

Can you go over a couple of ports and explain why the sim and ports almost never hold the same portfolio of stocks then? I always buy the recommendation. And the sell rule is a simple RankPos > 8.

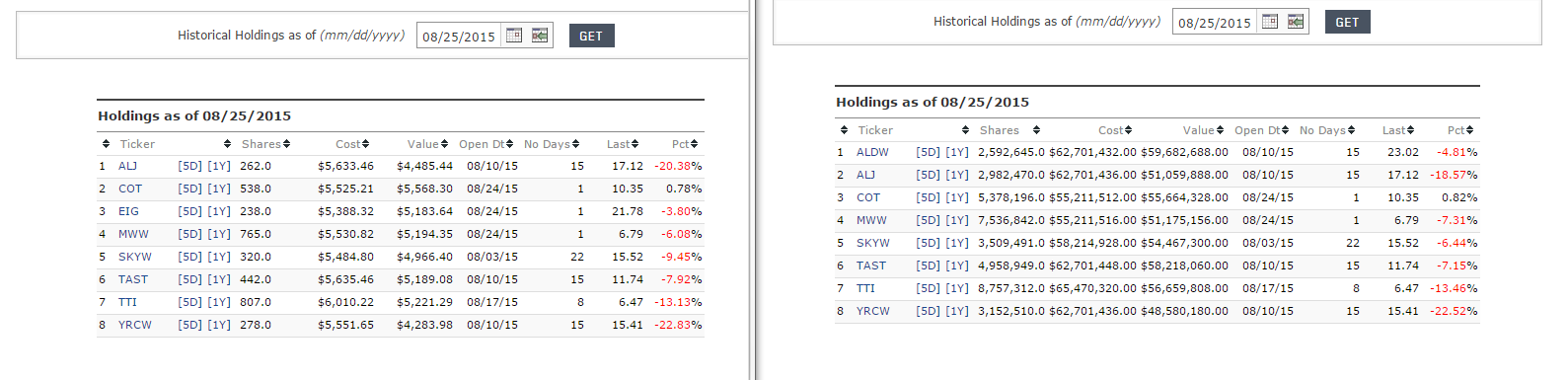

Monday 72 is an example. I did change the amount of cash recently and I get that part.

OK, so if you make the change you are contemplating, in my example, P123 quarterly SEC data would be for Q2 and CurrQ analyst estimates would be for Q4. Correct?

I just converted the port to the sim: Converted Monday 7. Same holdings on that date. There are other discrepancies and I will quantify it in a little bit. Did notice that there may not have been any when I looked quickly at the last couple months the other day.

Marco - these statements are contradictory to what you said six months ago. I was left with the understanding that estimates data was not “latched” and P123 wasn’t interested in doing so, which spawned a heated debate.

Now what is the correct story? Are estimates latched (and thus historically correct) or not?

On reflection, that was one of the rare weeks I used some discretion because ALDW and ALJ are held by the same parent company (or something like that). Confirmation bias on my part. I found what I was looking for.

Also, I was under some old misconceptions from when you discussed estimates with Chaim and others. I thought you were not doing snapshots and I think I looked at some data before you were doing shapshots. It does look like the snapshots are working now to keep the sim and port aligned when I am not using my discretion. I am glad to know that you are doing snapshots.

How far back where you able to go with the snapshots? Are you able to do that retroactively, somehow? If the sims are just beginning to match the ports… Hmmm…

If you get a chance I would be interested in how far back the snapshots go.

Thank you very much. I appreciate your time and your tolerance of all my posts.

Jim, the only reason we have snapshots is to store values that are too time-consuming to re-create when do reloads. Mostly estimate stuff , revisions, and few others. It’s about 100 factors.

Please, if you are here to make money in the stock market (not R2G, fees, or anything else), then this nonsense needs to stop. How can you implement a strategy -- a good strategy -- if every six months or so, Marco, or some other genius changes the way your algorithm reads the data? The point of P123 is, or at least prior to the R2G's, was to create a system that you could implement to make money.

I'm am still trying to do this. I am very happy with my systems and I want to let them work. How about it?

Can we please stop messing with the data? Please!

Your criticism is too general and does not appreciate the many efforts Marco and his team are making to get “clean data” for all of us.

This is a highly complex matter with many issues and not as trivial as you seem to believe.

So it would be nice if I could avoid buying a stock that I though had a recent positive earnings estimate revision, but in fact, had a more recent negative revision for the quarter or year of interest. This clearly happens under our present system. Maybe not too often.

But when it does happen you are probably buying a stock that has had a recent negative earnings surprise and that surprise has resulted in a negative earnings estimates revision. You are completely unaware that this has happened and you buy this stock when you rebalance. How many stocks like that are needed to ruin a port? Maybe it is your fault and you just need to stop over-fitting: it is not right to hope for too much.

One way to avoid this would be to use InList() and put stocks that have only had upgrades in that list using data from another source. A source not limited by fundamental data for timeliness.(Edit:Actually, excluding stocks with a downgrade in the exclusion list is probably better.) You would create a universe of stocks that had upgrades from the other source. Even if the other source has a negative revision because it uses different analysts maybe that is not the best stock anyway.

Not that hard using Excel downloads, copy and paste. One minute.

This may become a moot point. But assuming we might continue what we are doing: Any thoughts?

On further thought, maybe I want people buying a stock that I am unloading. Hmmmm… The R2Gs won’t be able to use InList anyway. I think I won’t delete and if Marco thinks any changes might be an improvement, I will take it. Either way: no longer a problem for me. Well, there is that one minute.

I thought my post was very much to the point. P123 needs to stop messing with the data, so we can actually implement what we test.

What is clean data to one guy is dirty as hell to the next. That is why it may seem complex; it's a morass; I'm not getting into it.

Marco has programming considerations that I do not even understand. I’m sure that he will make the best decision.

However, I am still considering the idea of getting confirmation of estimates data from another source–even if it is because the other source might follow different analysts. If the other source has a negative earnings estimate revision, I would reject the recommendation and move on.

I wonder:

What source are news programs citing when they say a company beat consensus estimates? Thompson Reuters claims: “…most quoted by major media outlets” on their web site. Is this true?

Yahoo uses Thompson Financial Network. Are they a good source of analyst and estimates data?

Does Yahoo update the estimates data in a timely manner?

What are other good sources or souces better than Thompson Financial Network?

Marco, A YEAR AGO I posted this http://www.portfolio123.com/mvnforum/viewthread_thread,8214#42604 in regards to inaccurate OOS performance stats following data “fixes” of P123. I think it was related to the earnings estimates. I simply requested that some sort of notification was put on R2G’s main page alerting us that the stats may be different as of “x” date of data change. And, to put a link to the new stat’s for us to be able to review and compare (leave the old stats also). I was under the impression that changes would be coming “soon” regards to that forum discussion. A year later and with the new “SmartAlpha”. I still do not see/how all the prior data fixes have impacted the R2G’s OOS performances. Again, I would like to see “yearly” OOS stats that include Model%, Benchmark% and max drawdown “per year”. Without this historical information and updated stats as changes are made in the background I am not sure I can make somewhat informed decisions regarding R2G’s. I appreciate you wanting to change things as you see need but we have the right to know how that effected the models. I also need back the ability to “combine” more than 1 R2G to review stats of those combination models like we had in the past.

Question: Will you be able to provide these requests “soon”? I have been paying for over a year waiting.