Thank you, and sorry for the mix up! what about the SD/beta/volatility? TOne reason to look at LS is to mitigate vol, right?

RTNL,

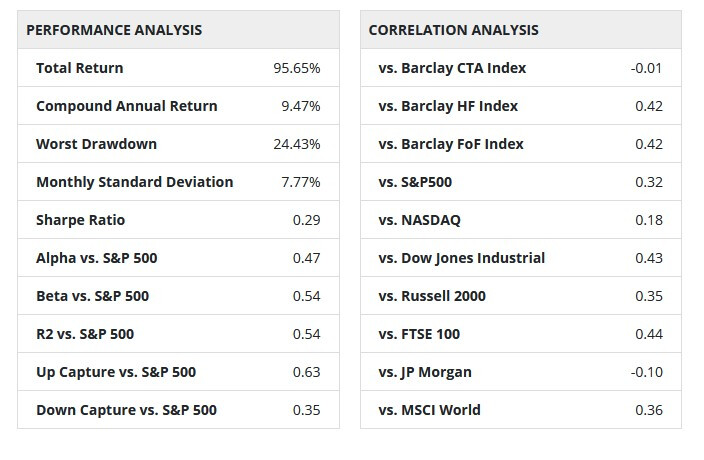

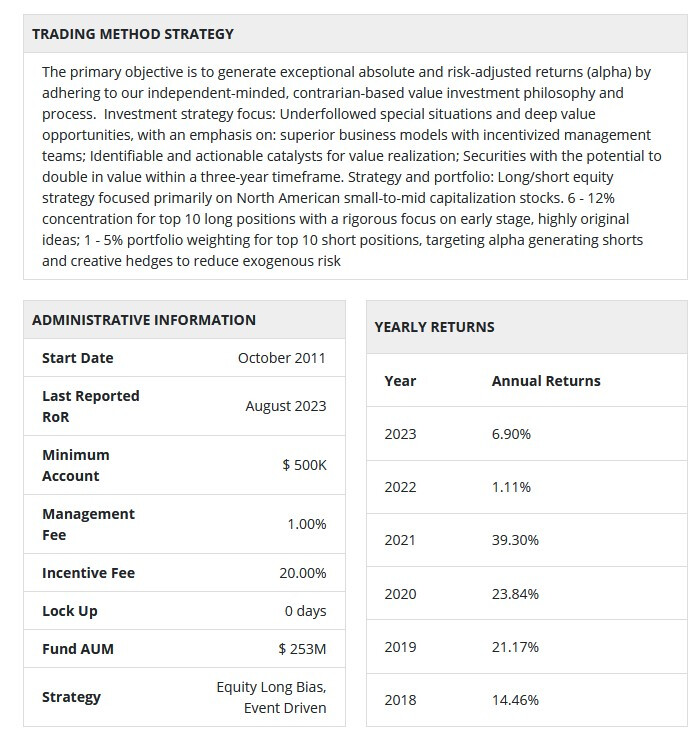

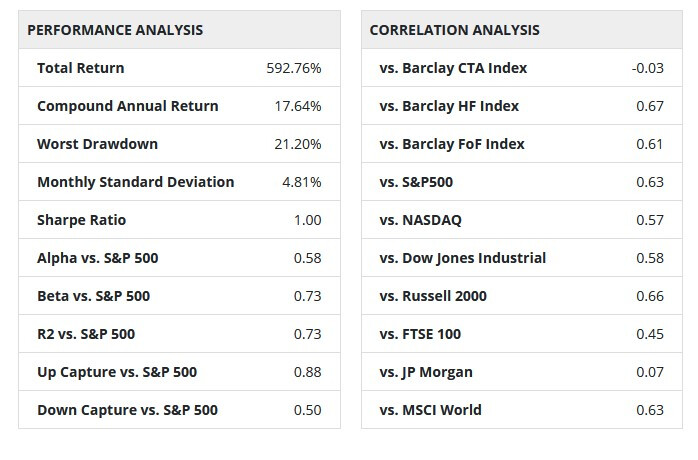

Here are the snapshot for the other 2 funds.

Regards

James

Brook Absolute Return Focus (London)

Voss Value LP (Houston)

2 Likes

thanks James

Hi Yuval,

Your hedging strategy sounds very interesting. Most studies on hedging indicate that it is generally more consistently profitable to be a seller of premium, rather than a buyer, and yet you’ve managed to have success with the latter approach. Did you ever attempt to sell OTM calls, and if so did you find that strategy was too risky or had some other flaws? Also, can you elaborate on how you evaluate the pricing of out-of-the-money puts to decide when they are too expensive? Thanks.

Because I was doing this in retirement accounts I did not explore the possibility of selling calls. I’d be interested to hear what advantages there might be to doing so. I’m writing an article about how I approach puts and will discuss, briefly, how I determine the price I’m willing to pay for them. The article will appear on the P123 blog in a few weeks.

Ah, makes sense. With respect to selling premia vs. buying, here’s my layman’s summary: so long as implied volatility is greater than realized volatility, then time decay looms large, ie it’s a tailwind for the seller and a headwind for the buyer.

On a related note, you might enjoy the attached research re: one such application of selling premia, ie selling short-term index “strangles” (ie OTM calls and puts with a similar delta and the same expiration). Also, AQR has published several pieces of research on various hedging strategies via options, they found that systematically buying puts is often a money loser, despite its obvious appeal (I suspect for the reason I stated initially). I’m attaching one such research article - you might search the AQR website for a deeper dive

AQR Chasing Your Own Tail Risk.pdf (465.5 KB)

.

Anyway, kudos on your success. I look forward to that article.

Index Options _ Benefits of Selling Volatility (3).pdf (766.0 KB)

Good point! I very rarely buy puts whose implied volatility is greater than realized volatility. I do understand that that is the case for most put options, but I’m looking for the exceptions.

Another idea to gain from equity market volatility was described in Positional Option Trading: An Advanced Guide by Euan Sinclair. He claimed that a trader can make profit by buying straddle on stocks with specific fundamental characteristics.

He suggested to buy straddle on stocks with:

- Low P/E

- Low P/CF

- High market cap

- High RoE

- High RoA

- High D/E

His backtest was performed on S&P 100 index. Unfortunately without option prices we can not validate these results.

1 Like