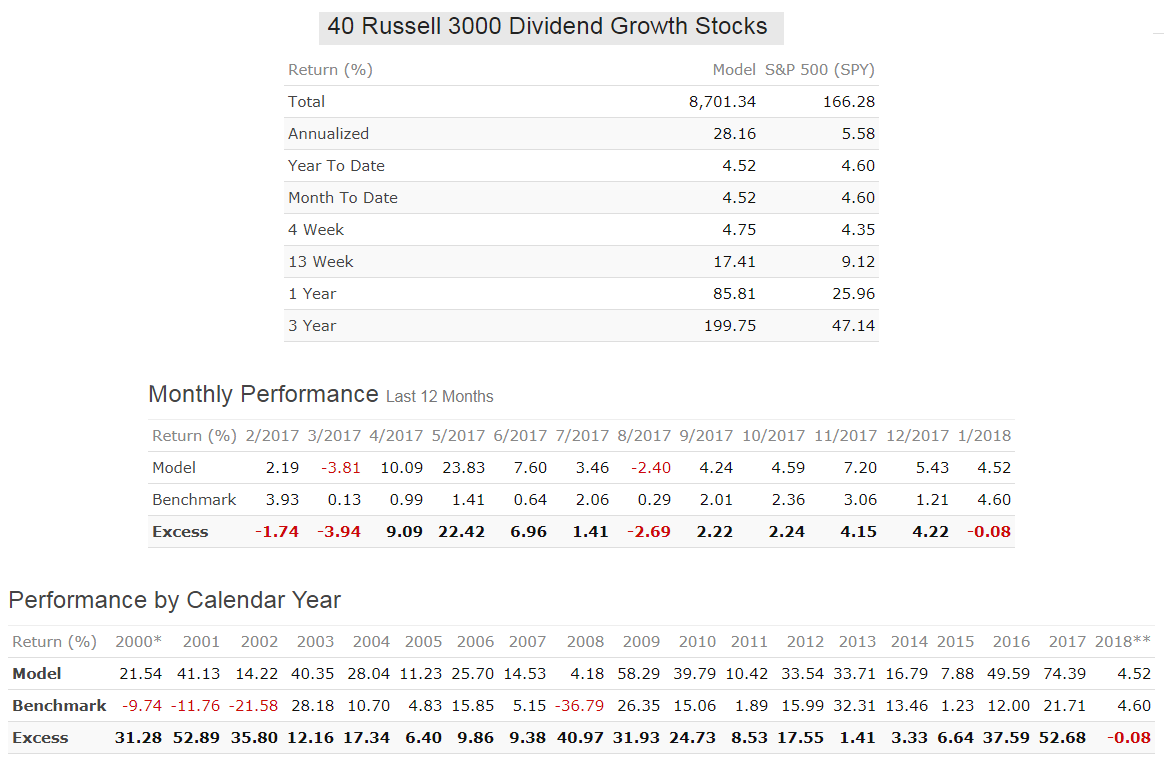

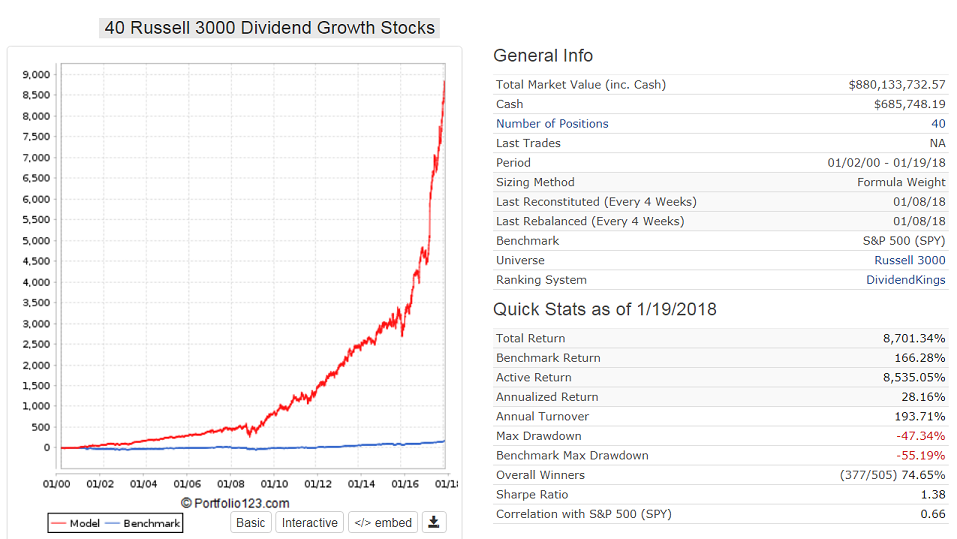

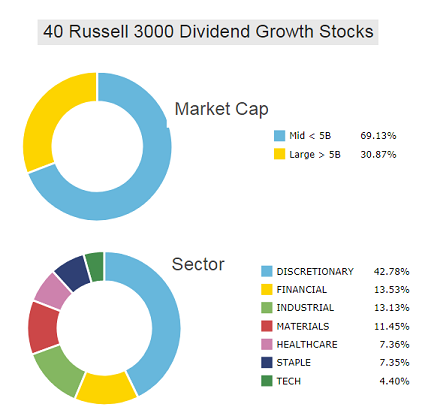

You don’t have to concentrate on the small caps. Here is a 40 position model, low turnover of 190%, annualized return= 28%, and no market timing, with the smallest MktCap of a position > 1-Billion.

Never made a loss over a calendar year.

You don’t have to concentrate on the small caps. Here is a 40 position model, low turnover of 190%, annualized return= 28%, and no market timing, with the smallest MktCap of a position > 1-Billion.

Never made a loss over a calendar year.

Having been at this a while, and having greatly underestimated the slippage and volatility of small / micro caps, I have been focused much more on the mid-cap space. It seems that a great backtesting larger cap model, like Geov’s, will at worst market perform out of sample, while a great backtesting small/micro model could completely blow up out of sample.

My other source of confusion, is the desire to go so small that institutions are not interested. I would think you would want to find stocks where institutions can play, as they are the major drivers of price. Being a small fish, you can get in and out of stocks where institutions play without impacting price, as opposed to stocks, where institutions can’t play and are much more subject to volatility and even manipulation.

Here’s an article from Seeking Alpha this morning. By their analysis, price-to-book was the best value factor in 2017.

https://seekingalpha.com/article/4138638-value-2017-worked-wall-street

It all depends on how thoroughly the model has been tested, in addition to a very large number of other factors. Mid-cap and large-cap models can fail too.

But institutions ARE interested. Almost all the stocks I invest in have institutional ownership percentages greater than 25%, and a number of them are greater than 80%. OK, I do own shares of some companies like GSL and BASI, with institutional ownership only 5%. But I also own lots of shares in NWY and FWP, with institutional ownership near 90% to 95%.

By the way, what kind of “manipulation” do you see happening in the microcap space? I haven’t come across any myself, but maybe I’m not looking hard enough.

The post on NHLD come to mind the other day. The stock shot up like 60% then came crashing back down. It doesn’t take much to send a thin stock flying around for seemingly no good reason. To each his own. My small cap experience has not been good, and one key to investing success is knowing your personality and what fits it. I wouldn’t rule out a microcap model, but it wouldn’t be more than 20% to 30% of my overall equity exposure.

The other question is how much effort is required for good performance.

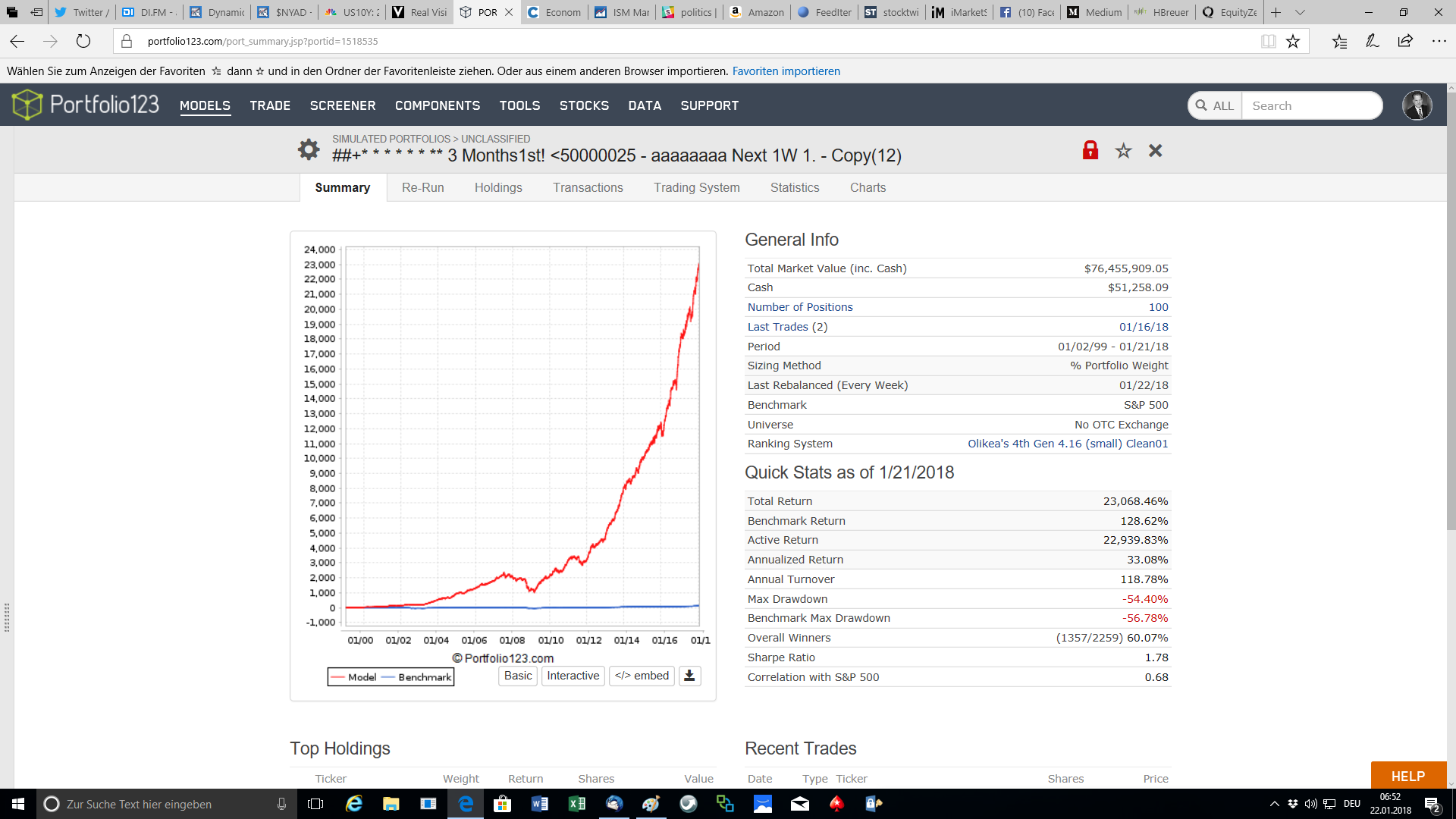

Yuval’s small-cap model shows 3,345 trades and weekly rebalancing.

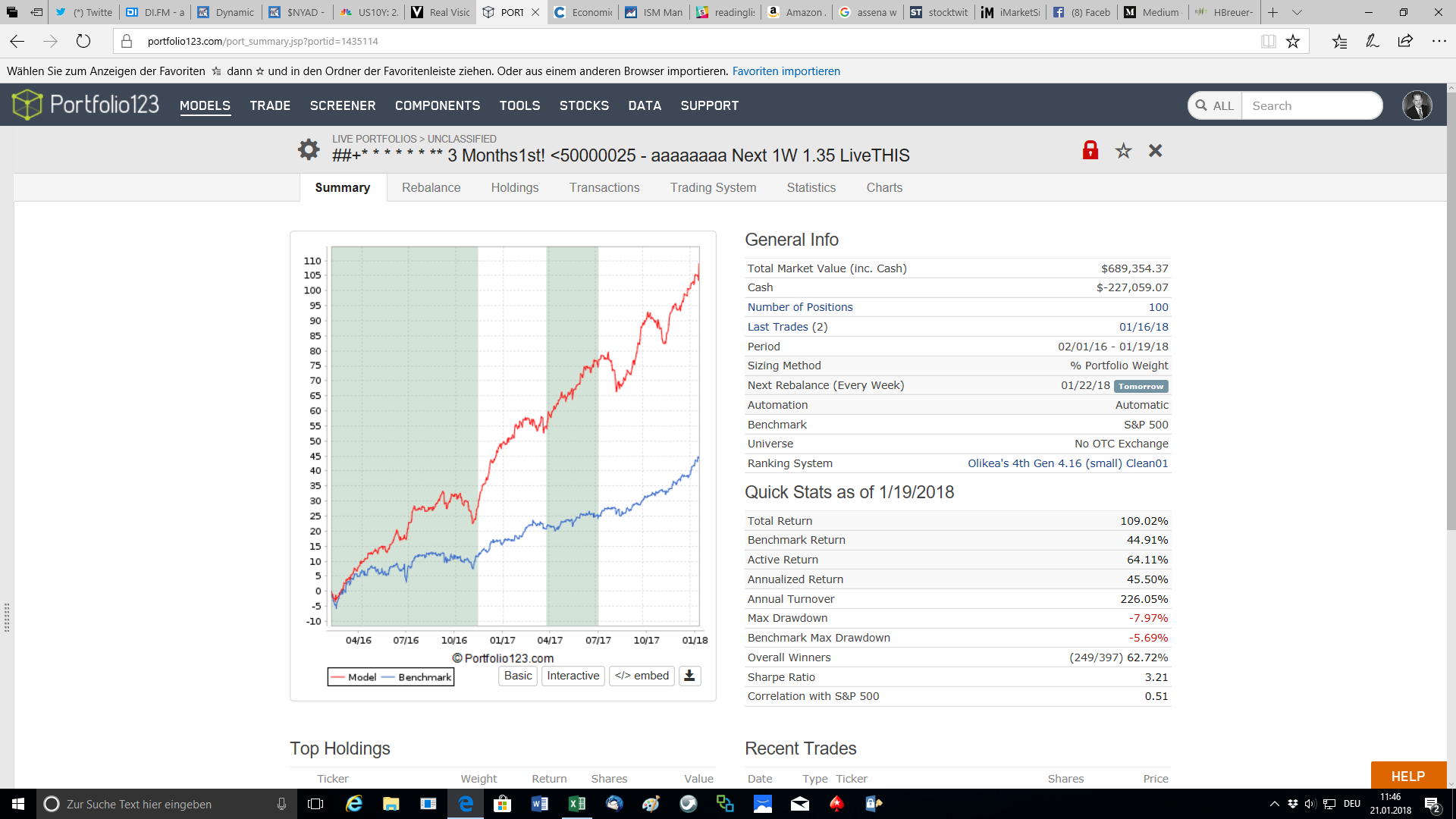

My model above is rebalanced and reconstituted every 4 weeks and shows only 505 trades. If this model is only rebalanced and reconstituted every 8 weeks, then annualized return = 26%, not much different to the 28% of the 4 week rebalanced model . This would indicate that the model is fairly robust, and does not depend on accurate signal execution.

That approach seems to make sense. A complex smooth function is more likely to be robust than a simple convoluted one. As you say, “keep it complicated”. Or as in the PEP 20 : “Simple is better than complex; Complex is better than complicated.”

Without getting too much into detail, I was hoping you might share your general thoughts on system(s):

Thanks!

//dpa

I didn’t mean to stir this much trouble. I just found it odd that the same (sensical) value factors did well up to a point mid 2014 where as if a switch was turned on and it no longer had any merit. For the record, none of them are PE or P2B based.

I appreciate that there’s alpha erosion but why would a collection of well-meaning factors cause a negative alpha? Tortoriello in his book graphed individual factors and noticed good alpha with a number of them. If the market is “catching on to it” I’d expect a flat market return, rather than a negative return…Unless my assumption is inherently wrong.

When I plot a histogram it shows a choppy, uninterpretable pattern which tells me there’s a disconnect; it has no bearing on returns in any way. What I gather from that is that people are not looking for value but are valuing other things in a stock.

I wonder if I’ll ever stop enjoying trading . . . The effort is a big part of the reward for me.

Usually around 40 or 45. I create a variety of ranking systems whose weights are all in increments of 2.5% (i.e. some are 2.5%, some are 5%, some are 7.5%, and some are 10%). My actual working ranking system is an average of the ones that work best in different time periods, with different numbers of stocks, and judged according to different criteria.

I have a lot of conditional rules to account for stocks with no analysts, financial sector stocks, and ADR’s. But those don’t really deal with factor interaction.

None of my models have 20X turnover. The one I work with has 6.5X turnover. I couldn’t deal with 20X turnover–no way. I like to trade, but I also really like to hold. The thing I hate most about my system is when a factor suddenly goes N/A, lowering a stock’s rank dramatically, and I have to decide whether to sell or hold it. That happened with LXFR when all its shares converted from ADRs to shares on the NYSE. All of a sudden SharesFDQ went N/A, messing up a huge number of my factors, and that field has been N/A for six weeks now, even though I know that the number of shares hasn’t changed at all. So I’ve decided to just hold onto LXFR until its next earnings report in March, when (fingers crossed) that’ll finally be fixed. To answer your question, I’ve decided to stay away from super high-churn factors like short-term mean reversion. Even P123’s basic sentiment system, which I use a lot, is a bit high-churn for my tastes.

You haven’t given us enough detail to explain this. How many stocks were in your system? What were those stocks (i.e. large caps, small caps, nanocaps)? How many factors were you using, and what were they? There could be a very logical explanation for your results that has nothing to do with “market catching on to” a factor or “people not looking for value.”

Thanks, Yuval. That’s a lot of good stuff to be thinking about.

I must’ve misread the 20x turnover. My apologies.

That is up with value ![]() Just had a monster trade with ford, up 200% on Friday, so I thought I sell it intraday (Its on the sell list for monday ayway because of a sell rule that sells everything with high liqudity

Just had a monster trade with ford, up 200% on Friday, so I thought I sell it intraday (Its on the sell list for monday ayway because of a sell rule that sells everything with high liqudity ![]()

Dear Kumar, please look up the secret sauce thread here I posted some stuff on how I do it.

The thing is, I can not make a r2g portfolio out of it, because R2G Portfolios calculate slippage in a way that it would destroy (theoretical) the performance of the model. I calculate with 0.3% slippage on very illiquid stocks in my backtests and my real time portfolios, because I am able to replicate that kind of slippage in real terms since 2013.

a 5 Stock model going sideways a year is totally normal, because it rolls the dice much less then a 100 Stock model. Interesting enough that

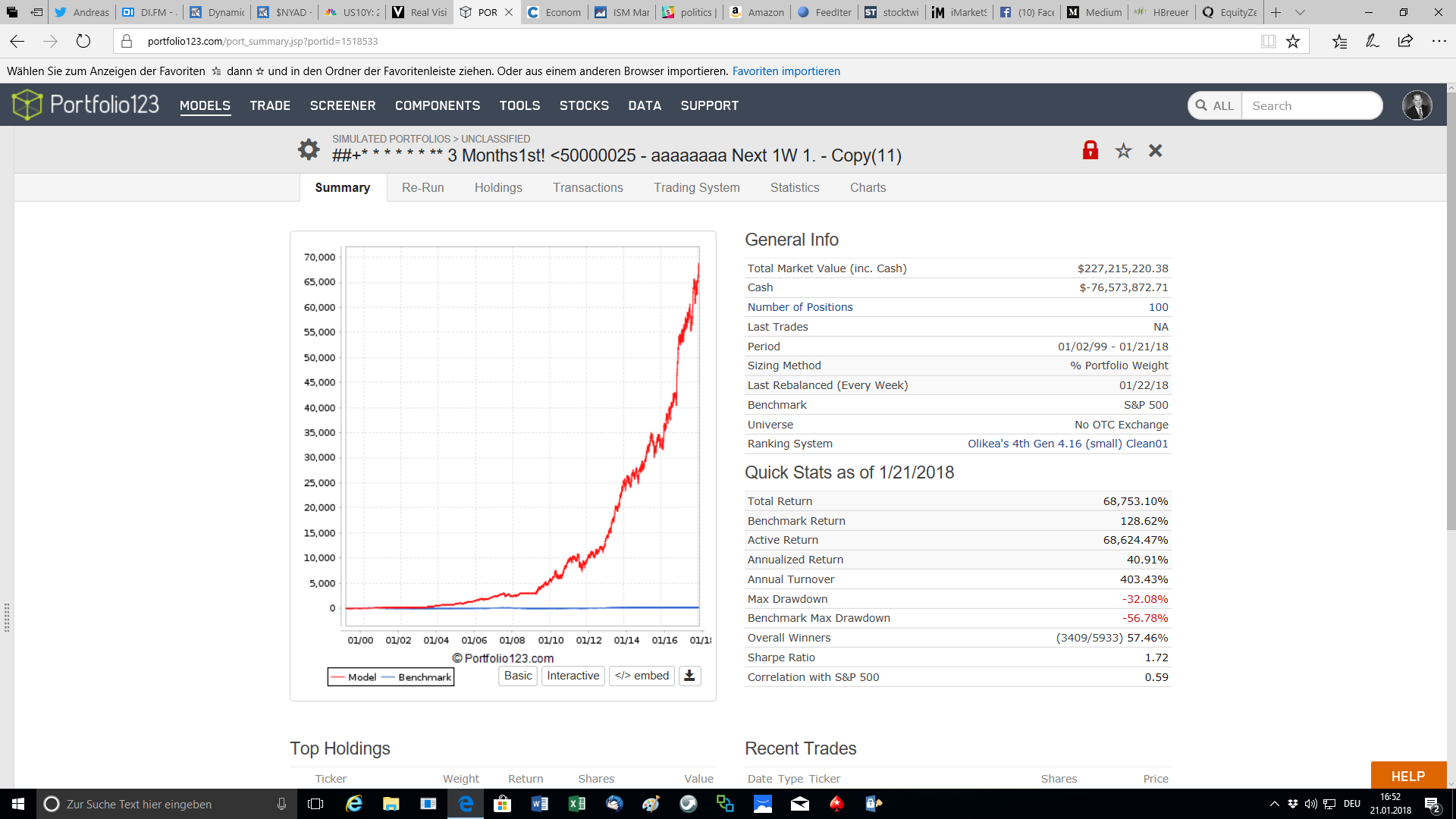

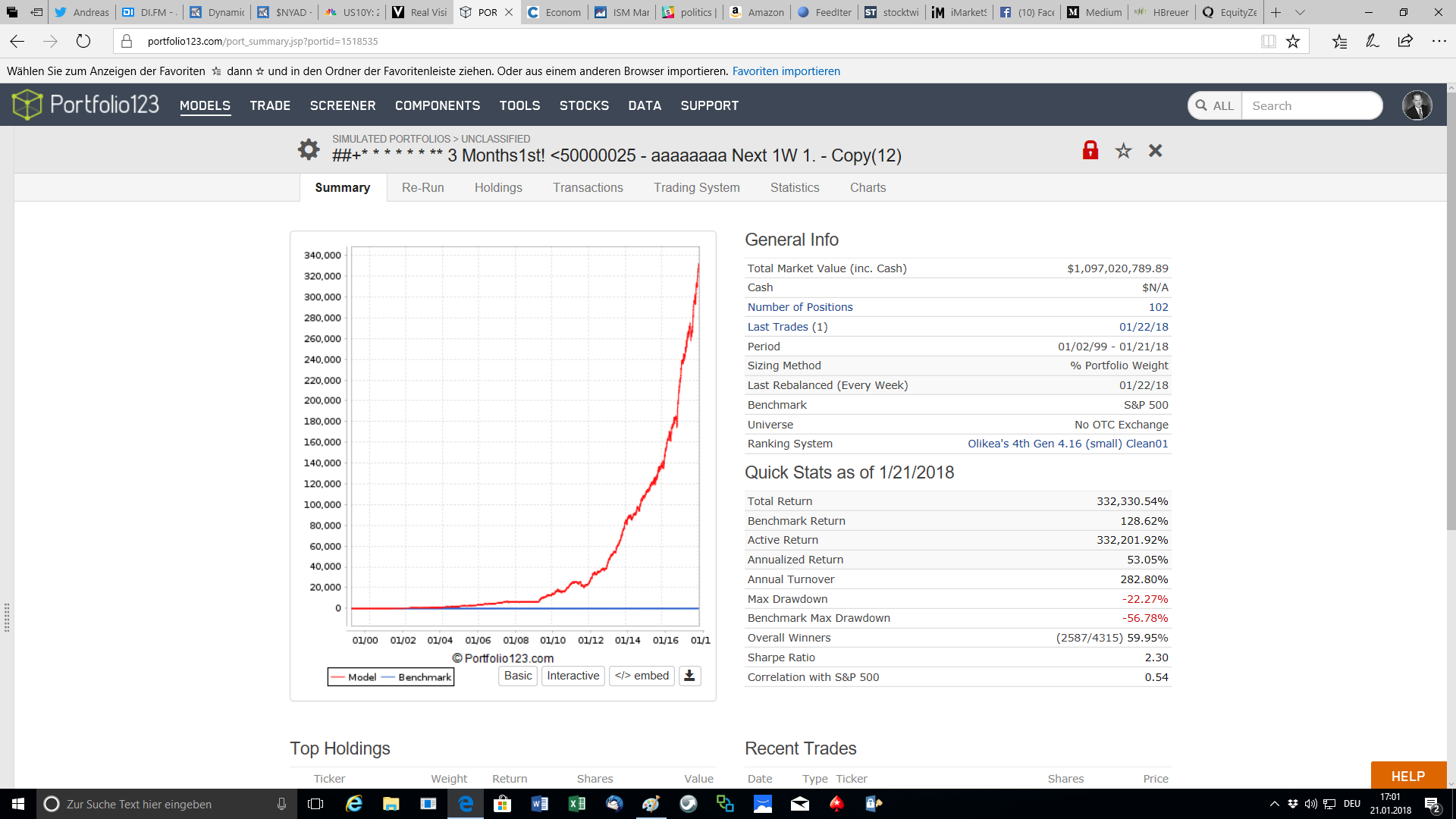

my Modell with 100 small cap stocks https://www.portfolio123.com/app/r2g/summary?id=1062281 is doing pretty good

A got a nice SP500 Value based Modell coming, 18% per year and a very, very nice capital curve, which I will trade when my port is

to big to chase those small caps

I got another very interesting Modell with 33 Stocks that I would be willing to sell privatly, but the price would be way higher then a normal r2g model so I will not go through this channel but find it through my private network.

If a Modell is not psychologically hard to trade (like trading small caps or encountering DDs) and if you do not overcome this, you

will not beat the market

on the timing side watch the movies of @CiovaccoCapital and read oshaugenny, https://app.hedgeye.com/ (macro show!) will also be a good source of timing the market, also earnings trend (fed Modell of p123) are a good watch to see where we are…

In summary:

Value is 100% the way to go, combine it with a bit quality and momentum and small caps and some knowledge on how to trade small caps

and avoid slippage then you got your system. The rest (90%) of the game is your mind, it took me 21 Years to learn this…

Best Regards

Andreas

if you want to learn how to trade with minimal slippage here is a good start: https://twitter.com/chuck_fulkerson

Andreas, just curious if you would be willing to post a SIM of your main system with the liquidity being avgdailytot(60)>500,000. It seems like low liquidity is the main driver of your results. Is this true? Thanks for all the openness on your system!

Yes, low liquidity micro caps is one of the main driver…, also it is levaraged with 35% this one is with 20 days average and > 500k a day…

and here the one I am trading with 20 day volume average of 25k, yes 25k. the main point is, with a port of below 1 Mil. and 100 or 200 Positions this can be replicated by using gtc trade orders, it sounds crazy but so far I was able to do it… (2013, 2014, 2016, 2017)

Very interesting. One more request. Would you mind posting those with no leverage and no timing? Again thanks for all the great posts.