One more thing. In Yardeni’s pdf, the squigly lines over the CNY series are not our CurrY & NextY. They are estimates for the specific year. That is also the correct way to do it. I don’t think they are worth the trouble to re-create since the CNY is enough IMHO

So you have changed the data in the CNY series?

Hugh

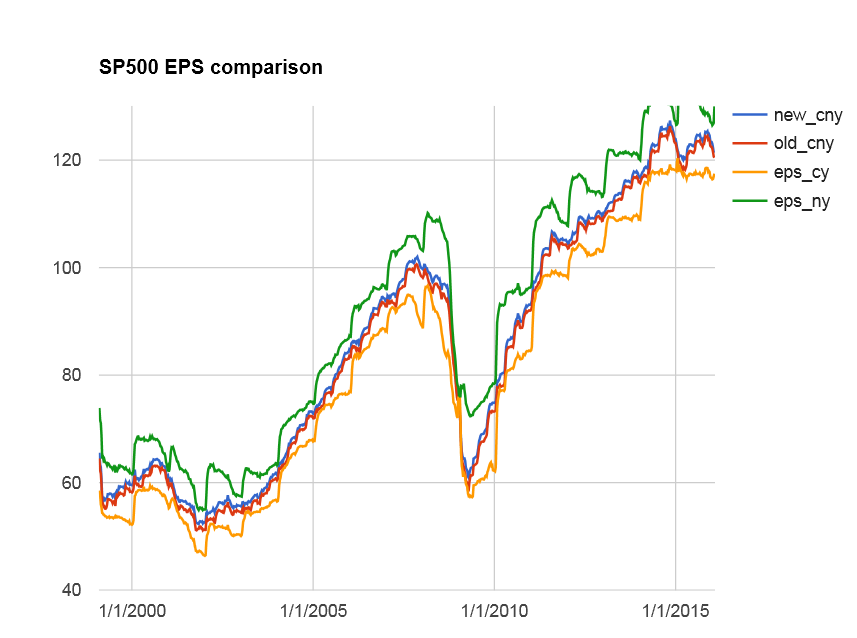

No the CNY has not changed. You can see the new one below or in this google drive spreadsheet:

As you can see the CNY is in between the CY & NY , as it should be , and the new one seems a bit smoother. Probably not enough to justify changing it. Using quarter # to slot in the CY is a perfectly valid way to do it (Compustat does it with Q#).

I agree that the end and beginning of year SPEPSCY data is unreliable.

I mention this in this viewthread: http://www.portfolio123.com/mvnforum/viewthread_thread,9380_lastpage,yes#lastpost

Also there is a blatant error in Feb-2010. In Jan-2010 SPEPSCY jumped from 62 to 75 within one month. See also chart below where the spike is shown.

Estimate data is very spotty before 2000. Reuters was the same.

The SPEPSCY jump in 2010 is legit. It’s simply CY switching from 2009 to 2010 . This is precisely why CNY should be used instead.

Make sure you exclude berkshire with: UnivExclude(“BRK.B”)

We have not been able to resolve the issues with berkshire switching “primary” stock from A to B on the Compustat side while CapIq maintained A as the “primary” issue.

ok, thank you!!!

Hi, Marco:

Is it possible to show us a sample #SPEPSCNY in “Custom Series” so we can adjust it if necessary? For example, I want to see some sector-specific EPSCNY.

Thanks a lot.

Hengfu

Marco,

The Feb-2010 spike was due to berkshire.

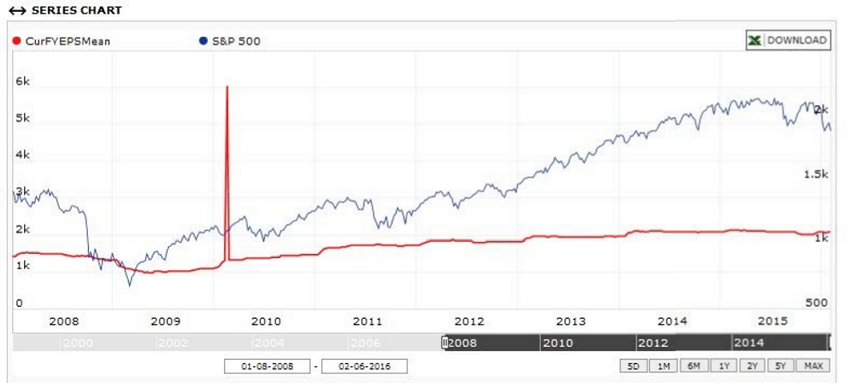

But please explain how P123 calculated the last value (2/6/2016) of EPS CurrY = 118.13975 in the FedModel.

That would be the with the Friday 2/5/2016 data.

I one uses the custom series MySPEPSCY to calculate this value then it becomes 113.84. There is a huge difference here.

For the previous 4 weeks the difference between the FedModel data and the custom series values was much less.

Thanks.

A good place to start is here: https://www.portfolio123.com/app/series/summary/37?st=1&mt=8

I have created custom series for blended, sector specific estimates. Very helpful to understand relativ sector strength / weakness.

Thanks, but your example is using CurFYEPSMean.

I am looking for the BlendCNY item to construct #SPEPSCNY specified in

https://www.portfolio123.com/doc/doc_detail.jsp?factor=%23SPEPSCNY&popUpFullDesc=1

#SPEPSCNY: Calculated using a blend of the Current and Next Year estimates for the S&P500 stocks. The weight given to the CurrY and Next Y depends on which quarter was the most recent. For each SP500 stocks the following is calculated:

BlendCNY = if Q4 then (CurFYEPSMean)

if Q1 then 75% (CurFYEPSMean) + 25% (NextFYEPSMean)

if Q2 then 50% (CurFYEPSMean) + 50% (NextFYEPSMean)

if Q3 then 25% (CurFYEPSMean) + 75% (NextFYEPSMean)

The SP500 Blended EPS is then computed as

num = Sum { BlendCNY (i) * Shares (i) }

den = Sum { MktCap (i) }

#SPEPSNY = ( S&P500 Close * (num/dem) )

Geov, 113.84 is coming from you clicking “Totals” right ? There’s a issue with clicking “Totals” on a Monday. It’s uses the benchmark last date available to set the “as-of-date” for the estimates, but that’s a Friday, so it’s missing this weekend data. The backtest, or time series generation, is correct though.

Long story short… we’ll investigate “Totals” so that it’s not confusing. It was always meant to be just a way to spot check data.

Marco, Thanks a lot for this explanation, very much appreciated. I noticed that the graph showed the higher value at the end, in line with the FedModel data.

As I said above, my link is a good point to start, not the final solution. Just use “month” and “eval” for quarter-specific blends.

.

Not sure how P123’s SPEPSCNY is computed or if it is computed correctly.

Since P123’s EPSCurrY and EPSNextY are both going up right now, why do we have falling SPEPSCNY? See attached chart.

As Cyberjoe suggested, here my version of SPEPSCNY:

https://www.portfolio123.com/app/series/summary/4075?st=0&mt=8

The EPS Blend CNY I got:

1/2/2016 119.2668457

1/9/2016 118.943634

1/16/2016 119.048645

1/23/2016 119.4662094

1/30/2016 120.8971024

2/6/2016 121.7691879

My SPEPSCNY is going up. Anything wrong in my formula? Any idea?

CNY represent “the year ahead”. It is falling now because more & more companies are reporting Q4, which results in 1/4 of NextY being dropped off, and more & more CNY being the same as CurrY. Since NextY is usually bigger than CurrY , during the first few month of the year when most companies fiscal year ends, CNY moves towards Curry resulting in a decline. A real decline, not artificial.

Marco, I know you have gotten beaten up about this. But I wanted to say thank you for being open on your inputs and rational on this topic. It made me rethink a timing strategy I have that was using CY and I have redone it completely using CNY. My overall strategy got better because of this re-think.

Since the Jan and Feb values of SPEPCY are unreliable, one should not use those values in a model, especially when there is a down-market present. I got good results with SPEPCY in timer models when restricting the model from going long during the period Jan-Feb while down-markets exist, indicated by sma(50,0,#bench) < sma(220,0,#bench).

I think I understand the reason behind SPEPSCNY, but when I tried to calculate it using the formula:

SetVar(@q1num, @EPSAdj * UnivSum(“1”, “0.75*(CurFYEPSMean * SharesQ) + 0.25*(NextFYEPSMean * SharesQ)”))

It is different from series SPEPSCNY, and SPEPSCNY data seems to be wrong.

Just hope SPEPSCNY calculation won’t get revised later after people build strategies around it.

Great idea. Thanks.

Hengfu, please see my https://www.portfolio12.com/mvnforum/viewthread_thread,9514_lastpage,yes#lastpost

And, yes, there will be a slight revision to #SPEPSCNY but it should not be significant as I explained in the post.

Thanks