Works good for me now, as it is, using allow cash and margin.

It calculates the 20% goal/maximum number of shares for the port which I can reduce on my own when there is not enough cash available.

Thank you again!

-Jim

Works good for me now, as it is, using allow cash and margin.

It calculates the 20% goal/maximum number of shares for the port which I can reduce on my own when there is not enough cash available.

Thank you again!

-Jim

It doesn’t seem to be working. Even if you put it at 100% it allows a lot of very minor rebalancing transactions to take place. It definitely worked last week. Is there a difference from last week in how it should be set?

You are correct. The line of code implementing it was removed when it was removed from the front end. It should be functioning again as expected, but input on whether a relative percent would be more sensible for this option would still be appreciated.

Aaron,

A percent relative to portfolio value seems a little problematic for what you are doing.

I think Marc’s general goal and one I might use at some point is for a 20 stock portfolio the first stock may have a weight of 10% gradually declining to a desired percent of 2% for the lowest ranked (or lowest weighted) stock before it is sold.

2% of portfolio value has a very different meaning for the highest and lowest weighted stock. I.E., a deviation of 20% of ideal weight for the highest ranked stock but 100% for the lowest ranked stock.

20% of ideal weight keeps things constant. I am not sure that this is the best way but better than % of portfolio value, I think.

I think I am probably not understanding that second quote correctly: taking it too literally or out of context?

Just trying to be responsive to your request for feedback.

-Jim

Aaron,

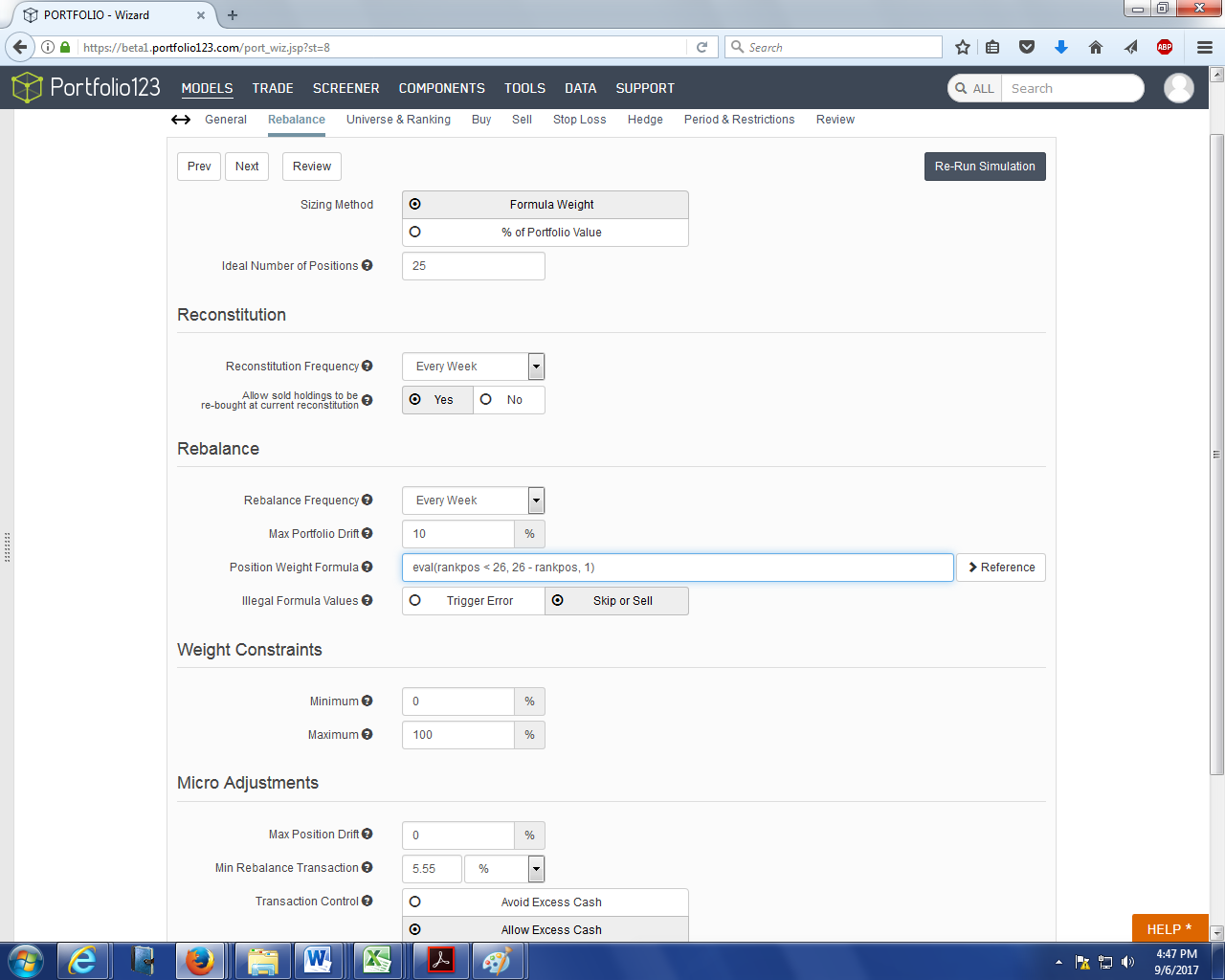

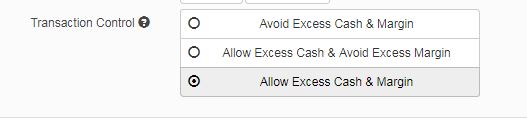

I get “Encountered unrecoverable error while rebalancing. Please contact support.” when rebalancing with “Avoid Excess Cash & Margin”.

Works o.k. with the other two options.

iM-Short SDS or PST

https://beta1.portfolio123.com/port_summary.jsp?portid=1499914

Aaron,

I have been playing around with a 20 stock sim that I want to be low volatility (which goes to cash a lot and I want to stay in stocks as much as possible).

I get better results when using the new formula based system when I use the following setting. Can you explain what the difference is between the last setting and just using the % Portfolio value rebalance method (they feel like they should almost be the same. They both end up with cash outstanding but just different amounts)? If it is already posted somewhere, can you point me to it?

I really like the tradeoff in results that it gives me (AR vs cash invested vs Sharpe vs STDDEV vs Correlation vs beta).

thanks.

David - Look at your transaction records for your sim. You might see that with this setting your highest and lowest ranked stocks are bought at very close to the same percentage each period, and that without this checked off your percentages vary widely depending on how many positions–and how big they were–you sold at the same time. At least, that’s what I see, but my settings might not be the same as yours.

Also, look at the average leverage by downloading the results off the main page and averaging the leverage. You’ll often see an average leverage over 1.0 using this button, which in some part explains the higher results. - Yuval

Aaron -

I would very much like a relative percent for this option, because it more closely mimics how I actually trade. When my system says that the amount I have invested in a stock is too low, I buy more only if the additional amount is more than 25% of what I have. When my system says that the amount I have invested in a stock is too high, I sell some only if the amount I sell would be equal to or greater than the amount that I should own. So my buy min transaction is 25% and my sell min transaction is 100%. That may not be possible to mimic in this simulation, but a relative percent that I can adjust would be nice.

The way it is now configured the minimum rebalance is exactly the same as the max position drift, as far as I can tell. I’d prefer to have it the way it was last week.

Thanks,

Aaron -

I see you’ve changed the “transaction control” to disallow leverage. This is not a good thing. Here’s why.

Look at the screen shot below. This is my system–it’s not terribly complicated. My buy rule with this system is rankpos <= 13 and my sell rule is rankpos > 25 and stalestmt = 0 and nodays > 8.

I run this and look at my transaction record. Let’s just look at the stocks that are ranked 100.0 (rankpos = 1 or 2). Here are the new percentages bought: 5.21%, 6.92%, 7.95%, 7.26%, 5.33%, 7.64%, 7.14%, 9.12%, 9.23%, etc. In other words, there’s a huge variety here. And it all depends on how many stocks I buy that particular week–if it’s a lot of stocks, the percentage is low, and if it’s not many, it’s high.

If you allow leverage, the transactions are much much closer to the ideal, and are all really consistent. They no longer depend on how many stocks you buy or sell that week.

Thanks,

I was liking that too. I cannot get very close to my goal of 20% now.

I can’t really get margin in my SEP-IRA but I usually have some cash from the other ports and it is not hard math reduce the positions manually when necessary.

And I don’t want to just hand money to the market maker so I never go over 20%. “Use Margin or Leave in Cash” was way cool!

Of course, none of this is hard math and I am good with what the community as a whole wants. In fact, no problems with the way I’m doing it now.

-Jim

Aaron -

Another idea to avoid the huge discrepancies between buying positions from week to week would be to add an option of max weight deviation from ideal, like we have with the % of portfolio value option. Then leverage would no longer be necessary.

The leverage option is no longer available for cash portfolios, but it still is for margin portfolios.

It is quite counterintuitive, and not very realistic, to have the possibility to go on leverage without margin.

To use transaction control the way it was on cash portfolios, you can set up a margin portfolio with target leverage 1 and select the Rebalance option “allow for deviations from target leverage”.

That works for me, and it makes a lot of sense. Thanks a million!

By the way, if anyone else wants to explore this option, it’s important to realize that you’re going to get much higher apparent returns if you do, and those should be adjusted for the amount of leverage you’re using. The easiest way to do this is to use an Excel spreadsheet.

Does “maximum weight constraint” mean that if you set it to 5% no positions will be larger than 5%? If so, it’s not working–I get positions a lot bigger than 5% even when it’s set at that. Or does it mean something else? Thanks, - YT

There was a > that should have been a < in the code that constrains weights. Thanks for letting us know about it.

Well, now the “maximum weight constraint” actually does something, but from looking at the transaction records, it’s different from what I expected it to do. Can you please clarify? It’s certainly not capping my buys at the percentage I’ve inputted, which is what I expected it to do. Instead, if I set it to 4%, all the buys that week will be more or less the same percentage–in other words, it overrides the position weight formula–but they won’t be less than 4%. And I can’t see any difference between setting it to 10% or 100%–those two settings seem to give me the same result.

Also now I see the min rebalance transaction works quite differently from how it worked last week if you set it to %. Maybe that’s a good thing since last week it exactly replicated the max position drift.

Thanks for all the interesting stuff going on here. It’s a lot of fun to play with.

Regarding the max weight constraint, I’ll need a sample simulation where you’re seeing unexpected behavior to understand what you’re saying.

Min Rebalance Transaction % now implements a relative percentage by ensuring the number of shares in rebalance transactions are at least X% of shares owned. We may allow a distinction between buy-side and sell-side transactions in the future (as you indicated in this post), but we can’t consider it for the initial production version.

OK. Look at this public simulation: https://beta1.portfolio123.com/port_summary.jsp?portid=1502097. The max weight constraint is 4%. Open the list of transactions. You’ll see that every week the transactions are all equal: the position weight formula is totally ignored and the weights are all between 5% and 7%. Then redo the simulation with a max weight constraint of 9% and now the position weight formula works fine, but the max weight is higher than 9% during the initial buys. - YT

Personally, I would make it such that when someone checks “allow excess cash” that “max weight” would become a hard limit. This would set the weight of the highest weighted position and everything else would be scaled down from there.

Or, alternatively, that all weights above the “max weight constraint” are set at the maximum weight with some of the lower weighted positions (possibly) having less than the max weight. I am not sure what the community would prefer on this. Probably the option of setting it either way.

And who does not want the answer to this question: What if I buy the highest ranked stocks in amounts up to the maximum liquidity buying lower ranked stocks only due to liquidity constraints–as I have more money available in the future? Would I start with 5 socks now and end up with a bazillion dollars holding 25-50 stocks in 5-7 years?

This is the actual plan for many of us—with some added diversity/risk management measures. The present compounding of the 5-10 stocks is not actually realistic unless you do not get much slippage buying $100,000,000 worth of a micro-cap or a small-cap stock. The realistic plan could be tested with a hard limit and a sell rule: 1 (or even RankPos > x). This would be a new feature that all but the closet indexers of the SP 500 would use.

Then “avoid excess cash” would continue to allow the hard limit to be exceeded with scaling and relative weighing for the new positions to keep maximally invested.

I understand that will not happen in this release. Then the only question remaining is whether anyone will understand this release or use it if it happens that some do understand it. Using it and not understanding it–until there is a problem–being the worst case scenario.

I guess we will see. And good luck on that.

-Jim

The maximum wieght percentage should simply cap the weight of an individual security. That is the most intuitive way and I’m not a believer in making the algorithms that are too sophisticated. Capping the weight is what ETFs do and it would be nice to be able to emulate their performance.

Steve