But SUPirate1081 uses IB VWAP orders and told me I worry too much about slippage (a while ago in a post). He thought he could get as low a 6 basis points of slippage on whatever universe he uses.

Again, without really knowing about anyone else’s slippage, SUPirate1081 was right. Slippage does not have to be a big problem by my accounting. I do use a more liquid universe, however, so as Kurtis says: slippage is different for everyone. I am not implying that VWAP is important: I use VWAP less than half the time.

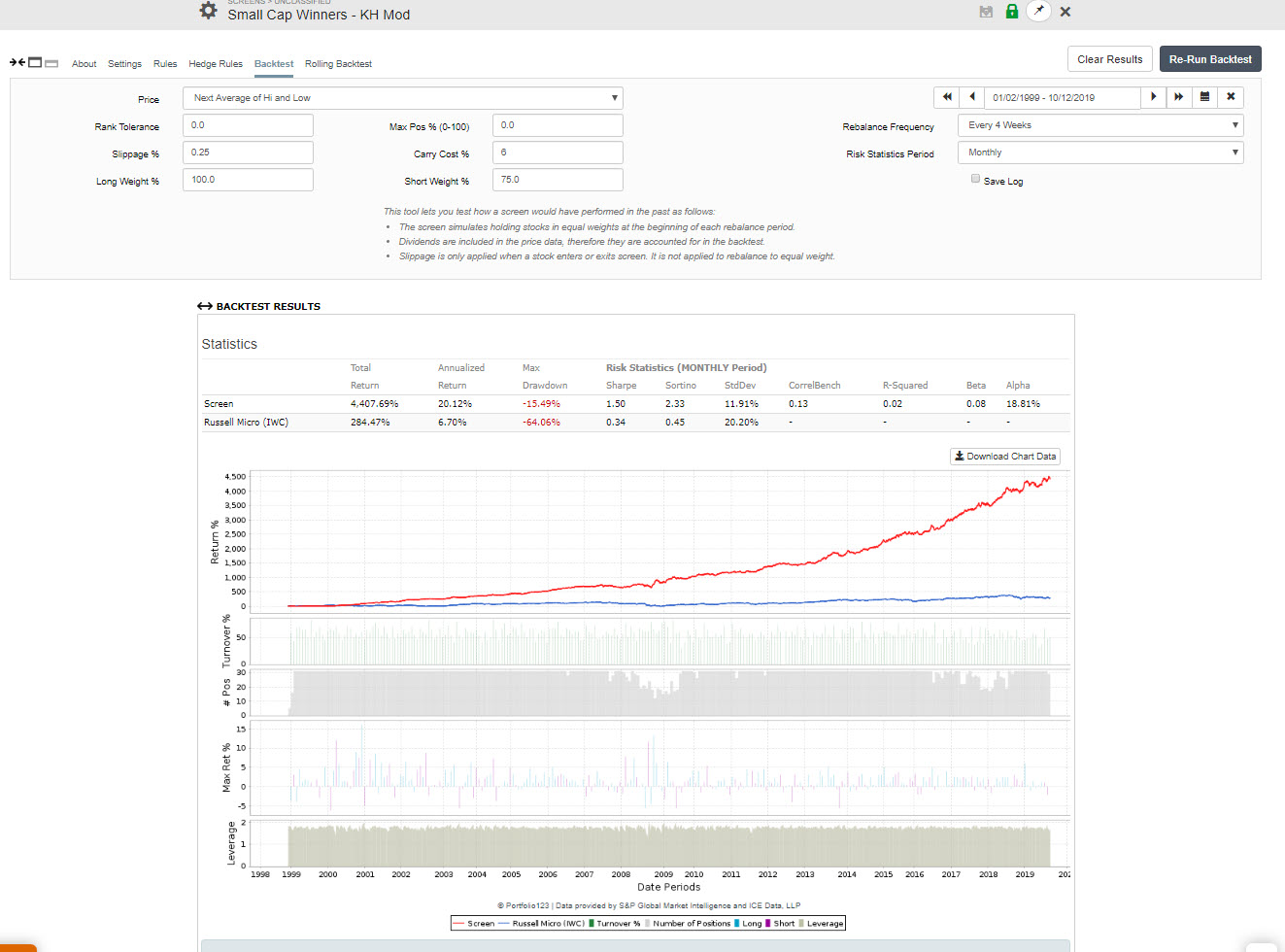

This particular screen (small-cap winners) is loosely based on the ranking systems that I’ve been using in my own trading for years. The biggest factors in my own ranking systems are share turnover, price-to-sales, forward earnings yield, sales acceleration, accruals, sentiment factors, and operating income growth, which, except for accruals, make up the prime selection factors of this screen. To come up with the ranking systems I use I did test all sorts of factors to see what worked in the past. But this screen itself was not backtested much, nor was it optimized. Also, I now rarely pay much attention to the 1999-2007 period when backtesting. Though perhaps I’ll regret that . . .

Another way to improve that screen might be to impose it to pick only from defensive sectors in the summer.

Just a thought to contribute - I have not tested it here but it worked well for me in other systems.

(based on the seasonality observation articulated many times by Georg in this forum)

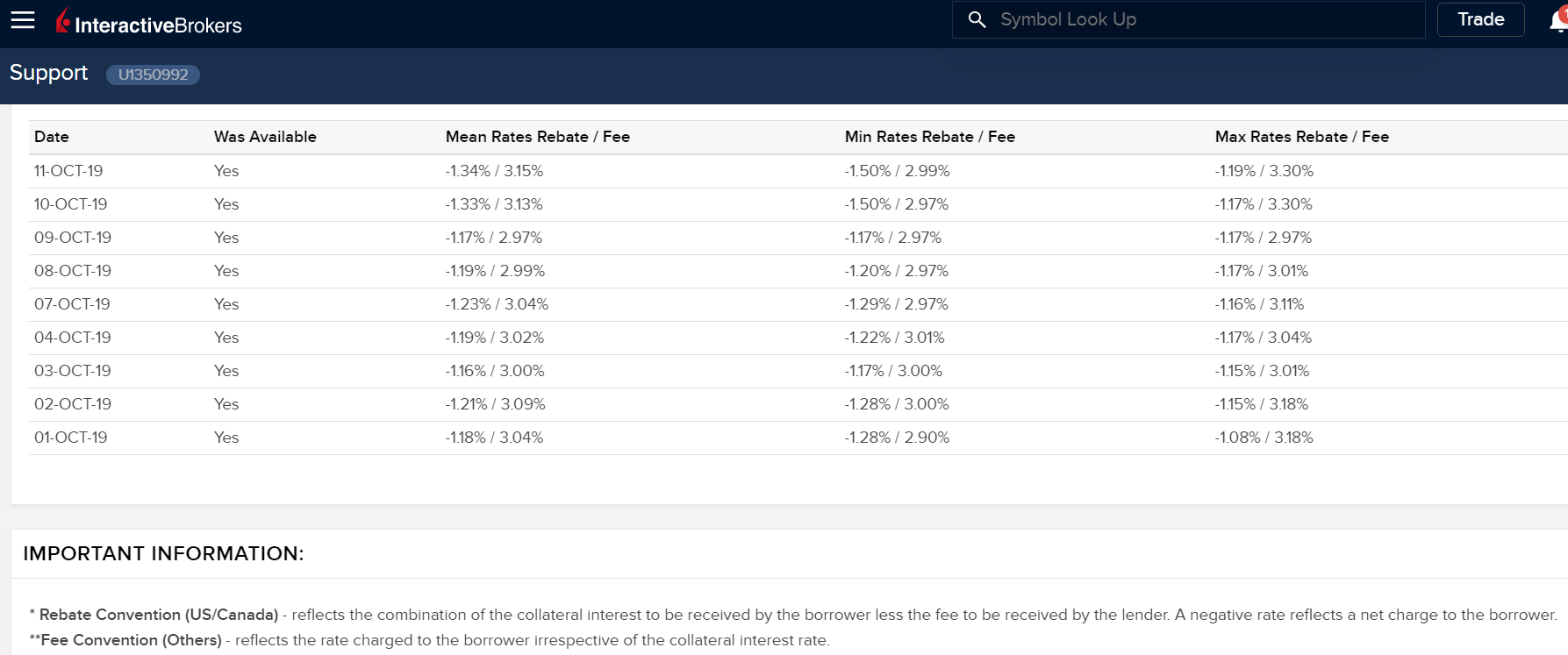

Wouldn’t the correct number be the rebate amount? That’s the fee to the guy who owns the stock minus some interest paid on the cash in your account. So 1.34% cost to borrow assuming you are using cash. Add in margin fees if you are borrowing the cash from your broker.

Kurtis you are correct. But since you have to borrow the collateral cash for the short position from your broker you have to add margin fees.

When you short a security it must first be borrowed. In order for the lender of the security to ensure that she is paid back she will insist on receiving collateral to secure the loan.

The security lender will then pay the borrower some portion of the interest that she earns from the collateral. This interest payment is known as the short rebate. For IWC this is currently -1.34%, meaning the borrower will be charged this interest rate - not receive it. The rebate rate is negative because it is calculated as the Fee Rate (3.15%) minus partial interest earned on the collateral (1.81%) = -1.34%.

From IBKR website:

The Fee Rate represents the rate (generally expressed as an interest rate) that the lender assesses to the borrower of the shares. The lender will then reinvest the cash collateral posted by the borrower to secure return of the shares and may offer a partial rebate of those earnings back to borrower’s broker (generally equal to the Fed Funds Rate in the case of USD stock loans). Many brokers do not pass any part of this rebate to retail accounts although IBKR does and the Rebate Rate reflects the net of the Fee Rate and any rebate offered.

For example, assume stock ABC is hard-to-borrow and carries a Fee Rate of 20%. If the Fed Funds Rate and rebate provided is 2% then the Rebate rate is -18% (note that a negative Rebate Rate reflects a net charge to the borrower).

If your collateral is not cash then you have to borrow the money from your broker. You need a margin account for this. For IBKR LITE it will cost you 4.32% on a debit balance of $100,000. So if you have not sufficient cash in your account and use the long positions as collateral for your loan then you need to borrow the cash for the short trades from your broker.

To this must be added payment to the lender of any dividends received from the borrowed security. In screens prices are with dividends and not accounted for separately as in strategy simulations. The current yield of IWC is 1.16%.

The total current carry cost for IWC would therefore be:

For screens: 1.34% + 4.32% + 1.16% = 6.82%

For sims: 1.34% + 4.32% = 5.66%

So if one uses this carry cost in your screen the annualized return is about half of what is shown with zero carry costs.

Note: It would be better to use IWM as a hedge. The current Rebate Rate for IWM at IBKR is +1.41%, so the carry cost becomes less: -1.41% + 4.32% +1.16% = 4.07% for screens, or 2.91% for sims.

I’ve increased the carry cost to 6% and kept it with IWC. The other change is that I am keeping the top 30 according to the Zweig ranking system with a minimum rank cut-off of 70.

Of course, converting this to a sim allows you to be much more dynamic and timely with the selling while lowering turnover. i.e. you can rebalance weekly but have lower annual turnover with higher returns. But again, this is just idea generation - not a model that I am recommending anyone copy line for line.

There is a scientific way to determine the HEDGE amount based on information theory.

Fortunes Formula popularized this theory and describes what a hedge does using a horse-racing analogy:

You would have done better to hedge your bets by wagering ……on all the other horses. You would be sure to win something, and possibly a lot. The bets on the horses you think will lose are a valuable “insurance policy.” When rare disaster strikes, you’ll be glad you had the insurance.

He goes on to describe how much to place on each horse:

He places bets according to his best informed estimates of the probabilities. When you believe that War Admiral has a 24 percent chance of winning, you should put 24 percent of your capital on War Admiral.

How to determine the probably of the port and of the hedge winning over a certain period?

Easy, rolling backtest. There may be other ways that are a little more complex. But that would be a start.

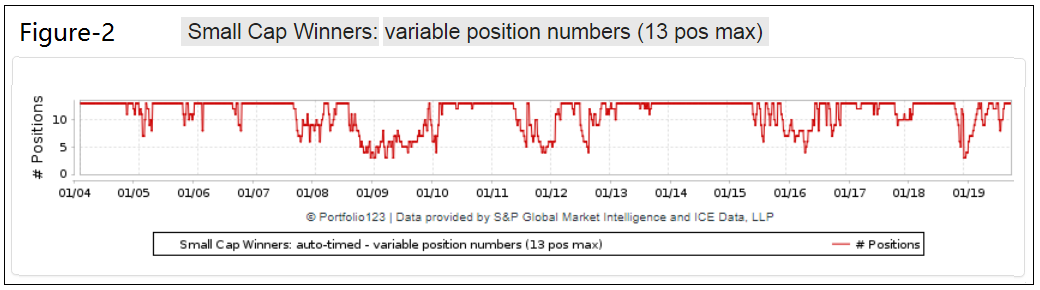

One can use this screen as a stock market timer.

Look at the screenshots which Kurtis posted. When the number of positions get less, like from 2007-2009, it is prudent to reduce exposure to equities.

Here is my own model based on modified rules of Yuval’s Small Cap Winners screen. It only selects a maximum of 13 stocks. When the model holds more than 10 positions it should be relatively safe to be in equities.

I’ve been doing some research into this and with an all-or-nothing payoff (i.e. one horse wins and all other bets lose), with frequent betting, and with high stakes, it’s indeed wisest to place your bets exactly according to the percent chance of winning. The mathematics behind this is pretty neat.

But with graduated payoffs (i.e. you don’t lose your entire stake on horses that don’t win), the best strategy can be very different. I’m in the middle of writing an article about optimal betting strategies, and will reveal more soon.

Very much agreed. Shannon’s Entropy is EXTREMELY INTERESTING.

BTW, some of your concerns are why I picked a hedge. Ideally, the stocks would be like the horses—only one wins. I.E., ideally there would be a perfect inverse correlation between the port and the hedge. I am open to the idea that this does not solve all of the problems using this theory—even if there were ever a perfect hedge.

Horse races do have different payouts: different odds. The theory says the odds should be completely ignored and you should “bet your belief.”

Is different payouts (odds) like different returns for stocks. I will think about that and I will keep an open mind. My guess is that the payouts should be a zero sum game for this to work without modification—like bookmaker payouts. Does an ETF and the short of an ETF approximate that? Maybe but a port is not an ETF.

There are other legitimate concerns with my post. E.g., it is not a zero sum game like horse racing (I went ahead and discussed some of this above but I am not sure that covered everything). Theoretically, all stocks can win as the economy expands. I look forward to ideas that refine and improve my thinking on this.

Without a doubt the bookmaker take or slippage, commission, borrowing costs, margin etc add complications.

I look forward to the article. Can you put link in this thread when it is available?