Currency ETFs don’t go back that far. 10 years is pushing it.

Currency ETF inception dates are:

FXA, FXC, FXS 6/26/2006

FXE 12/12/2005

FXY 2/13/2007

UUP 2/28/2007

So earliest start date for the model is one year after inception of the youngest ETF.

That gives you 3/1/2008.

10 year backtest is not “pushing it”, because 8/4/2008 is after 3/1/2008.

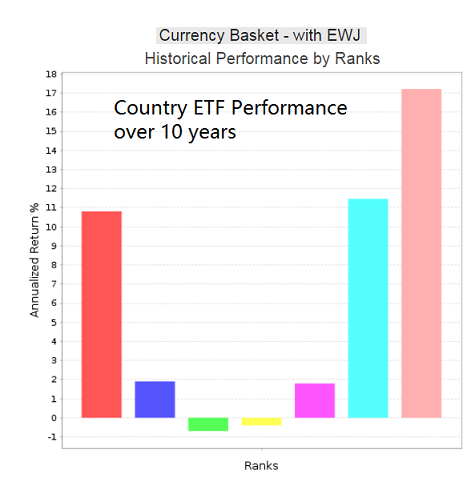

Here is what I get over a 10 year backtest period using EWJ instead of DXJ. About 17% annualized return, similar to the simulation’s 10-year annualized return of 18.2%. The return includes the performance during the great recession.

The ranking system based on the performance of the respective currency ETFs seems to work well.

Nope. Currency hedged ETFs are designed to perform better when the base currency is weak.

The model is based on rotating into countries when the base currency is weak.

It’s logically consistent.

Foolish consistency (sticking with all unhedged ETFs because there aren’t enough hedged) is a damned hobgoblin.

DXJ and EWJ have not much in common, because they follow two different Indexes. DXJ holds companies that derive less than 80% of their revenue from sources in Japan, while EWJ covers approximately 85% of the free float-adjusted market capitalization in Japan.

DXJ tracks the WisdomTree Japan Hedged Equity Index.

The WisdomTree Japan Hedged Equity Index is designed to provide exposure to Japanese equity markets while at the same time neutralizing exposure to fluctuations of the Japanese Yen movements relative to the U.S. dollar. In this sense, the Index “hedges” against fluctuations in the relative value of the yen against the U.S. dollar. The Index is designed to have higher returns than an equivalent non-currency hedged investment when the yen is weakening relative to the U.S. dollar. Conversely, the Index is designed to have lower returns than an equivalent unhedged investment when the yen is rising relative to the U.S. dollar. The Index consists of dividend-paying companies incorporated in Japan and traded on the Tokyo Stock Exchange that derive less than 80% of their revenue from sources in Japan. By excluding companies that derive 80% or more of their revenue from Japan, the Index is tilted towards companies with a more significant global revenue base.

EWJ tracks the MSCI Japan Index.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. With 322 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

So DXJ is not actually hedged against fluctuations in the US dollar - Yen exchange rate, it merely invests in companies listed in Japan which derive less than 80% of their revenue from sources in Japan. So there is no reason why my model should not use DXJ in preference to EWJ.

Miro - your argument is incorrect. Just because a currency WAS weak, does not mean that it WILL BE weak going forward. My ranking system test using currency ETFs effectively demonstrated that.

Goev - you are getting further away from any kind of logical narrative. i.e. you are using weak Japanese currency to enter a position that is more global than japanese-based, and carried further by hedging using a currency that doesn’t closely match the equity holdings. All I can say is Huh???

Steve - did you use currencies from the manipulators like China, etc? Or did you use Geov’s set of 6 free floating developed currencies?

Miro,

That is a very good return from investing in currency ETFs only. The implications for trading currency futures based on this model should be of great interest.

Steve, I fail to see the logic of your criticism. You must have misread the description of the WisdomTree Japan Hedged Equity Index.

The Index only excludes Japanese companies that derive 80% or more of their revenue from Japan. So for example, a company which has 79% of income from Japan and 21% from outside Japan is included in the Index. Below is the list of the Top 10. They look very Japanese to me. These companies are not more global than Japanese-based, as you assert. Also you seem to think that there is some currency hedging going in DXJ. That is not the case, they simply hold companies from the WisdomTree Japan Hedged Equity Index.

Top 10 WisdomTree Japan Hedged Equity Index Holdings, as of 3/31/2018.

Company Name Weight in Index (%)

Toyota Motor Corp. 5.5%

Mitsubishi UFJ Financial Group, Inc. 3.5%

Sumitomo Mitsui Financial Group, Inc. 3.2%

Nissan Motor Co., Ltd. 3.0%

Canon, Inc. 2.8%

Honda Motor Co., Ltd. 2.8%

Japan Tobacco Inc. 2.8%

Mizuho Financial Group, Inc. 2.6%

Mitsubishi Corp. 2.3%

Takeda Pharmaceutical Co., Ltd. 1.9%

…The index “hedges” against fluctuations in the relative value of the yen against the U.S. dollar…"

The fact sheet goes on to compare the index against the MSCI Japan local Currency index.

So whether it is in fact physically hedging or emulating a currency hedge, the intent is there to have currency hedging.

But the WT index is slanted towards equities with global revenues. This is what causes me grief. How does this relate to the original concept of trading country funds? It looks to me as if you are getting away from the purity of the original strategy. How meaningful is the weak currency ranking system for companies with primarily global revenues?

Anyways, it is your system, you chose to post here, presumably for comments, and I’ve commented ![]() I like the system but think the choice to use DXJ is not the greatest.

I like the system but think the choice to use DXJ is not the greatest.

Steve

Miro - I used the same 6 currencies as Geov used. The ranking system is EMA(50)/EMA(250) with lower values ranking higher. How did you generate your graph, and what is the securities universe (i.e. is it currency ETFs)? Do the buckets on the right represent weakest currency ranking?

But that’s not what he did. He picked 5 unhedged and the 6th hedged, merely because it performed better. I’m not smart enough to say which one is supposed to work better but if you’re following a pattern that makes logical sense and then go against it at 1 time (because it backtests better), that’s curve fitting.

Miro, I get similar nonsense results for currency rankings as Steve. Would like to know how you got those nice rankings for currency ETFs as well.

Miro - I have made my ranking system and two ETF universes public for you to play with. This way there can be no Apples to oranges confusion.

Ranking System: https://www.portfolio123.com/app/ranking-system/298169

Country ETF Universe: https://www.portfolio123.com/app/universe/summary/213298?st=1&mt=12

Currency ETF Universe: https://www.portfolio123.com/app/universe/summary/213299?st=1&mt=12

Steve,

I guess for formula $StrengthXXX you used EMA(50)/EMA(250) of the currency ETFs as per your earlier posting.

My apologies… Custom formulas are used to overcome maximum characters in the rule. Here are the formulas:

$StrengthFXA EMA(50,0,GetSeries("FXA"))/EMA(250,0,GetSeries("FXA"))

$StrengthFXC EMA(50,0,GetSeries("FXC"))/EMA(250,0,GetSeries("FXC"))

$StrengthFXE EMA(50,0,GetSeries("FXE"))/EMA(250,0,GetSeries("FXE"))

$StrengthFXS EMA(50,0,GetSeries("FXS"))/EMA(250,0,GetSeries("FXS"))

$StrengthFXY EMA(50,0,GetSeries("FXY"))/EMA(250,0,GetSerie("FXY"))

$StrengthUUP EMA(50,0,GetSeries("UUP"))/EMA(250,0,GetSeries("UUP"))

I don’t think there is any way to predict future currency performance based on past currency performance. Also it depends very much on the time frame of the backtest.

Best I found was to use past country ETF performance in the ranking system,with higher being better, to simulate currency performance.

Geov - I agree with that, although I believe that currencies tend to trend more than equities, thus there is more persistence (momentum).

On the other hand, currency strength does have some level of influence on future equities price performance i.e. currency weakness will give a boost to profits, at least for export firms, profits that don’t show up until next quarterly report… This is why I think there is potential with your system.

Hi Andreas, I checked out most of the mentions on your list.

Is there anyone else with a fundamental data approach similar to Hedgeye that you’re familiar with? It seems so much of the macro is technical in nature, but I’m attracted to the modeling approach that’s rooted more in economic data. Hedgeye’s view is also divergent from the technical viewpoints I’ve seen. The recent call on interest rates and EM has been intriguing so far. One of the Hedgeye analysts also views China bearishly as leading indicator for the global economy, but not much of that has shown up in the US market yet, so another interesting theme to watch.

Some of what worries me is the self-promotional, and almost self-congratulatory nature of some of the material. That style of presentation tends to be a red flag for me, but I do find the approach quite interesting. Unlike anything else i’m familiar with.

Also, have you subscribed to their newsletter or any of their material? If so, I’d appreciate thoughts on it. thanks,

This, of course, assumes that the company’s input costs are primarily domestic and output sales is primarily export. FX changes would have the opposite effect on a company which has large non-domestic input costs with majority of sales domestically.