Regarding microcaps, my approach is never to look at past prices when choosing stocks. I look at value, quality, volume, growth, sentiment, size, sector, etc. But never momentum or 52-week low or mean reversion or any technical indicators at all. I have no idea what prices my stocks traded for in the past and I don’t care. I do look at the past few day’s prices when I set my limit orders, but that’s it. So “timing” is only an issue if the price is rising so fast I’ll miss out on my valuation multiples when buying, or falling so fast that selling no longer looks like the best option. If you ever consider getting back into microcaps, my advice is to concentrate on fundamentals, volume, and sentiment.

With ROBUST modeling I doubt that I or anyone else is going to get a 40% backtest return on a R1000 portfolio with a quarterly hold. I may be wrong, but the last thing I want to do is offer a non-robust model and cross my fingers that it’ll do well. I want to offer only models I’m very confident in, and that means sacrificing some backtest returns. For example, I never backtest a portfolio of fewer than 50 stocks. I could achieve great results for a smaller portfolio, but they wouldn’t mean much going forward.

To be clear, I still by micro caps, but I don’t buy nanocaps. My microcap universe starts at $250MM in market cap. My previous experience was with nanocaps below that level. My point on the pricing was that these nanocap stocks showed backtested returns that were much, much higher buying Monday’s open than Monday’s close or the average. Not that price mattered directly. I had a bunch of screens that showed a 60-80% return from the open, but it might only return 30-40% at close. There was no real world ability to duplicate these models, unless you were in and out at that open.

The 40% target was monthly in my mind. Quarterly would obviously be lower. Regardless, I don’t understand your comment on robustness. What is your definition of that? How is one model more robust than another? I develop mine and then test them forward out of sample for at least 5 years. I use the same methods for all.

I also think that 50 stocks is way to many to trade. I do agree that you could never hit any decent returns on large caps at that level. I try to do 5 stocks a week, rolling 5 weeks to 25 positions. Under those conditions, you can hit some nice returns that are longer hold and actually executable. For microcaps under these conditions I am close to 40%. For largecaps its closer to 25%, but I haven’t testing that many factors and believe much higher results are possible.

If your model has 50 stocks traded weekly, then I don’t think anyone will pay for that.

I’m sorry I didn’t make myself clear in my last post, and I probably misread yours.

What I meant to say was that when evaluating or developing a strategy, I never backtest a portfolio smaller than fifty stocks. But when it comes to actually investing or showing my results to someone, then I’ll use a much smaller sample. The reason for this is that if you optimize your strategy by backtesting with only a small number of stocks, your results will have a lower chance of persisting, and you’re too liable to make changes to your system that won’t benefit its out-of-sample performance.

For example, let’s say you came up with two different systems, one for fifty stocks and one for five. The fifty-stock model shows a return of 25% per annum and the five-stock model shows a return of 40%. Would it be better to invest in the five-stock model or invest in the top five stocks of the fifty-stock model, even if a backtest run on those only got you 30%? I would argue for the latter, unless you could expand the five-stock model into a fifty-stock model that got better results. I wouldn’t offer any top-five, top-ten, or top-fifteen designer model unless I arrived at it through top-fifty or top-hundred backtests. That’s what I mean by robust modeling.

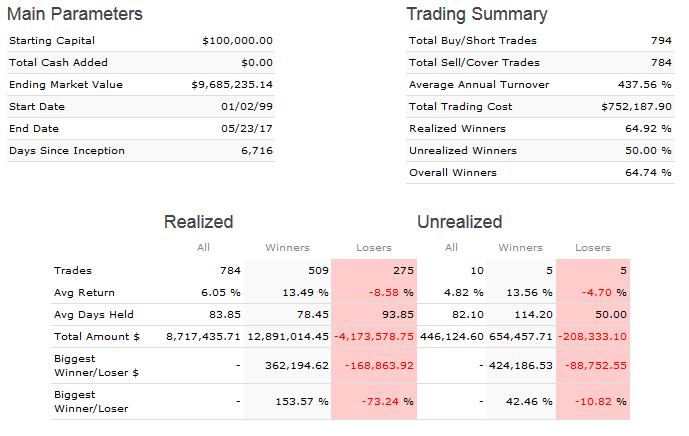

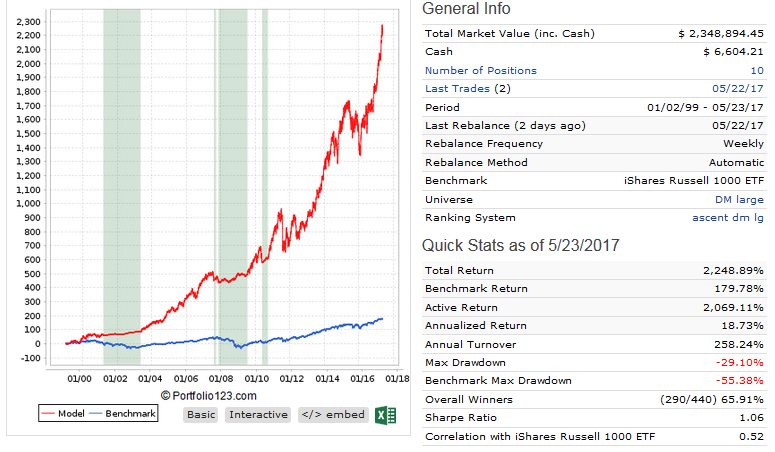

For what it’s worth, I recently did a correlation study of thirty similar strategies, testing them over eight different eight-year periods and comparing the results to the subsequent three-year periods. The eight-year tests were done with varying portfolio sizes ranging from 20 to 400 stocks. The subsequent three-year periods were with baskets of twenty stocks. The highest correlation of the thirty different strategies, by far, was when the first portfolio was in the 45-to-105 stock range. See the results below. Now I’m not saying my results are definitive, and they might vary some depending on universe size, the type of strategy being tested, the size of the “subsequent” baskets, etc. But that’s where I’m coming from.

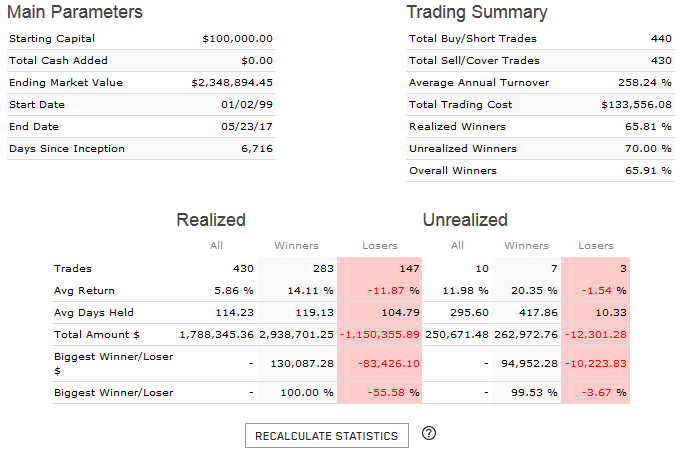

Your real-world results impress me, and I respect your years of experience. I don’t get appreciably different results for my microcap and nanocap strategy when I backtest at the open, the close, or the high-low average. Maybe that’s because I’m backtesting large portfolios. As for my results, I’m getting over 50% per annum on my microcaps since 1/1/16, which is two months after I started using P123’s ranking systems.

You may want to think about this in another way. You spent a LOT of hard work developing excellent models. Instead of considering how much profit subs will make, consider how much MORE you can make. If you offer 1 microcap model for $25 to only 10 sums and it is successful out of sample, you will make $250/month, $3000/year, for no more effort than you have already spent. If you launch 5 $25 small cap models, with $1 Million or more liquidity and 20 subs each, you can have a total of $2500/month and $30,000/year. That is not pocket change. And for no additional work. The difference at $100/month is that you will have VERY few subs unless you systems outperform every other Designer Model out of sample. Consider the TWY 5 stocks HG EMA 11 SYS model at 323% gain over 4 years out of sample. It only has 10 of 20 subs at a cost of $88/month.

When an investor signs up for ANY mutual fund, ETF, or any other type of successful investment system, that investor is profiting from the hard work of the people that developed those systems. Why should you expect to be any different? Especially since there is minimal additional effort on your part and it won’t effect the profits you make on your systems.

And I wonder if you systems are all that different from many others on P123. Have you compared your holdings to the list of tickers in “Popular with our Users” on the P123 home page? Or the “This week’s top stocks in Portfolio123 models” list in the weekly Portfolio123 Weekly Performance Report? I always find 20 to 30% of my holdings listed there.

This is good advice indeed, and I thank you. I don’t know whether it’s realistic to expect such a lot of subscribers, but I might as well try. I do need to adapt my present systems for designer models since with a higher liquidity limit I’ll be emphasizing different factors.

My system is indeed very different from those of other users. I don’t have a single one of the stocks in the “popular with our users” list, nor do I have any of the stocks on the “top stocks in Portfolio123 models” list. My top seven holdings right now are INTT, ALSK, STRM, JIVE, CNTY, MEIP, and BASI. I don’t think those stocks are very highly ranked in most people’s models. Their QVG ranks are mostly pretty low: 60, 66, 30, 38, 98, 44 and 30 respectively.

How comfortable are subscribers with buying stocks that sell for under $3? There are plenty of good stocks with ADT over $500K but prices under $3 (e.g. VVUS). Should I put a lower price limit of $3 or $1 on my universe?

The overall return for QLD/SSO with basic market timing might be 20-30% but it will be quite volatile. Large cap designer models don’t have as much OOS but provide much less volatility - should be able to get return in the 20’s w/basic market timing.

Let’s say I launch a designer model that rebalances every three months. Does a new subscriber then wait until the rebalance in order to get recommendations? Or does the model recommend the held stocks? If the subscriber subscribes two months after the last rebalance, is there a way for her to get the top ten ranked stocks as of that date rather than the top ten stocks two months ago?

Can I change the ranking system regularly as I get more and better ideas and do more backtesting? Or is it set in stone once I launch the model?

Looking through all the designer models with a decent number of subscribers, I can’t find a single one that rebalances less frequently than weekly. Maybe a 3-month rebalance wouldn’t get subscribers because of the above problem and I should just offer weekly rebalanced models?

I am interested in your weekly rebalance models in Smallcap & Midcap.

One of the boon in p123 is weekly fundamental data. If any model take the advantage of timely data and perform in out of sample, it will attract more subscribers.

[quote]

How comfortable are subscribers with buying stocks that sell for under $3? There are plenty of good stocks with ADT over $500K but prices under $3 (e.g. VVUS). Should I put a lower price limit of $3 or $1 on my universe?

[/quote] I ALWAYS use a universe of >$1 and I don’t use a buy rule greater than that. In my mid and large cap ports I very seldom have a buy recommendation less than $3 so for those it probably doesn’t mater much depending on the design of your ranking system.

Of my 3 micro/small cap ports, my ranking systems include a Close(0) factor set to lower is better. I just downloaded the Transactions; All page of the 3 ports to excel, ordered them on Price, and compared the stocks that were bought with a price < 3 to those bought with >= 3.

18% of the stocks had a price < 3 and of those the % winners was 67.3%. While the stocks with a price >= 3 had a % winners of 64.6%. that’s not a big difference, but it implies there is not a good reason to limit the stocks to a price >=3.

3 months rebalance model might have good number of savvy subscribers.

They will subscribe once in 3 months using last rebalance date + 3 months.

Just they need to subscribe for the rebalancing months. 4 times a year.

Well, I just launched three designer models. They’ll be available for subscription in three months, on August 20.

But I’m quite dismayed by two things.

I defined my three models by market cap, using the conventional limits: up to $1 billion for small and microcaps, $1 to $5 billion for mid caps, and over $5 billion for large caps. But when I look at the holdings of my large-cap model they’re all classified as mid-caps and when I look at the holdings of my mid-cap model they’re all classified as small caps because of the way P123 uses a percentage ranking and because of how expensive stocks are nowadays. So it looks like the very NAMES of my models are lies.

The stocks are ranked by momentum, value, and quality using P123’s conventional ratings. My picks are NEVER going to be near the top of those ratings because I use completely different measures. For my small cap models, the ratings are all in the 40s. This puts me at a significant disadvantage. Why should P123 impose their measures of value and quality on designers who might have entirely different measures? I use a LOT of measures of quality and value that P123 doesn’t use, and in my opinion, my stocks have VERY high quality and value.

I don’t know how much you can see of my models at this point, but they’re here:

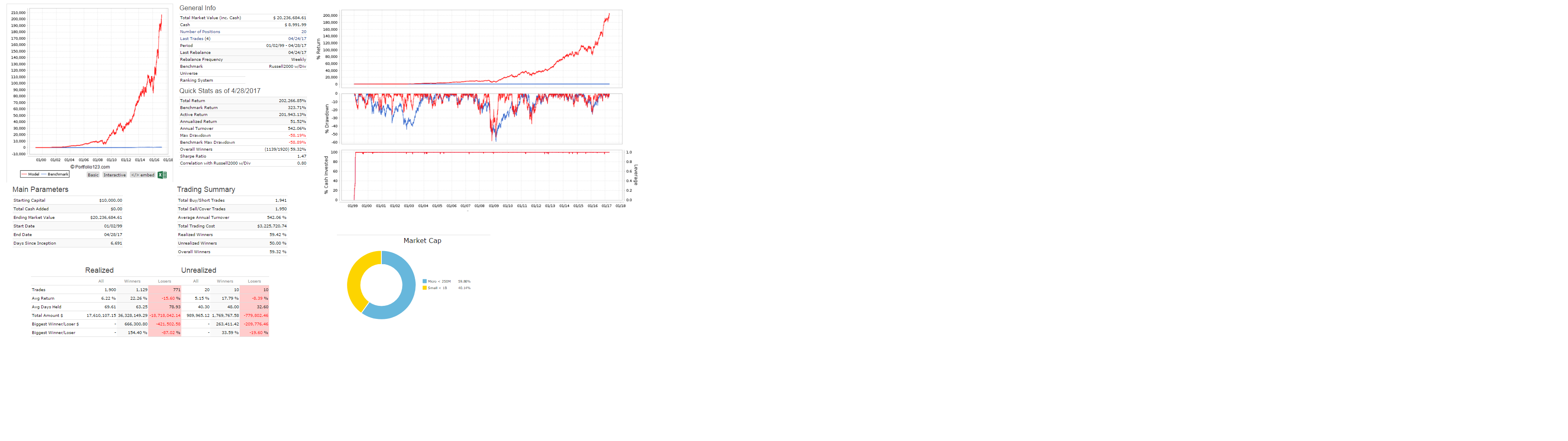

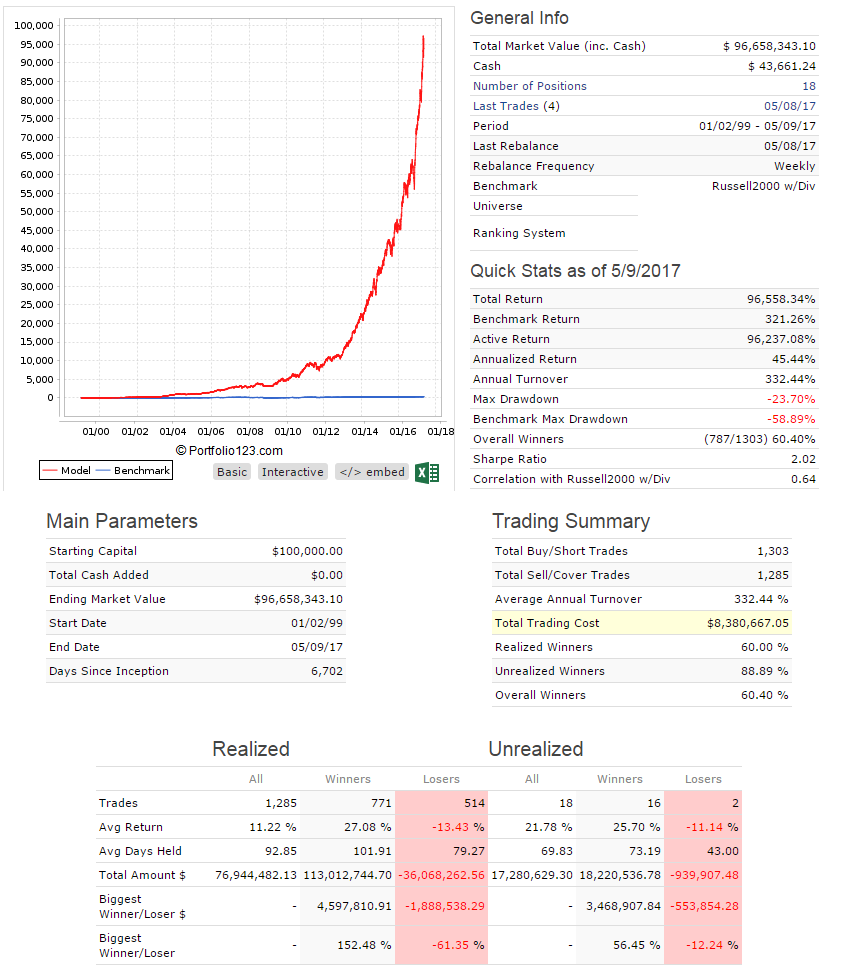

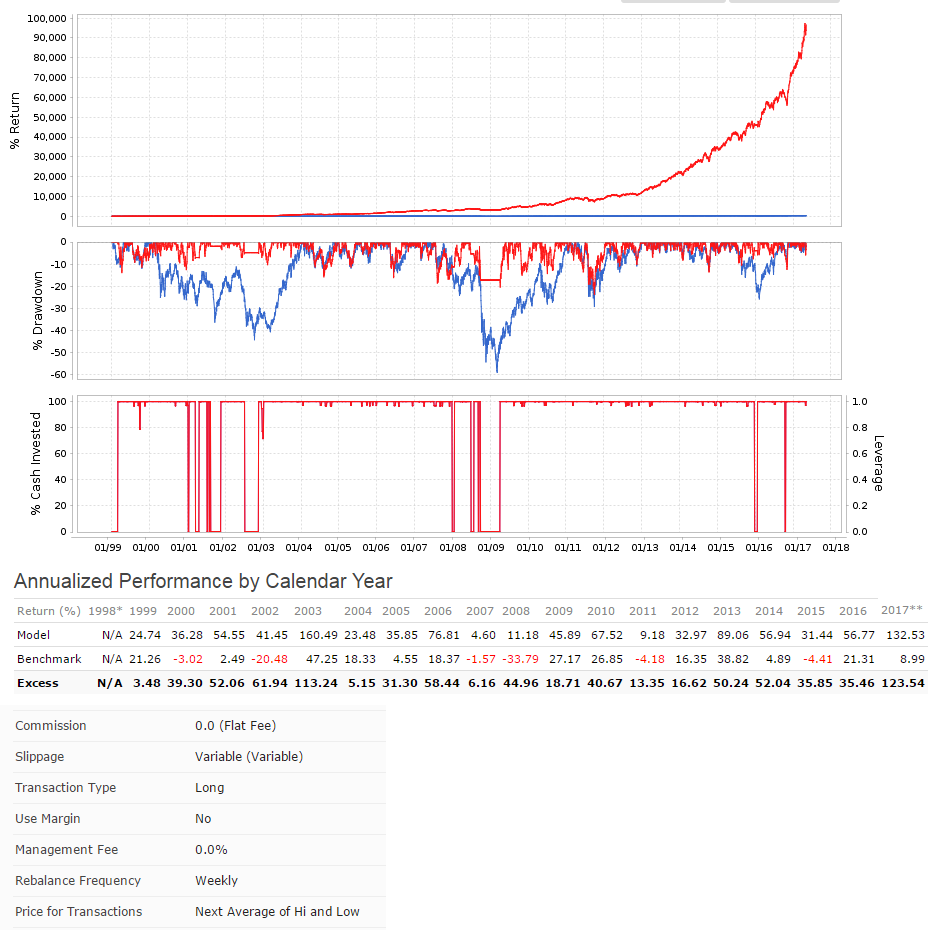

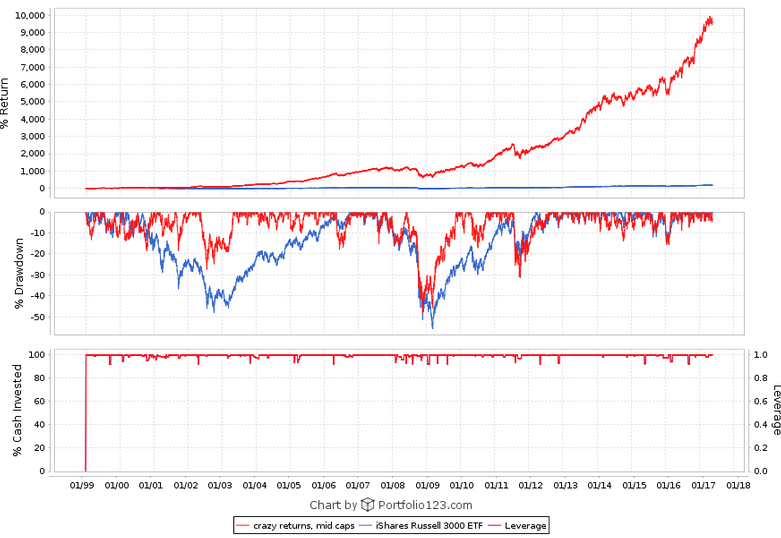

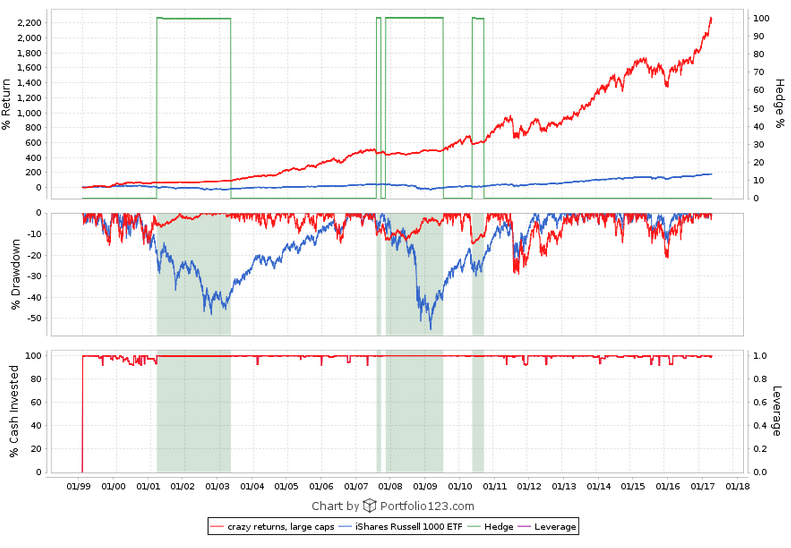

Here are the charts. The small cap model has a $500,000 minimum 3-month median daily dollar volume and a maximum market cap of $1 billion. The mid cap model has market cap limits between $1 and $5 billion. The large cap model is for over $5 billion. All three are designer models so they’re variable slippage and the buy and sell price is the designer model formula (part high, part low, part open, part close, I think?). You can get descriptions of them at the links I provided earlier.