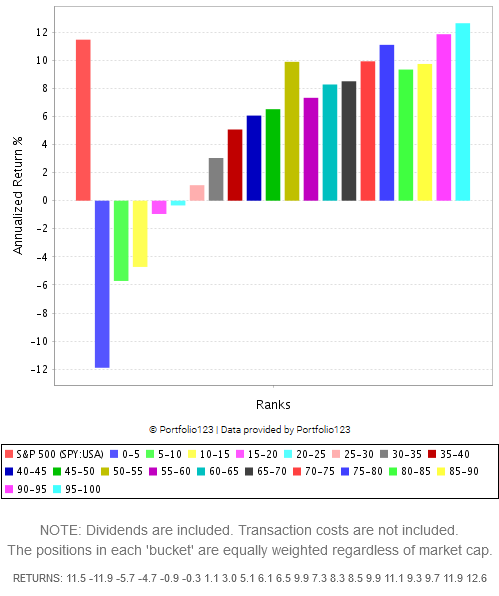

In designing a ranking system for going short you want to reverse most factors but keep the size factors the same. (Or reverse the entire system and then reverse the size factors again.) Size factors (the smaller the better) are augmentative, making both ends of the ranking system steeper. Or simply exclude the size factors. Here’s how Core Combination has performed on the Easy-to-Trade US universe over the last ten years, rebalancing monthly:

That has truly significant negative performance in its lowest 5% bracket. And consider that this ranking system has been around for more than ten years in one form or another, so it’s almost out-of-sample.

I’ve made a ton of money buying cheap out-of-the-money puts dated about six months out; the returns have been fantastic, and it’s wonderful to be able to hedge my portfolio with them. The factors that seem to work the best for these are decelerating sales, a high ratio of net operating assets to total assets, low market cap, unstable ratio of gross plant to sales, low free cash flow margin, high price volatility, low current ratio, dividend payments that exceed net income, negative subsector momentum, negative price momentum, and a large increase in investment (gross plant and inventory) compared to total assets. I don’t use value factors nearly as much in my ranking systems for puts as I do in my long strategies.