All,

Here is an article by Pimco that shows how every risk-control method you have (probably) ever heard of can be connected to the other methods: An Asset Allocation Primer: Connecting Markowitz, Kelly and Risk Parity

Jim

All,

Here is an article by Pimco that shows how every risk-control method you have (probably) ever heard of can be connected to the other methods: An Asset Allocation Primer: Connecting Markowitz, Kelly and Risk Parity

Jim

This is a great article if you have a sophisticated understanding of the various allocation models. Do you know of an article or book that gives a very basic understanding of all these various approaches? This is like a Part Two, and I need a Part One that explains how each one works.

Personally, I would love to be able to implement a Kelly approach to portfolio optimization, but the only way I know to use a Kelly approach is to balance one risky asset with a non-risky one. What if you have twenty risky assets, and some are riskier than others? Everything I’ve read about multiple Kelly is beyond me.

Hi Yuval,

I hope you will soon believe me when I say you already know all you need to know for the most part. Perhaps an outline will help convince you of this.

I. What I am sure you already know about discrete bets.

You can refresh your memory here. I will not expand as I have already seen your post on this in the past: Kelly criterion

II. Optimal bet size for coninuous returns (like a stock or ETF).

Optimal bet size = (μ - r)/σ^2

μ = mean return

r = risk free rate

σ = standard deviation.

That is it.

Of course, one can write this as Sharpe ratio/Standard deviation. You already know this formula. You can get this from the metrics of your sim or port. Just make sure of your units, annualization etc.

Or you could get a starting point for the Sharpe ratio for multiple assets from P123’s Books and adjust the leverage of the portfolio as a whole which is a practical answer to your main question, I think.

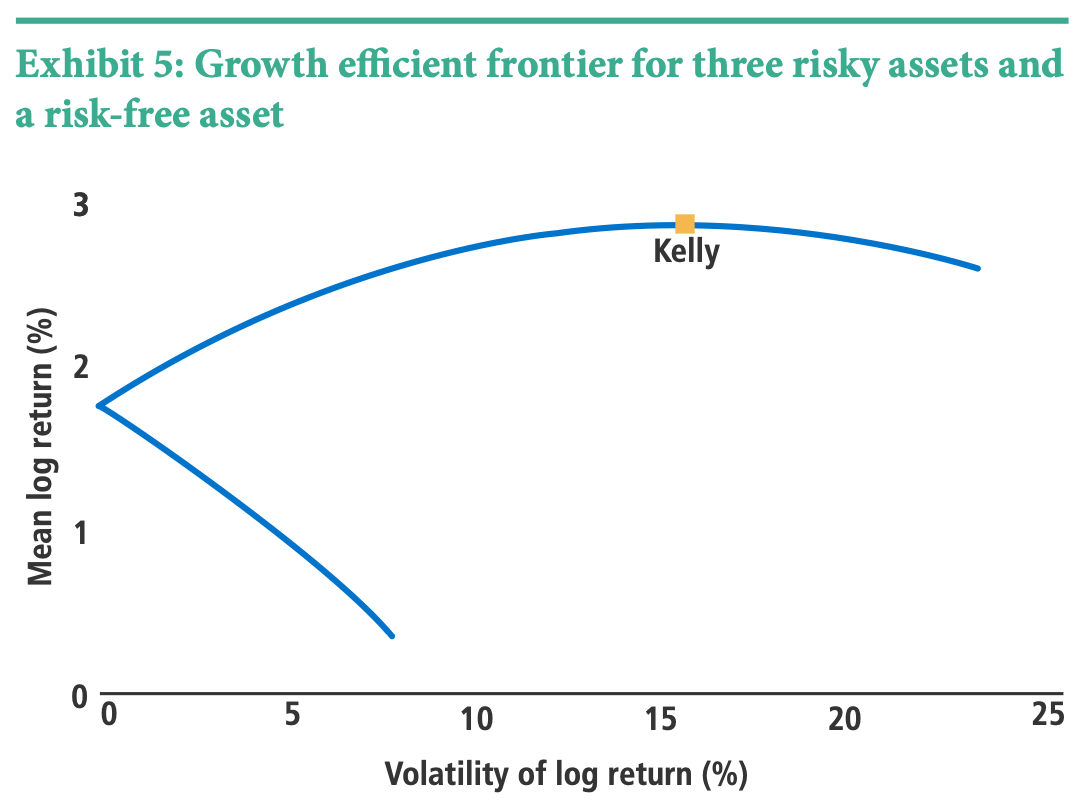

Radical? Yes if Pimco is radical (first image). Notice γ is set to 1 to be the Kelly Criterion but one can use other numbers.

Also note that as per Pimco this is the “instantaneous Sharp ratio.” I take that to mean one might update this based on the expect volatility (and returns) as the market changes from day to day.

III. What to do? One possible method

So one can get a first estimate of theSharpe ratio (from books say) or even optimize a first estimate of the Sharpe ratio with mean variance optimization.

Note, I do not advocate using historical data (from sims or books for example) alone for means variance optimization. In fact, I strongly recommend against this. But one can use whatever method one prefers to get an expected Sharpe ratio for your portfolio going forward. Once one has something they personally are comfortable with then simply divide by the expected standard deviation to get the optimal bet size.

IV. The most important thing: Never bet more than what the optimal Kelly will be out-of-sample.

This means be right about every step above (or allow for error) . Full stop (the most important thing). Needless to say there may be some art to this or a person may benefit from some experience.

For support on the problems with overbetting (or too much risk) just look at this graphic in the Pimco article (Image 2).

With this outline you can go to step 3 on your own. I am pretty sure the Pimco article will make more sense the next time through as a start. Wikipedia will have some of what you might want. I am sure the many on the forum can help with any questions.

Thank you for your interest.

Jim

Jim,

Thank you for your link and the detailed explanation.

As a frequent user of Kelly Criteria, I did learnt something new from the PIMCO paper.

Regards

James

I found this paper somewhat useful too, though I don’t understand it all:

As far as books one can look at this: Kelly Capital Growth Investment Criterion, The: Theory And Practice

It is pretty dense mathematically but not quite as bad as the above paper that Yuval references. And it does cover additional ideas such as adjusting strategies as you approach your goal (e.g., retirement goal). The book is affordable for those who are truly interested.

But for those just wanting to start using the Kelly criterion going to Wikipedia and finding this formula along with the rest of the Wikipedia article should do it. The practical portions of the Wikipedia article are probably accessible: Kelly criterion

Optimal bet size = (μ - r)/σ^2

μ = mean return

r = risk free rate

σ = standard deviation.

That is all you really need. Annualize everything I think (but check me on that and post what you find, please). Maybe adjust your position (using the equations) as volatility changes in the market. Maybe use the annualized volatility of your port for the last 3 months. You could also experiment with expected volatility.

[color=firebrick]Assumptions about future returns give the greatest error when trying to do something like this!!! Something that could sting and leave a mark (on your portfolio) if there is a market regime change.[/color]

Risk parity or a minimum variance portfolio reduces the number of assumptions you are making but you could still run the risk parity (or minimum variance) portfolio through Books or Portfolio Visualizer to get a Sharpe Ratio and the standard deviation for a portfolio to get a maximum amount for your leverage (and back off from that).

There is nothing about this stopping you from using discretion when selecting the strategies in the portfolio or how much you back off from the calculated “optimal Kelly fraction.” [color=firebrick]The only thing not optional is avoiding making too large of a bet. Pimco (and Kelly) would agree with me on this.[/color]

I’m afraid I fail to see the connection between the Kelly criteria and the standard deviation.

Let’s take a simple case. An asset has a 50% chance of gaining 270% and a 50% chance of losing 70%. The risk-free asset remains constant.

The Kelly criteria says that you should put 0.5/0.7-0.5/2.7 into this asset, which comes to 53% of your portfolio.

But (μ - r)/σ^2 = 17% or 35% depending on whether you use the sample or the population standard deviation.

Yuval,

Right. So as long as this discussion is about the Kelly Criterion, I don’t think I can invent a better (or simpler) formula for continuous returns other than (μ - r)/σ^2. I apologize for that. Pimco, Wikipedia, the book referenced above and many other references were enough to persuade me to put it into this thread (and not edit it out now).

BTW, the above book that I referenced is edited by Edward Thorp who made a bunch of money using the Kelly Criterion and popularized it in in the 1960’s (it has been around for a while). He does not have too shabby of a record as a hedge fund manager either. I am more inclined to think he (and all of the works he edited) might be right about the Kelly criterion than spend a lot of time trying to prove that he is wrong. I think you can find all the proofs of the validity of the formula you might want in the book I referenced (including Kelly’s original proof in the 1950’s) if you are truly interested in learning about that. I am not sure how much that can be simplified and I won’t attempt a new, simpler proof or copy and paste an existing proof into this post.

This is not a new topic and we do not have to reinvent the wheel here at P123, I think. Fortune’s Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall Street might be a good first book for any member interested in the general topic.

As for the question of which standard deviation, I think you are probably doing it wrong to get that much of a difference. The n or the n-1 in the denominator has nothing to do with the number of holdings, BTW. But I am not sure what you are doing.

Anyway just use the sample standard deviation would be my simple answer to your question considering you are actually finding the standard deviation of a sample and will never have data on the entire population–unless you can show me a reference saying otherwise.

BTW, I am not recommending or using the Kelly Criterion myself except to the extent that it is actually “connected” to any professional strategy used almost everywhere–as supported by the Pimco article. I was just trying to answer your question.

Anyway, I wish you the best with whatever formula you end up using for determining what leverage amount has the appropriate amount of risk for you. And ultimately the method you arrive at might be better: your question was about the Kelly Criterion.

Best,

Jim