You wouldn’t get the same list of stocks unless you’re using a rather small universe because if you put WeeksIntoQ on its own line with no qualifications it’ll exclude stocks with WeeksIntoQ = 0 or NA, and the stocks with those values for WeeksIntoQ are going to differ between one server and another and between data providers.

Correct.

Yes. Take ACU, for instance. It announced on April 17 and filed on May 8. WeeksIntoQ on Legacy is 3.

Finally had a good chunk of time this weekend to dig into differences in my Strategy Sims between Legacy Engine Compustat and Current Engine Factset databases. I’ll focus on one specific big difference for now since it affect a bunch of my strategies.

I have a risk management rule that is based on economic data and price performance of the index. Buy rule would be as follows:

Eval(Close(0,#UNEMP)>1.1*SMA(12,0,#UNEMP),Eval(BenchClose(0)>SMA(120,0,#Bench),1,0),1)

Sell rule would be similar but the opposite:

Eval(Close(0,#UNEMP)>1.1*SMA(12,0,#UNEMP),Eval(BenchClose(0)>SMA(120,0,#Bench),0,1),0)

These rules are causing large performance differences in strategies run on the Legacy engine with the Compustat data and the new engine with the Facset database. The results are even quite different if I use the Current Engine with the Compustat database. If I turn these rules off to test the fundamental part of the strategies, the results are close, not the same, but at least way way closer than with these simple rules turned on.

Good catch. It looks like the buy rule gets activated on 4/6/09 on Legacy and 12/7/09 on Current, which explains the difference. We’re investigating and will report back soon.

OK, on to the next issue I’ve noticed in my strategies.

A strategy that ranks stock by a custom shareholder yield formula produces substantially different (over 3% in terms of annual return) results on the Current Engine between Compustat and Factset. The custom formulas is:

The custom formula is used in a custom ranking which is then used in the strategy. The strategy it is used in is “QEDGE: Large Stocks SHY Top 25 - 04”.

I tried to see if there was any big discrepancies in the individual stocks but didn’t really notice anything.

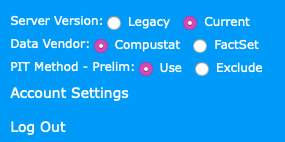

Can someone restate what the settings mean for the below. I have gotten confused on what the different combinations mean and how to use them for running current rules as well as a backtest. thanks. David V

Since last weekend (which got the engine to use FactSet estimates), many of my sims that rely on sentiments are performing much worse with FactSet. For example, take “core: sentiment” and “basic: sentiment” ranks from portfolio123. The ranking graphs are different between Current Compustat and Current FactSet. (Current Compustat and Legacy Compustat look the same).

I didn’t have a chance to go through the factors / formula used in these ranking, is this something that can be investigated by p123 team?

Paul, I’m afraid there’s not enough information here for me to investigate. Is that the only formula that chooses what stocks the simulation holds and what it buys and sells? Or are there other ranking systems, rules, etc. which might account for the difference? A number of the fundamentals are quite different between Compustat and FactSet.

FactSet fundamentals are things like NetIncBXor and CapEx. FactSet coverage determines which stocks are in the All Fundamentals universe.

We will be changing data providers for short interest information but I don’t know if that will be before or after July 1st at this point, and I’m not sure whether or not users will be required to pay extra for that information. We’re working on getting answers to those questions.

You should expect substantial differences. All the data providers count different analysts and have different methods of parsing those analysts’ numbers.

One of my models are not running at all, it uses Toronto Stock Exchange Universe, and it cannot find any stock during a 5 years simulation that meets this rule: EPSExclXor(0,qtr)>0 and EPSExclXor(1,qtr)>0 and EPSExclXor(2,qtr)>0 and EPSExclXor(3,qtr)>0 (last 4 quarters of earnings above breakeven). On Compustat it works fine (an on FactSet before this weekend change, it was working fine too).

Is there anyway to check in a log file whether Current-Compustat/Use or Current-FactSet/Use was chosen for a simulation? I’m see some rather large differences between the two data sources. That’s something new and I think it started recently - maybe today. But since I switch between the two often, it’s hard to confirm which results belong to each setting. Not having fun today.

Denis,

Many of the FactSet fundamentals were messed up around 5PM CT (7:50 hours ago). This was an unintended side-effect of work being done which will allow us to further address differences in FactSet fundamentals and make them behave more similarly. They should be back to normal by 4AM CT (in 3:10 hours). Thank you for your patience as we scramble to correctly implement all of the necessary features by the end of June.

Yep. I turned on and off all the other rules to isolate the performance difference to just that custom formula. I just ran it again and the Factset numbers got worse. Hopefully, this is because the 'FactSet fundamental are messes up…" right now…