Wallstreetbets would be proud.

1 Like

I was replying to my indexing rant/post. ![]()

No sarcasm intended.

Update:

Slight improvement compared to the last reading. These periods seem to be more favorable for factor investing, but results are still well below 50%.

36% of users managed to beat the benchmark over the past two years. Please note that the benchmark may be mis-specified for some DMs.

Interestingly, current market value (total revenues) of DM's market is 5014 USD/month. With more enhancements it will be easily bigger .... by allowing users better compare DMs and restricting Designers to remove DMs that do not perform.

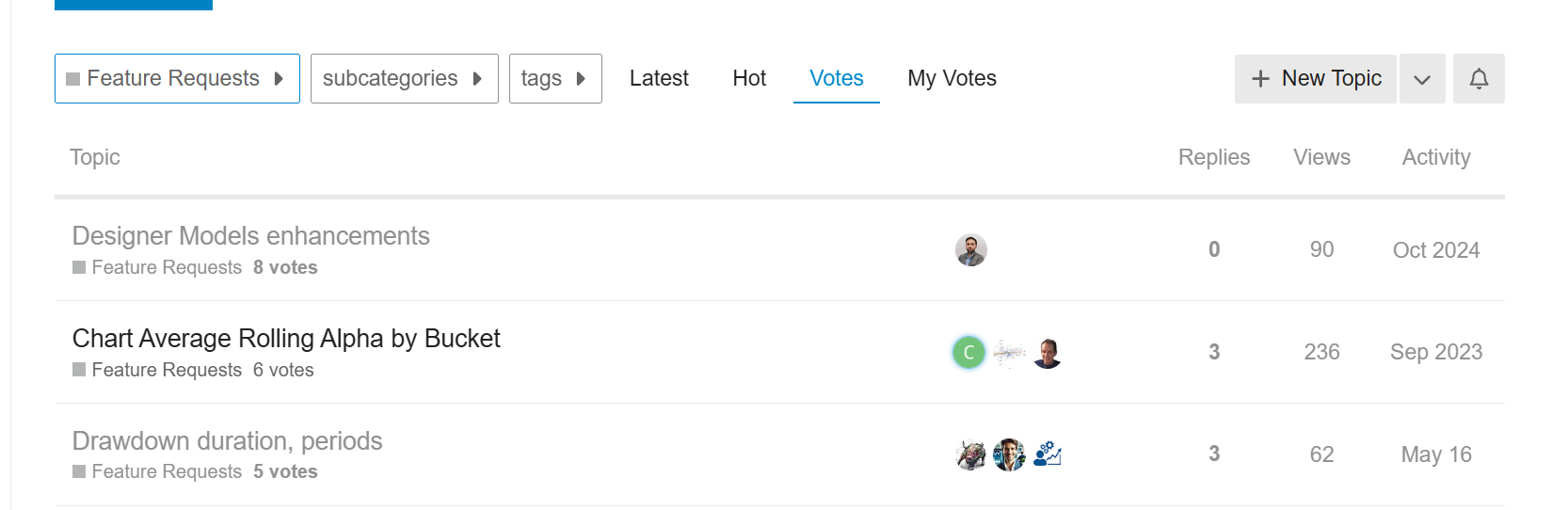

I’ve been waiting for the 10Y Return feature for quite some time. I believe it’s a three-hour job. Please vote: Designer Models enhancements

This is currently the top-voted request:

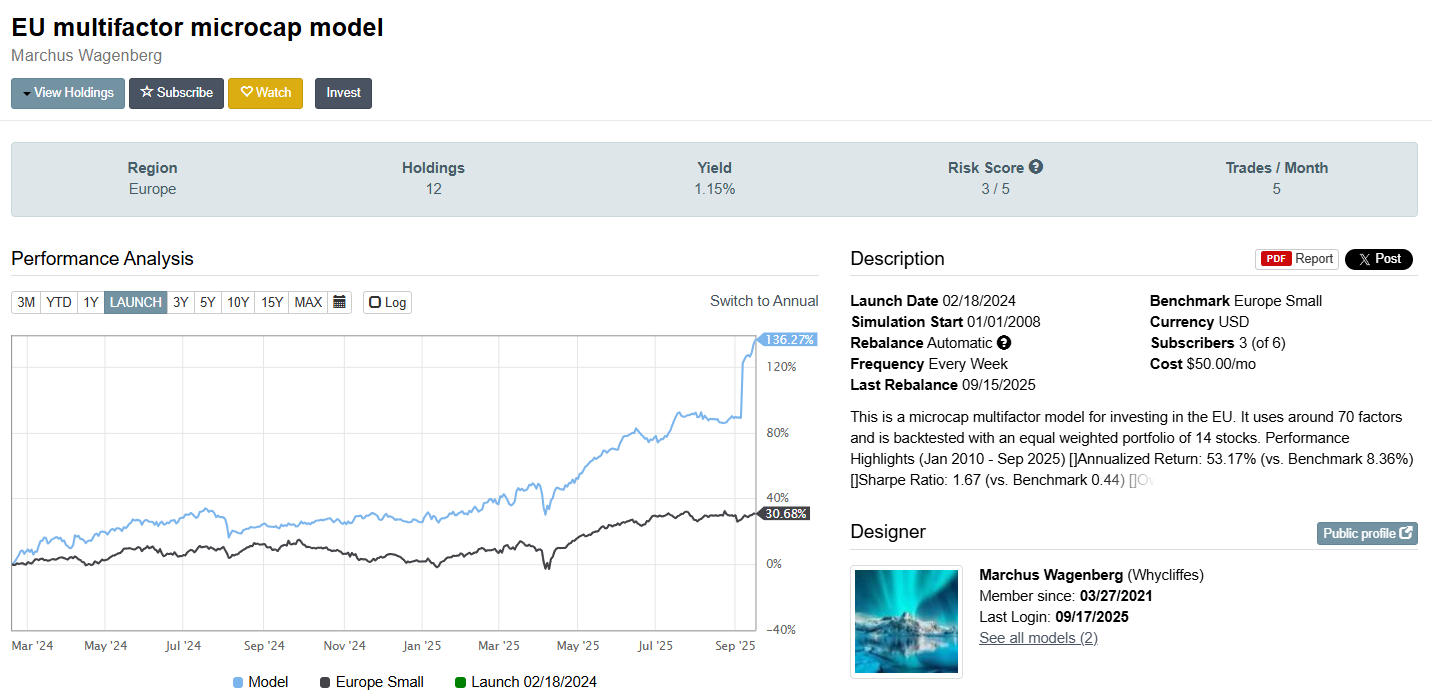

What happened here? ![]() (20% gain in one day)

(20% gain in one day)

The so-called lottery ticket has paid off – but that’s part of the game.

Congrats to Marchus, who is now the leader in the Europe segment! ![]()

4 Likes

It is part of the game, I think. Makes me wonder how we should handle outliers. Outliers have a real impact in live models.

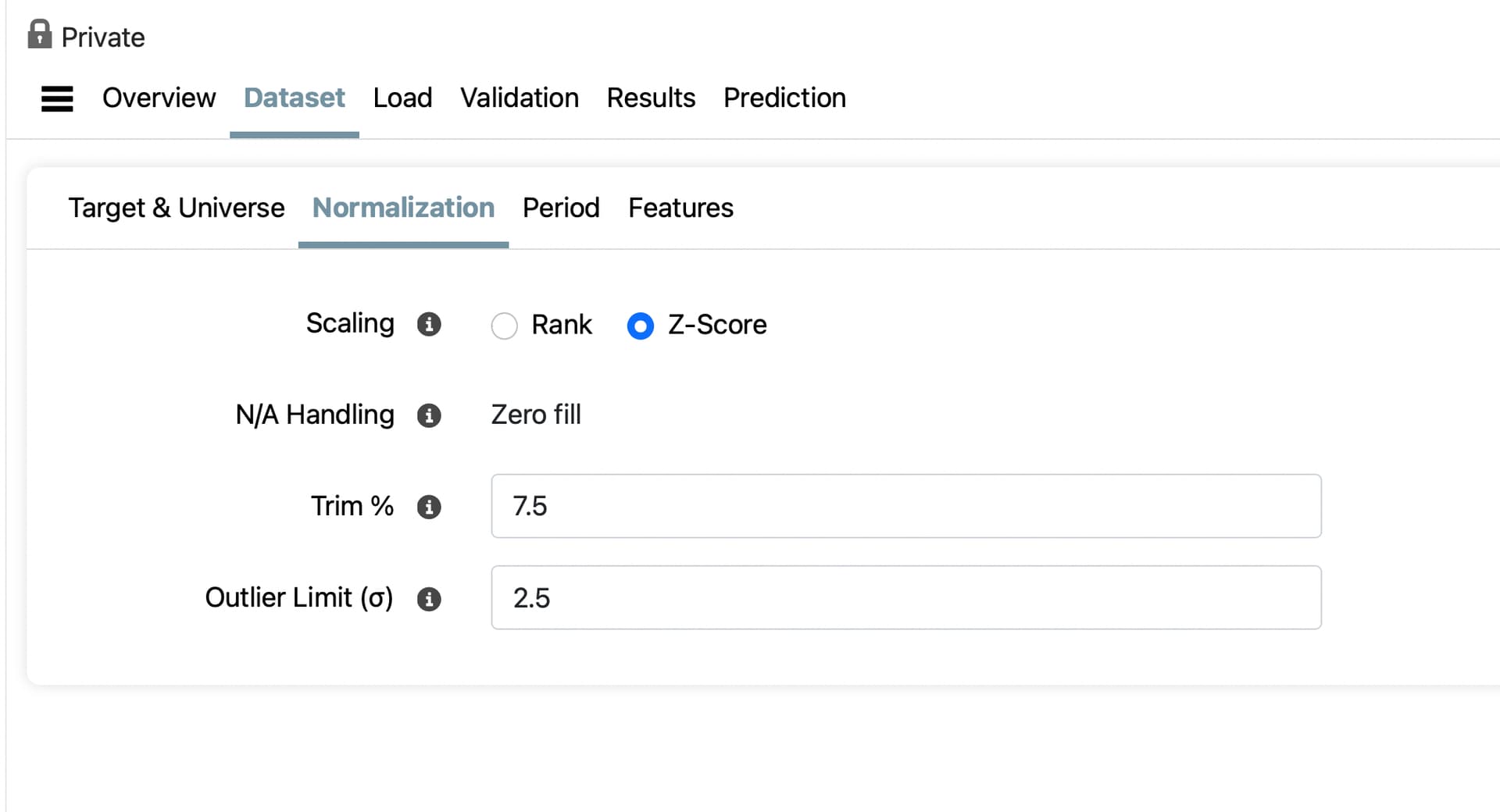

If the outlier is not an error in Factset’s data do we want to remove it at all? If so what is a good trim? We can change it, so what is a good trim for P123’s Z-score normalization?

If you use XGBoost is Huber loss a good way to handle outliers? Absolute deviations runs too slow for me. But do we even want to hide the effect of outliers if they are part of the game?

If we’re going to see outliers in real trading, shouldn’t we train on them — unless they’re truly one-off events?

Pretty sure I don’t know the best way to do it. but I think that data point would be removed in training if you used the default z-score normalization:

1 Like

Congratulations on the strong performance ![]() ! @Whycliffes

! @Whycliffes

Really impressive to see how you’ve positioned yourself and captured that growth. I noticed you’re investing in Turkey — that’s not so common, since access through Interactive Brokers (IBKR) to Borsa İstanbul can be quite limited for most retail investors. Did you go through a local broker, or perhaps use ETFs/funds with Turkish exposure? Would love to hear your approach — it could be very insightful for others looking at emerging markets.

1 Like

Hi, thanks. Yes, the system has done well and has captured most of the returns during a period when the portfolio was registered in EUR, and therefore I didn’t experience the change between EUR/ USD (12%). That said, even though I believe it is a good system, and I use most of the criteria in my own system, it is over a very long OUS-time that the systems will show their value.

But I chose to include Turkey because it seems that some have access to the market through IBKR, but I myself cannot trade there. However, I have done quite a few tests of the ranking system on other market compositions. Among others, the ones I trade in Europe, and the returns are not very different. I will publish that a bit later.

But take a look here: https://brokerchooser.com/turkey

1 Like

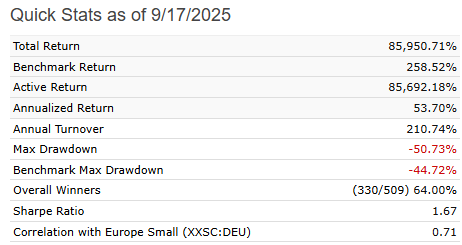

We are revising the performance for this strategy. There was a 17% jump because there was a model revision that changed the currency from EUR to USD. This is not supported and should have given an error, but it got changed because the revision logic is not checking.

This means that the performance of this model is around 17% lower for this year. Still a very good model, but maybe not the leader? We’ll see. We’re in the middle of fixing the problem.

Also, we will disallow revisions that change currency in the future. Sorry about this.

4 Likes

The 1Y performance dropped from 90% to around 60% which means the model will lose its current #1 spot after tonight’s update.

Projected placement is 3rd depending on its performance and Yuval’s model performance today.

1 Like

Good! I was also surprised by the sudden jump and tried last night to review which transactions could have caused it.

However, it should absolutely be permissible to change the currency cross.

This is because the model was originally set to EUR by mistake. Most of the other European designer models are set to USD and have benefited from the positive currency effect on their European strategy (13%). In addition, I think most of the platform’s users are based in the US or Canada.

I can, of course, restart the model with USD, but I really don’t like simply deleting older models and starting new ones. That has also been criticized many times here in the forum. It is better to improve and revise existing models and be transparent with those who choose to follow them.

The change of currency should never apply retroactively, as apparently may have happened here. It should only apply from the time of the revision.

Thank you, and yes, this is a good European model for now, and after the revision, even without the currency effect, a very good—with an equally weighted positioning—European model. However, I believe these models provide very little overall guidance as to whether they are good or bad until much more time has passed. ![]()

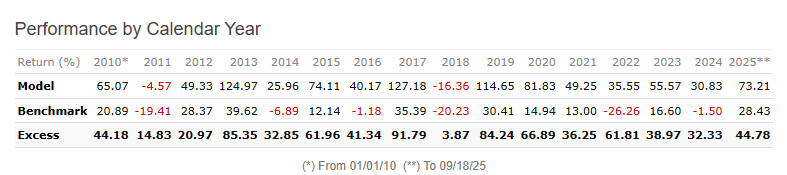

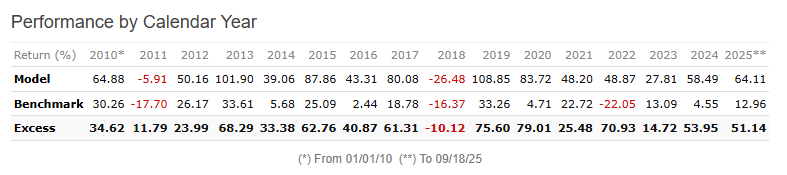

Here are the two models compared.

USD Based:

Eur Based:

1 Like

Thank you for clarifying this.

Therefore, congrats to Yuval, who remains the leader in the Europe segment!

@marco Could you also address the missing option to sort by ‘10yr Return’ in the main table?

1 Like

Europe can be tricky ![]() . Some countries carry relatively high corruption indexes yet still manage to deliver strong CAGR. I recall Yuval writing something about corruption indexes in a post. What’s interesting is that many of these markets still meet the minimum average volume requirements — what I half-jokingly call the “ADR of Europe.” Some of them are fairly reliable, others less so.

. Some countries carry relatively high corruption indexes yet still manage to deliver strong CAGR. I recall Yuval writing something about corruption indexes in a post. What’s interesting is that many of these markets still meet the minimum average volume requirements — what I half-jokingly call the “ADR of Europe.” Some of them are fairly reliable, others less so.

Then you have places like Turkey (just improving in terms of corruption, anyway): harder to access, but potentially very profitable if you know how to navigate them.

My own approach is to match the country I invest in with its local currency. That way, I strip out FX noise and get a clearer view of how the stocks themselves are actually performing.

Anyway, each one must do the corresponding due diligence where want to be invested ![]()

1 Like

Yes, I agree. I think the DM portfolios should have addressed this issue with currency crosses to a greater extent, and now with possible expansion into Asia on the horizon, this problem will become even more significant. Therefore, a solution where the DM portfolio subtracted currency gains or managed to match it against the local currency in the investment country would be great. ![]()

Currency was implemented as a read-only property across the platform due to technical constraints. Strategies and accounts are designed to support only a single currency position, so converting a model’s entire history to USD would be needed for it to function correctly. Preventing changes to currency when revising a Designer Model will align its behavior with the rest of the platform. (An internal tool which converts a strategy’s/account’s entire history exists, but it’s not something that has been exposed to clients.)

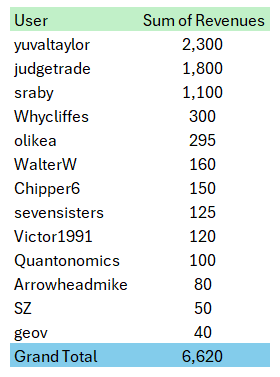

Top Users by monthly revenues.

Total (monthly) Market Value of DMs market increased from $5014 (Sept 2025) to $6620.

2 Likes

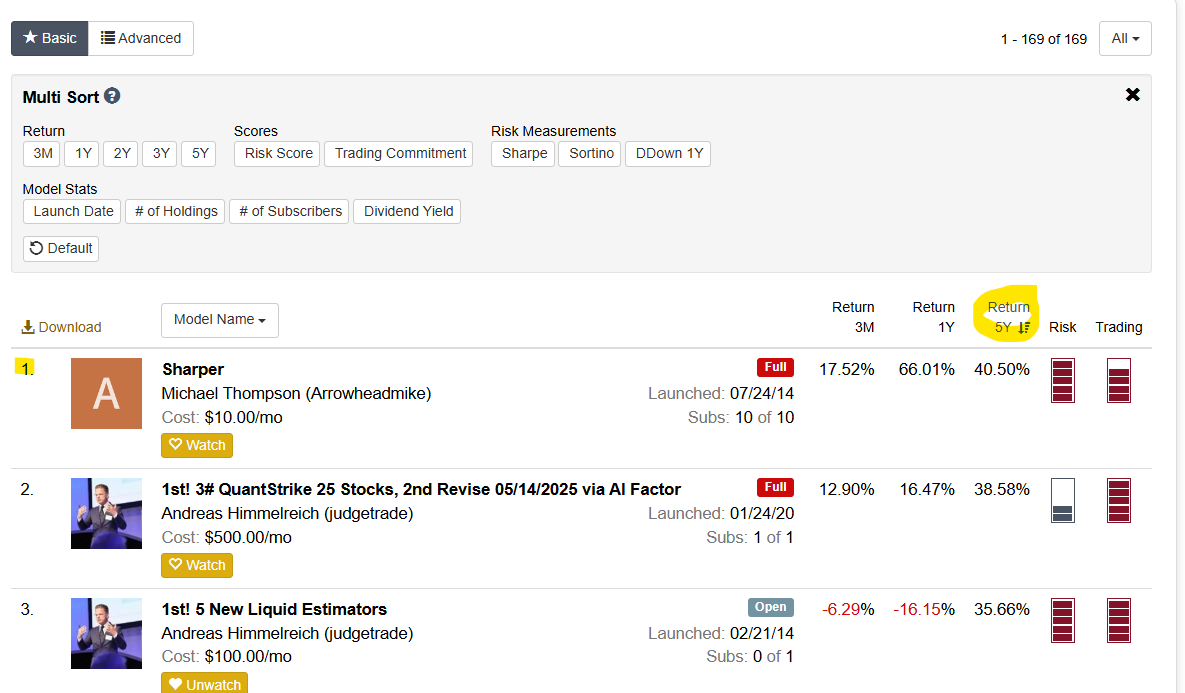

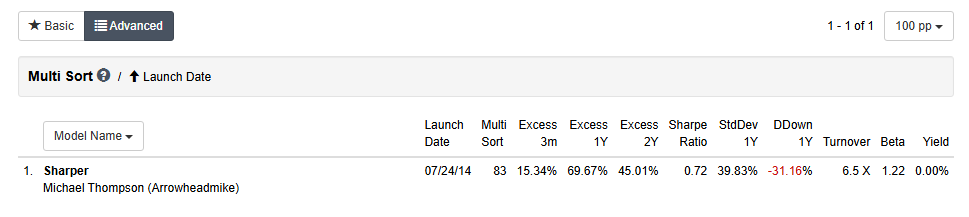

It finally happened after 1.5 years — we have a new leader based on 5-year CAGR.

The 10-year CAGR is still not available, but congratulations to @Arrowheadmike for taking the top spot ![]() .

.

Once all the promised new statistics are released, we should decide what the default performance metrics should be. In my view, 5-year or 10-year CAGR (with min. 15-20 stocks) is the most relevant metric for investors in their early or mid-investment stages.

Another useful category would be one based on risk metrics, highlighting models that excel on a risk-adjusted basis.

1 Like

Pitmaster,

I have some free time today and decide to take a deeper look at the designer models after your recent post. It is definitely not easy to find a designer model which outperforms the market in the long term.

Arrowheadmike DM performs well but it has a rather large 1yr drawdown of over 30% (all time MDD over 60%). I also noticed that he hasn’t log into the P123 platform for over 9 months.

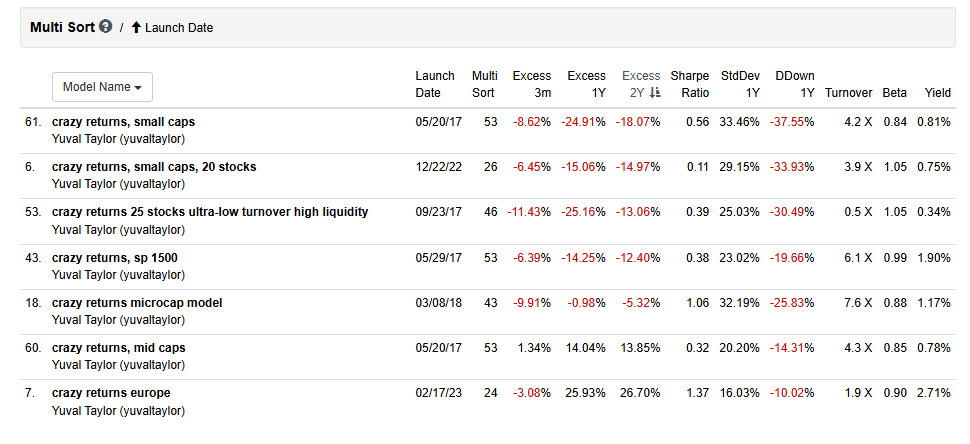

Even the designer models of our star in-house hedge fund manager Yuval is not doing so well (maybe due to the recent quant quakes/factor inversion) with the exception of Europe and mid-caps.

The judge (Andreas) seems to have removed the 1st New Liquid Estimators designer model from your screenshot. I follow the judge (Andreas) on X and knows that he is now focusing on developing strategies using the AI Factor (thus maybe the reason for the removal of the DM).

Andreas : If your AI Factors models are doing well, I have a suggestion for you. I will post again about a quant hedge fund named CFM which is based in Europe (same as you). Maybe you can approach them as they seems to be expanding very quicky.

Regards

James

1 Like

Indeed. Factor inversion plays a large part in this--and factor inversion isn't happening in Europe and Canada. Also I haven't revised any of these systems in years since I've been focusing on my hedge fund (which is up 54% YTD before fees).

4 Likes

Yuval,

I think 54% YTD performance for your hedge fund (Fieldsong Investment) is very impressive.

This is more than 4 times the performance of S&P 500 so far this year. (this should put you in the top 1% for all hedge funds that I have seen so far in the database.)

Great job and it is good to know that this kind of out-performance is achievable with Portfolio123.

Regards

James

EDIT:

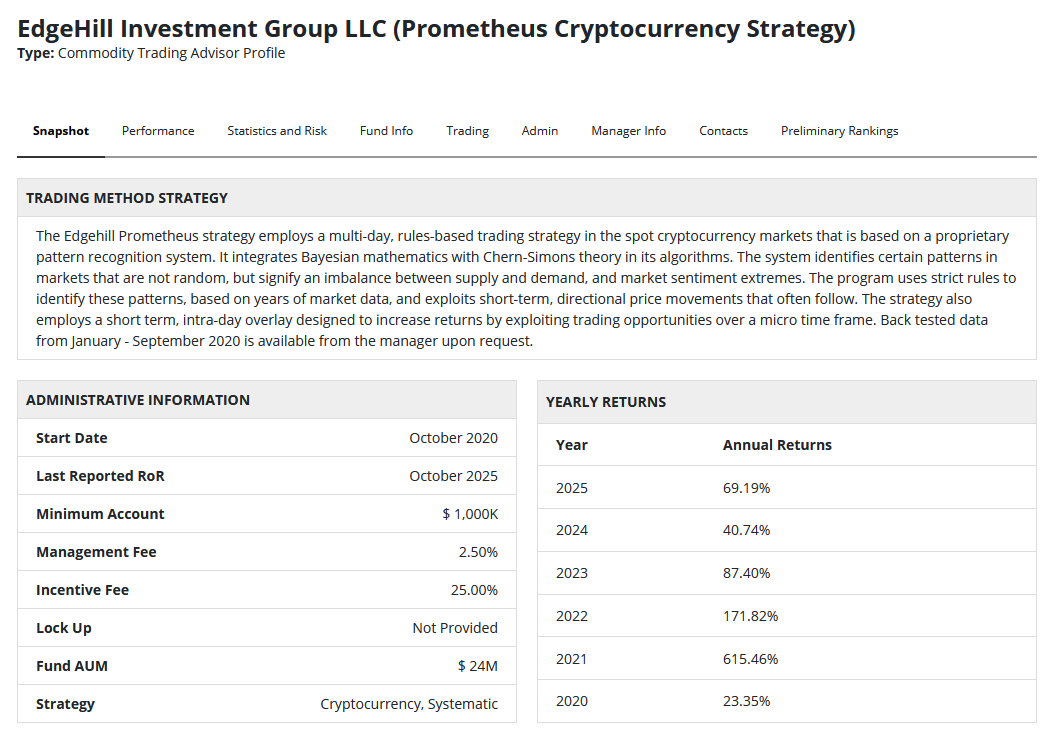

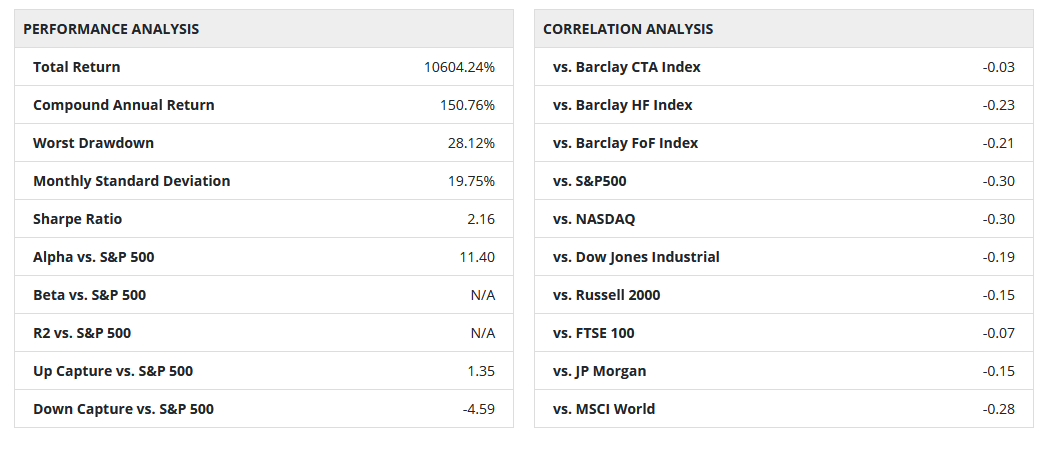

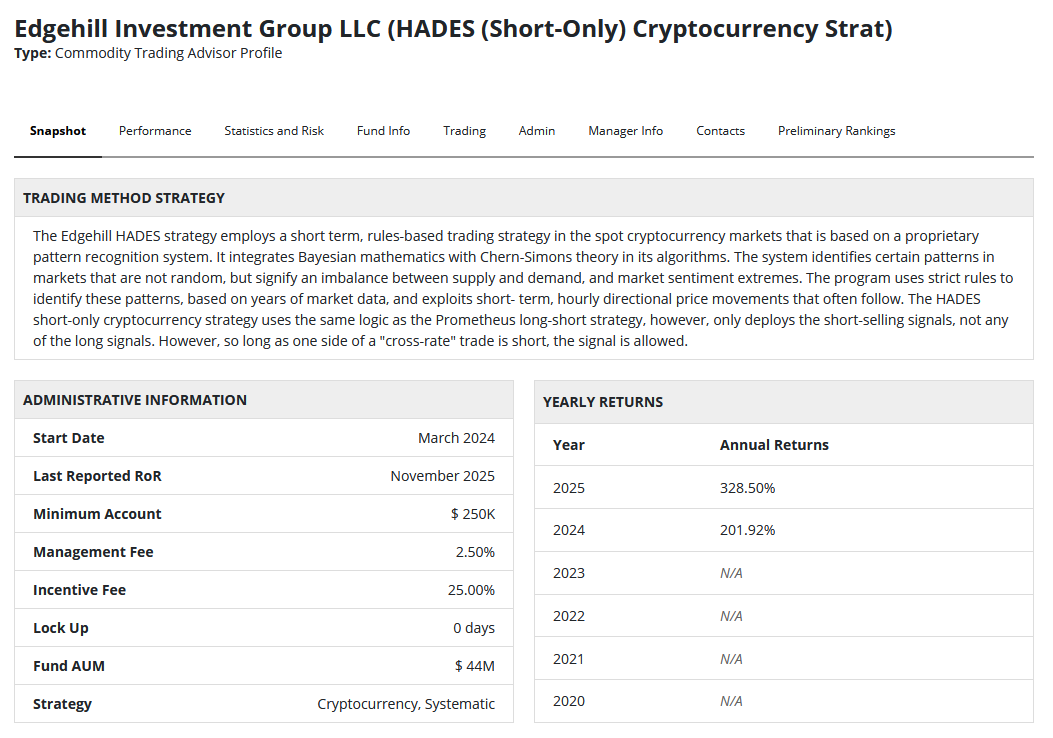

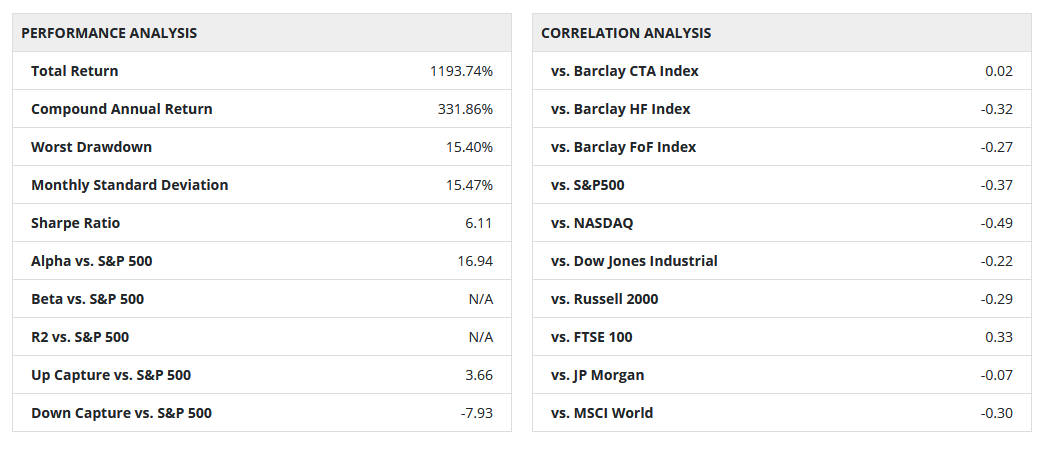

I already shared these with Korr a few months ago so it is no longer a secret. Two crypto hedge funds that did even better than Yuval year-to-date. (subscribe at your own risk, both funds are regulated by CFTC). The performance of the HADES version is better but a shorter history.

2 Likes

Speaking from experience in shopping the designer marketplace: because models can be optimized, retired, or affected by survivorship bias, the real edge comes from knowing and trusting the designer—far more so than any specific backtest.

An improvement to the marketplace would be placing more emphasis on the logic and rationale behind each model, as well as providing a clearer sense of the designer’s thinking, temperament, and quantitative approach. The brief model descriptions currently available don’t offer sufficient depth to evaluate robustness or philosophy. Giving designers space—and encouraging them—to explain why a model works and how they think about risk, construction, and ongoing maintenance would make the marketplace far more informative and useful than relying primarily on backtested data.

2 Likes