I was aware of this seasonal SP500 strategy 25 years ago so I believe that it works. There is one caveat however and it applies to all seasonal patterns. The caveat is that if the pattern does not hold for a given season then it will not hold “big time”. This tends to skew stats.

There is one seasonal S&P500 trading strategy that I remember from ~2000 that tried to take care of the above caveat. Basically, you only enter the S&P500 after October 16th when the MACD crosses above zero. I believe that stockcharts.com still carries this strategy but I’d have to track it down.

This doesn’t reduce it’s effectiveness if that is what you are getting at.

The SP500 seasonal pattern reflects the natural yearly business cycle. People take holidays throughout the summer and return for work in earnest in the fall. The business environment can’t truly be evaluated during the summer and numbers (employment, GDP, etc) don’t firm up until the October-ish time frame. And politics (elections) adds to the uncertainty every two years. We start getting a better understanding of how retail is going around US Thanksgiving. and this extends into January. Then we get into quarterly/year-end reports that reinforce the economy numbers previously published. This takes us to mid-April and IRS which marks the start of the summer season.

Generally speaking, October-May is bullish most of the time (70%??) but you should be able to tell how the winter season will play out in October based on Fed Reserve activities and politics.

The most important thing to remember is that issues (trade, foreign affairs, fed reserve actions, etc) occur all of the time and are outside our control. But market sentiment determines market action, not the news items. If there is a positive sentiment, then the markets don’t bat an eyelash with negative news. If the market sentiment is bad then it is like crisis mode even for things we know will blow over in a short period of time. Market sentiment usually works for investors during the winter months, and is stagnant during the summer months.

Steve, thanks for providing some reasons for the seasonality.

It’s not just the S&P that shows this anomaly. A German investor told me he is using futures on the DAX and makes about 10% return from the seasonal effect. In Europe many go on vacation during the summer months. Some while ago when I worked in Barcelona, the town was virtually empty July and August, same for Paris, Vienna, etc., and even the Germans take part in this summer ritual.

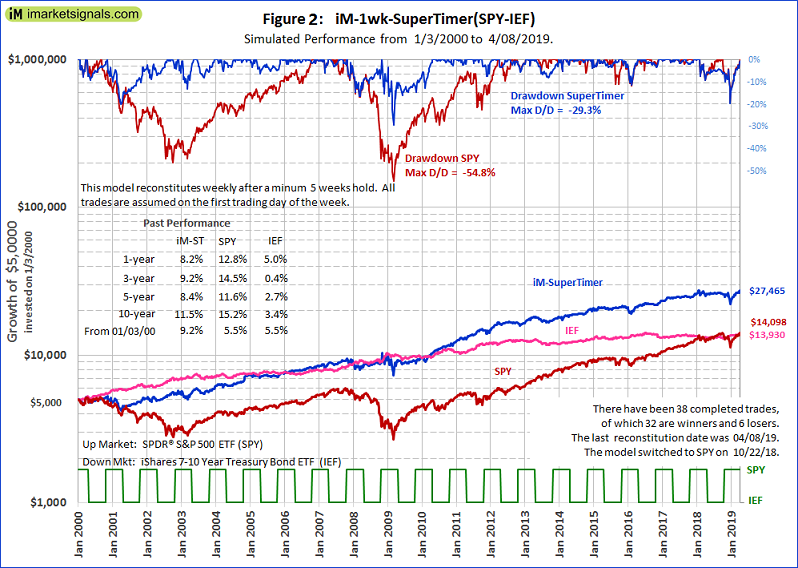

Here is my SuperTimer(SPY-IEF) from Jan-2000 to Apr-2019. For the seasonal switching strategy 14 of its component market timer models were turned off, only leaving the seasonal timer model on. Growth is plotted to a logarithmic scale, and the investment periods for stock fund SPY and bond fund IEF are depicted by the lower green graph in the figure.

For those who are interested, the iM-1wk-SuperTimer with all the 15 component market timer models from its arsenal turned on would have produced $169,692, for an annualized return of 20.1% with a maximum drawdown of -10%. There would have been 45 completed trades, 39 of them winners.