So, open question… should we add the Yuval’s ranking system to the P123 Ranking system list or not?

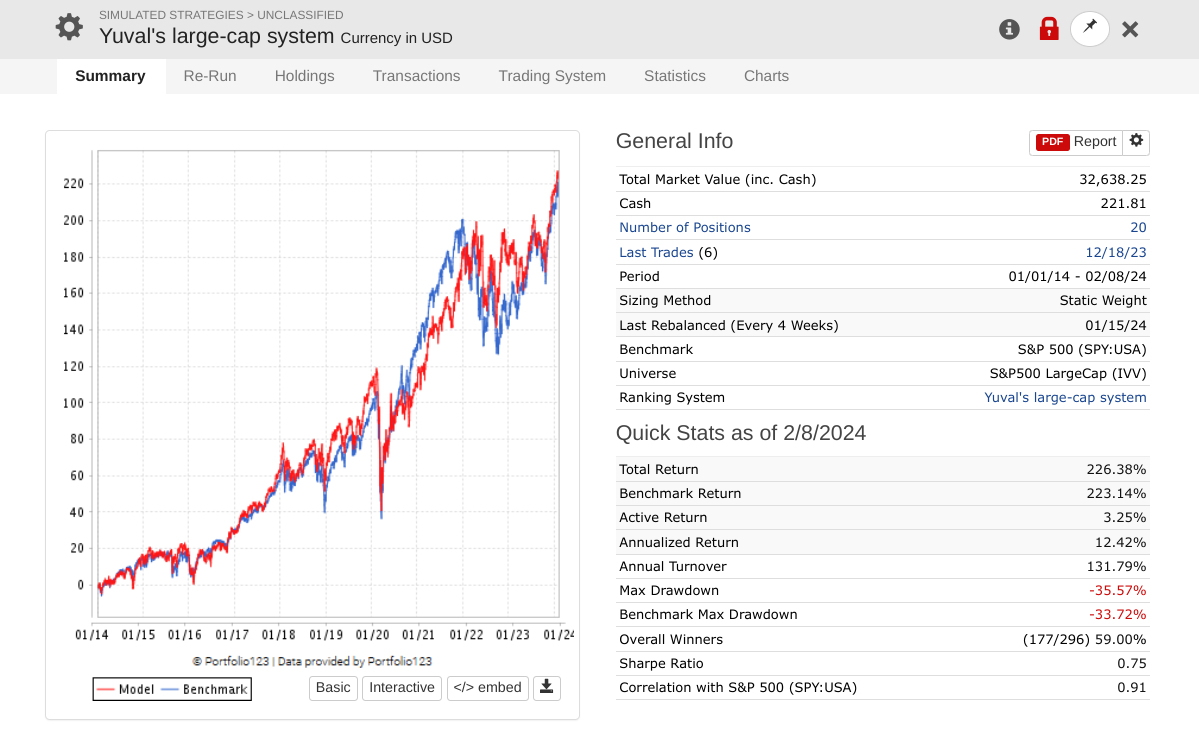

So, I wanted to resurrect this simulation and see how it had done over the past 4-5 years (essentially OOS). My observation is that it replicated the S&P with no improvement in alpha.

- Thanks to Yuval for providing something public that we could look at many years later.

- Does anyone else have a different story for success in Large Caps?

- Does anyone think alpha factors can still be exploited in Large Caps?

I think it’s very difficult to get alpha in large caps out of sample. I have not been able to do so. I hope to be proven wrong.

In my opinion, large caps are best for very long-term holding. They provide a good cushion. If you thought you might die tomorrow and wanted your inheritors to profit from the stock market without your knowhow, designing a large-cap model that specializes in very stable and reliable companies with an annual rebalance might be a good idea. Alpha might be elusive but risk might be minimal.

1 Like

personally success with large caps, my methodology is I only invest the tech sector, weekly rebalance, never more than one to five stocks in the portfolio, I do not require any edge to make $$$, the SP500 index is momentum, no momentum you are out of that index, every year or so, new inclusions ( all sectors ) to the index prove themselves over the next year or so, some of the vola in the tech sector is fantastic and you got the liquidity, muy importante, from my previous market experience with smallcaps, even when you have the dinero to invest can pose all type of problems, to the point you become the market, generally for the average investor its liquidity, the better the liquidity the lower the investment return, the more diversification the less return, the ranking from P123 that are very useful are growth and sentiment, anyhow you gain avg annual 15% more or less over 15 years, reinvested you make your madre and pappy cry with happiness for the sueno americano, for example see this link for the vanguard total mkt fund, from 1994, also exceptional performance from 2008, annual growth at 10%, Backtest Portfolio Asset Allocation, and this is a big diversified fund, anyways success is long term strategy ( sales = earnings as simple as and try not to be a seer) and keeping to the strategy thru thick and thin. addendum Backtest Portfolio Asset Allocation 4 tech stocks from 2012 not even well ranked until recently $10K to $100K ( inflation $86K ), thru thick and thin, most is about head space,

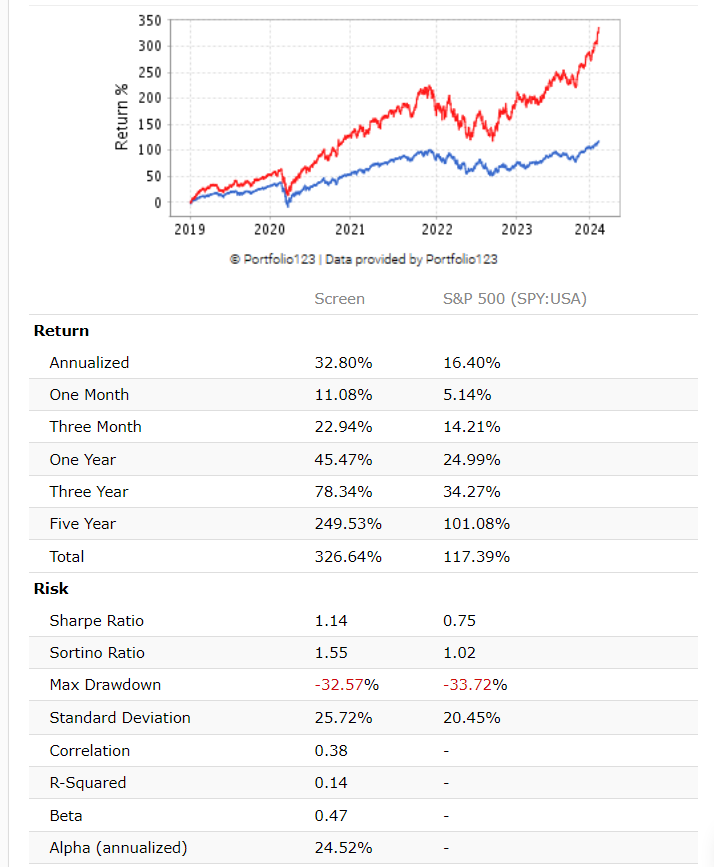

Screen that selects the 12 best stocks from the SP500

https://www.portfolio123.com/app/screen/summary/292174?mt=1

1 Like

Yuval, could you develop a ranking system for selecting REITs that will be standard in P123 ?

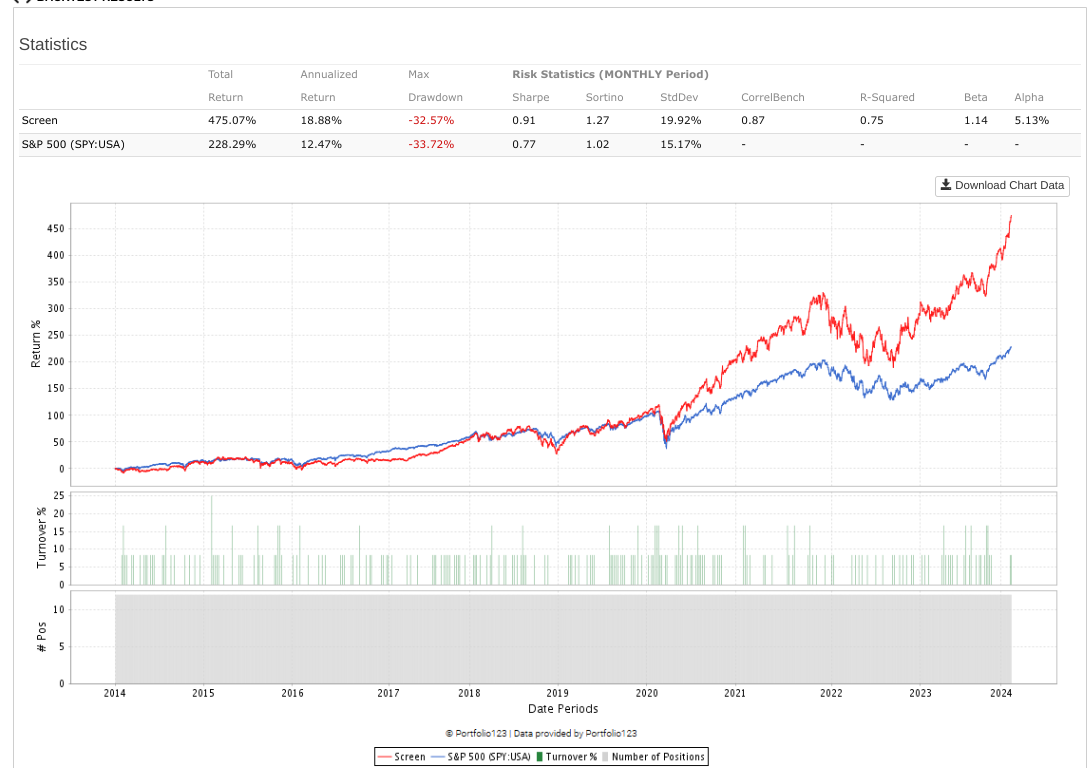

m7da, Do you have any suggestions as to why there is underperformance until 2019 and then overperformance?

I haven’t had much out-of-sample success with selecting REITs, I’m afraid.

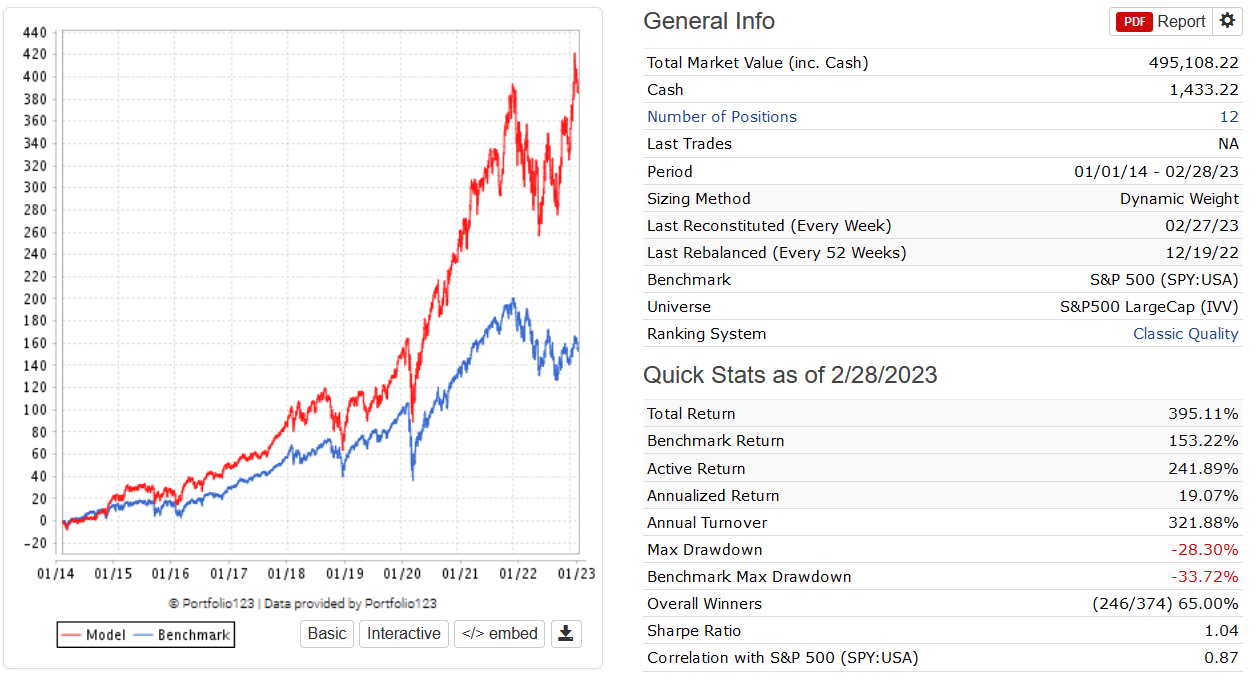

In fact, I’m using a screen with a lot of filters, which is similar to this simulation that I developed earlier when I had trial access to simulations.

regarding the chart above, based upon the inputs that I can see that is about correct,

how does the chart look if you simulate back to 1999 !, also I comment in an earlier reply to this post that, most investment is about head space and where your at etc, many good strategies were blown apart by the creator/s, for example I can see eight distinct time periods where a drawdowns occur over a time period of six months to one year ( circa 2022 ) in a downward channel, how do you feel when you encounter those downturns, change strategy, stick with it, bail out completely, it those downturns that most investors cannot handle and therefore fail, mindset is all, SP500 is alpha.

<ignore - deleted>