Hi Doris, and welcome to p123 from a short-time member.

First, I must note that I am not a registered advisor of any kind and whatever I say I try to relate to my own situation, experiences, and financial beliefs. There is a wide range of users here, from totally inexperienced to very, a wide range of ideas as well, and you can get into it as deep as you want.

Second, I was totally off the grid for a couple of days and just saw your message. Hope you haven’t been signed in, refreshing every once in a while to catch my reply ![]()

I came here for the same basic reason, to grow retirement funds. I am totally retired now and depend on those funds to supplement social security and a small pension.

In general, I agree that using another model to expand the number of positions is a good idea. But it partly depends on how much money you intend to invest, whether you are currently retired or have several years at least before retiring (related to how much risk you are able and willing to take), and how much faith you have in each model. Models with fewer positions usually, but not always, outperform (or underperform, if the rules are bad) the same model with more positions. With a small amount of money and lots of time before needing to depend on it you might do better by not spreading it among models. As the money increases or the time to dependence decreases, the goal changes and spreading the money among models is probably a good idea. It’s probably an even better idea to first look at diversifying among asset classes rather than among stock models.

The model I use is my own private one, and I don’t currently intend to invest in a RTG model or build one. So I have not studied the available ones enough to suggest anything there. If you consider a RTG, do what you can to understand as much about it and its designer as possible and whether its goal matches your situation. There are some good designers here and some variety in models.

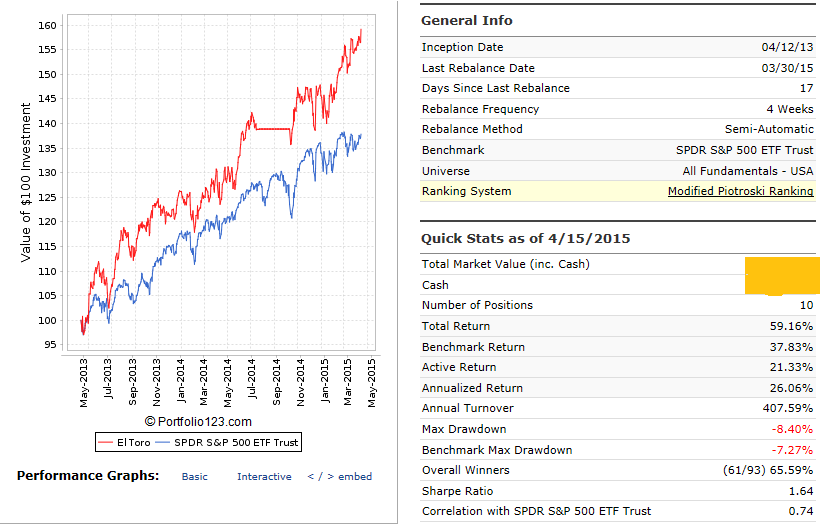

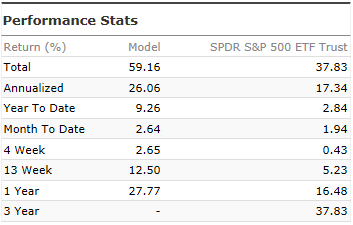

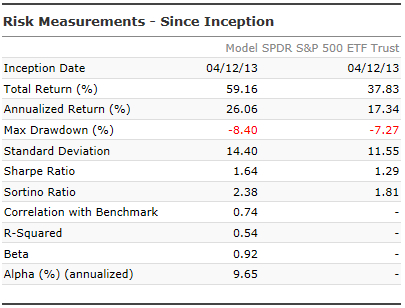

As for my own modeling and whether or not I have a second best choice versus the modified Piotroski approach I’ve used: The modifications I have made to the basic Piotroski model are attempts to tie together different approaches including the other All Star models, growth, sentiment, momentum and just about any other idea I come across. And I will likely continue to modify it as I find ideas that blend well with the existing model. I feel comfortable with the model so far and will likely expand its number of holdings to 20 or 30. If you want to attempt your own modeling, I suggest using your guest membership time to its fullest. You have the ability to run simulations and rankings for the entire data history, not just 5 years back. Look at the universes, ranking rules, and buy rules of the many prebuilt screens available and decide on a single starting model, then try refining it by bringing in attributes from others to see what effect is generated. There is a lot to consider at multiple levels (universe, rank, buy, and sell) and I used my guest subscription time to become somewhat comfortable with the process and do some full-length simulations, comparing them to the equivalent screen and finding suitable slippage for the screener that would be equivalent to commission charges in the simulator or portfolio.

There is also a wealth of information (and a lot of differing opinions about modeling periods and approaches) within the forums, as well as good stuff in the tutorials. This is an active site that I’m glad to have found.

I’m not certain there is a general consensus about technical timing, or even a consensus about what constitutes technical versus other approaches. I myself prefer to look for macroeconomic timing clues in commodity prices, inflation rates, borrowing costs, specific sector activity and such versus looking for changes in earnings, market momentum or volatility. I just want the holy grail - timing clues that occur before the market responds broadly. But when I can’t find those economic clues then I do consider the “technical” clues.

The one year results I posted of my model do not contain any out-of-market periods because the timing rules I’ve developed so far were not triggered. I expect to ride with most fluctuations but would like to avoid deep drawdowns of more than 20%.

I hope this answers your questions properly, and I hope you find what you want here. I’m sold so far.

Bob