It should make no difference in a ranking system. The relative position in the ranking system will not change. Easy math to follow.

BTW, nextFYepsmean/abs(nextFYeps1wkago) - 1 = (NextFYepsMean- NextFYeps1WkAgo)/abs(NextFYeps1WkAgo). So you are just adding or subtracting a constant (I.e., 1) which is why the rank position does not change.

So it is just a preference of whether you like to say my earnings are 120% compared to last year (100% would be the same as last year–no change) or my earnings are up 20% compared to last year. To get percent you would multiply your equations by 100.

Note that the whole thing falls apart if NextFYEPS1WkAgo = 0. In practice this does not seem to cause much problem but could be addressed using Eval.

Summary: use either one. Your equations will do the same thing. You would have to be careful in long equations with other variables such as earnings for trailing 12 months.

Good equation but can end up dividing by zero or close enough to zero to be a problem at times. I’ve tried using eval(nextFYEPS1wkAgo=0, NA, (NextFYepsMean- NextFYeps1WkAgo)/abs(NextFYeps1WkAgo)) without much improvement in results. Does just as well making NA neutral in the ranking system (as you would expect). Probably the computer converts an equation with zero in the denominator to NA anyway.

Your graph shows we may need to use something like Eval(NextFYEPS1wkago < 1 and NextFYEPS1wkAgo>-1, NA, (NextFYepsMean- NextFYeps1WkAgo)/abs(NextFYeps1WkAgo)) and make NA neutral in ranking system.

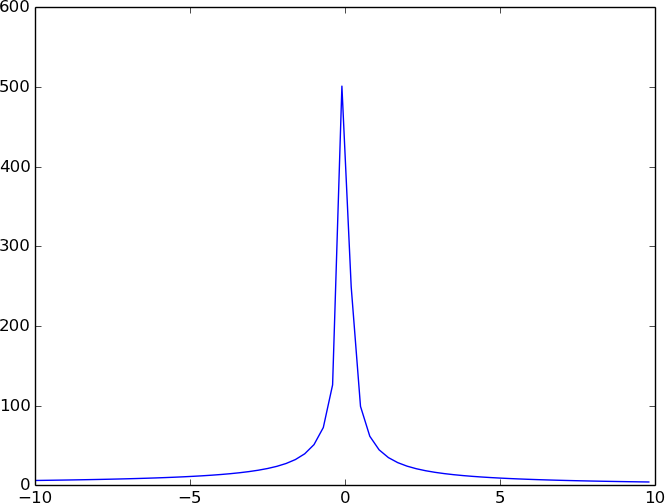

However, there has to be something better than my last equation. Does anyone in finance know what meaning an improvement of earnings from $0.01 to $1.00 per share has (this would be a 10,000% improvement as Aurel shows). How it should be ranked? Should it be treated more like going from $1.01 to $2.00 per share?

Did you edit the equation? My ports seem to always do worse when I exclude stocks with negative earnings in the ranking system.

I like abs(NextFYEPS1wkAgo)/(NextFYEPSMean - NextFYEPS1wkAgo). Lower is better. I think the Abs helps when both the NextFYEPSMean and NextFYEPS1wkAgo are negative but the NextFYEPSMean > NextFYEPS1wkAgo, as you pointed out earlier.

Yes, actually the formula is just a switched version since its only merit is to tolerate any value of 1 weekago but we still need to screen for Epsmean to be above 0, otherwise it’s the same problem all over again when EPSmeans moves between [-1;1]

For sure the above formula is better than nextFYepsmean/abs(nextFYeps1wkago) for the reasons Aurel stated. It’s the one I still use knowing it is not perfect when the denominator is close to zero.

what is the most appropriate language / rule

for selecting stocks with

eps revisions falling from one week to next?

if using in a RANK

(NextFYepsMean- NextFYeps1WkAgo)/abs(NextFYeps1WkAgo)

for positive revisions,

does “Flipping” the rule (selecting lower value button ) as opposed to Higher Values…

select stocks with negative revisions ?

or must a completely different rule be used when ranking

a revision going lower ???