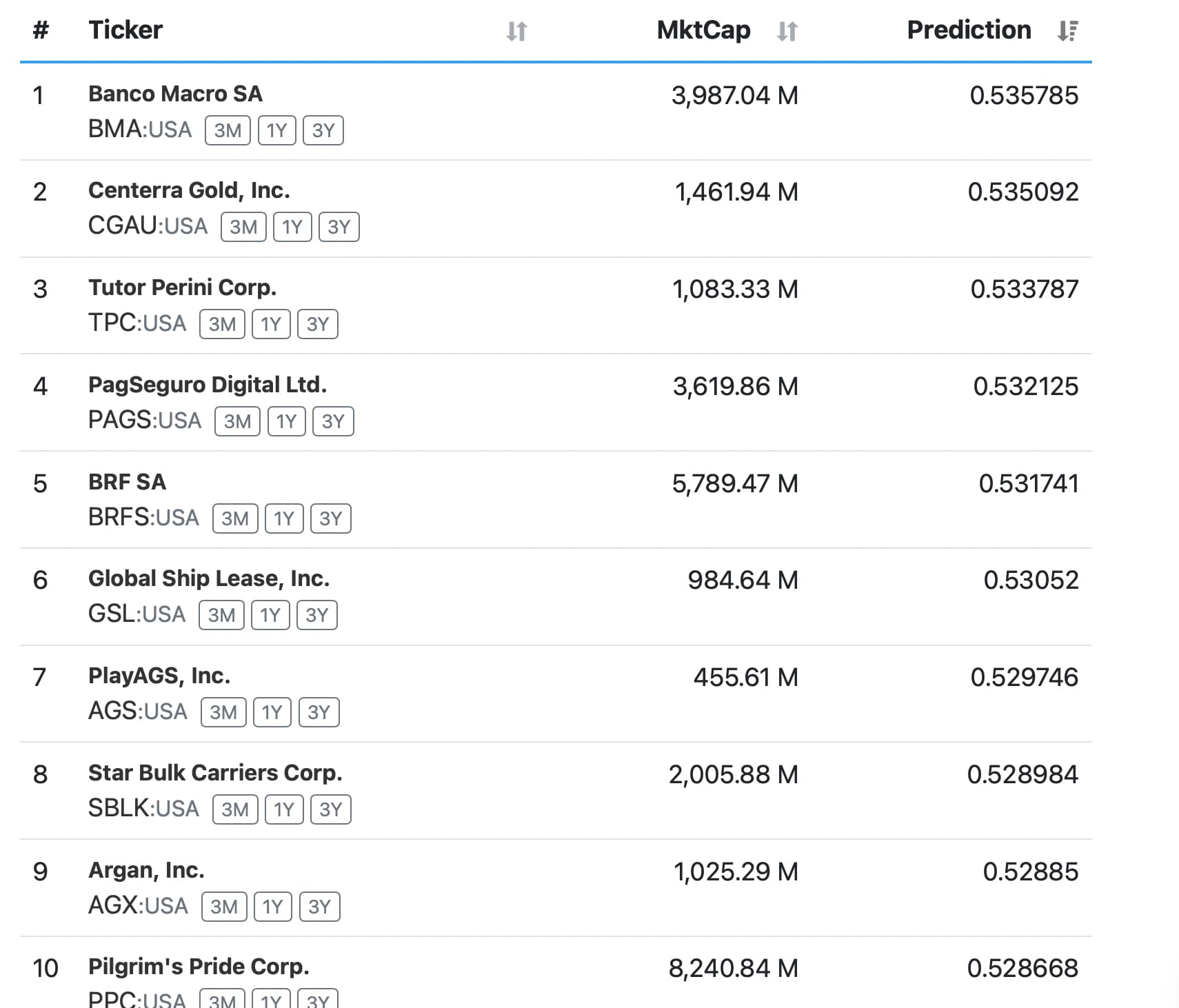

Okay, so we have predictions of returns now, and we can all consider how we might use this information. Example here:

So now, one might go to P123's screener, enter these tickers and use a ShowVar formula to calculate the trading costs for each ticker. You could enter a sophisticated formula to your liking there.

Then you would subtract the slippage calculation from the predicted return. Using zero slippage if you already hold the asset. Re-sort after subtracting slippage and form a new rank. This is a ranking of your true expected return for each stock over the rebalance period.

Assuming you are going to be relying on the AI's predicted returns to create a rank when you sign up for P123's AI/ML anyway, and that the you have a good formula for slippage, then this is clearly a better ranking system.

And easier to rebalance. If you have a 15 stock port you would always hold the 15 stocks with the highest rank when cthe ranks are calculated this way. Think about that and I think you will agree. Because you have set the transaction costs for a stock you are holding to 0 you would only be selling it and buying a hew stock if he new one had greater expected returns (including the transaction costs). I.e., for a 15 stock portfolio and this ranking system you could always set a sell rule of RankPos > 15. If your predictions of returns and slippage are good you would not even need a sim as a screener with this data would predict your returns.

I also note that rebalancing a port could all be done on just the new AI/ML server at each rebalance. Perhaps saving someone (P123 and/or a member) additional costs of moving that data to another server for rebalance. And this is just a better ranking method anyway

Or you can do it yourself using InList. I.e., Sell rule: Ticker ("Insist") = False. Buy rule: Ticker ("Insist") = True..

Jim