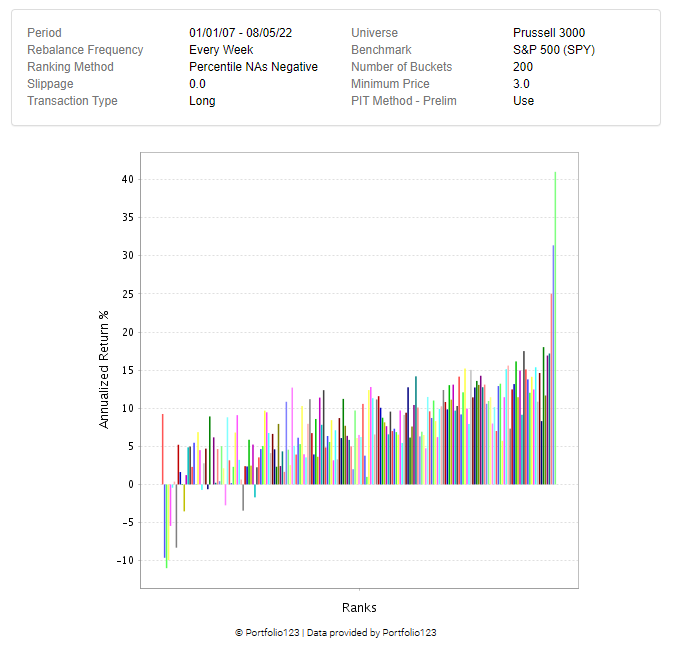

The one w/ the chart is based on a simulation trick. It can’t be run as a live strategy.

ha ha looks like i have a lot to learn. what is the simulation trick if you don’t mind sharing?

Close(-1) can be used in simulations to peek at future price.

Just an observation. It is possible to get a crazy annual return on a simulation with variable slippage and a reasonably liquid universe and trade it in real life. For example, if I run a simulation with variable slippage on a universe based on North American with a minimal daily dollar volume greater than $27,000 and a price greater than $0.50, using the same ranking system I use for trading stocks every day and a formula weight rebalancing method that weights higher-ranked stocks more heavily, with an average holding of 11 stocks and an average leverage of 1.03, I get an annualized return of 78% since 1999 (with 8X turnover). I know, however, that simulated returns are usually optimized to some degree, and I don’t expect to make anywhere close to 78% per year. (My CAGR since late 2015, when I started using ranking systems with P123, is 46%, and I expect that number to drop.) I also know that the bigger my portfolio gets, I either have to hold more stocks or trade more liquid ones.

So my advice is this. Don’t discard your model just because the returns are crazily high. But always test using variable slippage (or some other slippage percentage that’s reasonable)–just because you up your liquidity doesn’t mean you can trade without slippage; always vary your testing by tweaking your universe, ranking system, and so on; aim for lower turnover systems; and don’t expect your real-life trading to be as profitable as your simulations.

I think you’re on the right track!

1 Like

To that point, is there a rebalance rate and turnover % that is recommended/tolerable?

Personally, I wouldn’t recommend going above 1000% turnover, and wouldn’t recommend rebalancing more frequently than weekly. But that’s just me; others might have different ideas.