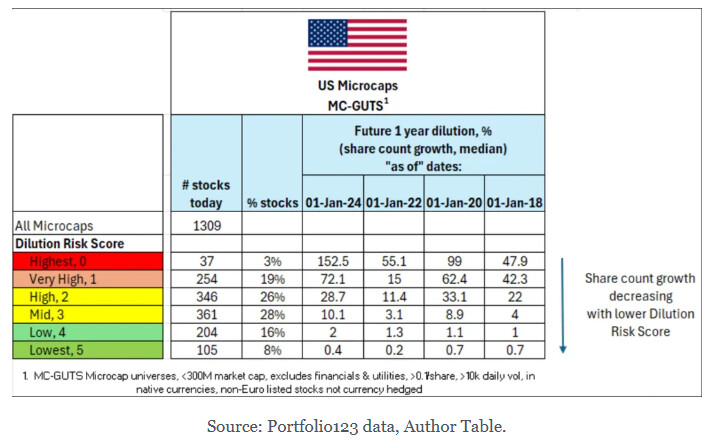

I tried to replicate A Dilution Risk Scorecard from @rtelford :

formula:

or this simpler one:

Works quite well especially for shorting (or filtering out) stocks.

Source:https://microcapclub.com/how-to-avoid-dilution-in-microcaps-a-dilution-risk-scorecard/

5 Likes

This is pretty close Piotr, a few minor differences, but it’s more or less it.

It does seem to work well to filter out a lot of junk, and stocks at higher risk of diluting.

https://microcapclub.com/how-to-avoid-dilution-in-microcaps-a-dilution-risk-scorecard/

Thanks for sharing the link with the forum!

Cheers,

Ryan

2 Likes

tr

January 21, 2026, 6:40pm

4

pitmaster:

Eval(((IsNA(SharesFDQ, SharesQ) - SharesQ) / Max(0.001, SharesQ)) < 0.05, 1, 0)

Thanks for your insights.

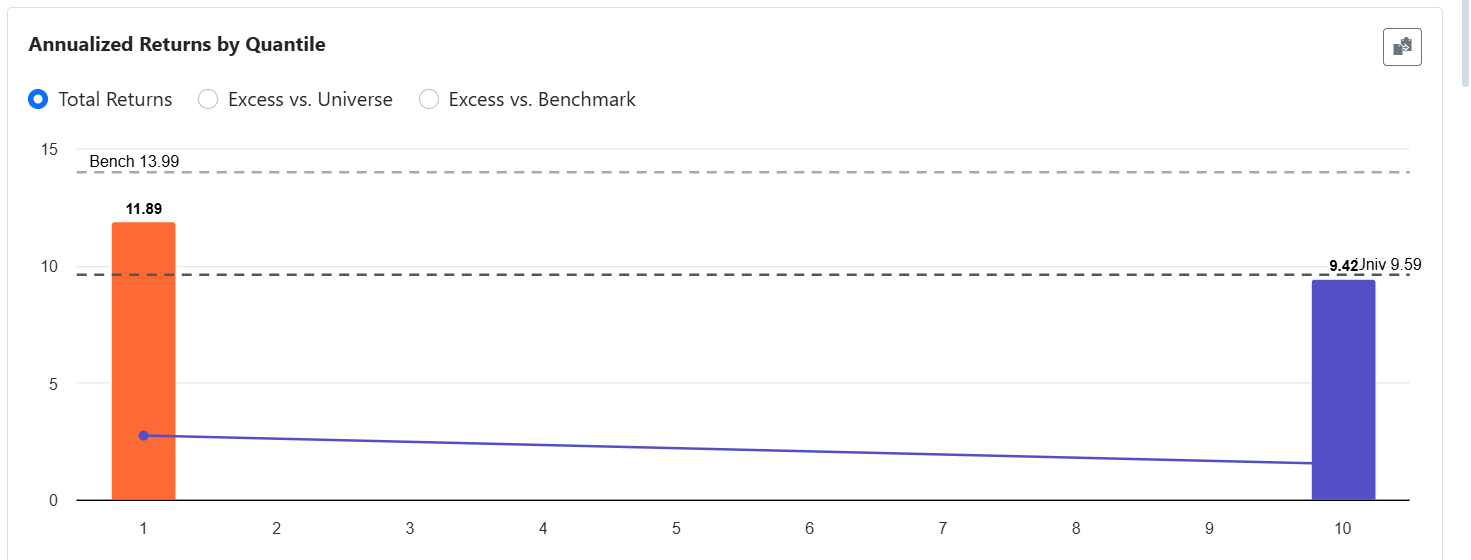

However when i apply this factor to ranking i get opposite results than what we expect on R3000 stocks (bucket 10 indicate factor =1, bucket 1 indicate factor =0). Can anyone replicate this result?

I used 5 buckets, R3000, and added tiny random noise to sort stocks with same score.

isna((OperCashFlTTM > 0) + (Eval(FCFTTM >= 0, 1, CashEquivQ / Abs(FCFTTM) > 1)) + (SharesQ / SharesPYQ < 1.03) + ((SharesFDQ - SharesQ) / SharesQ < 0.05) + (CurRatioQ > 1.5), 0) * (random/1000)

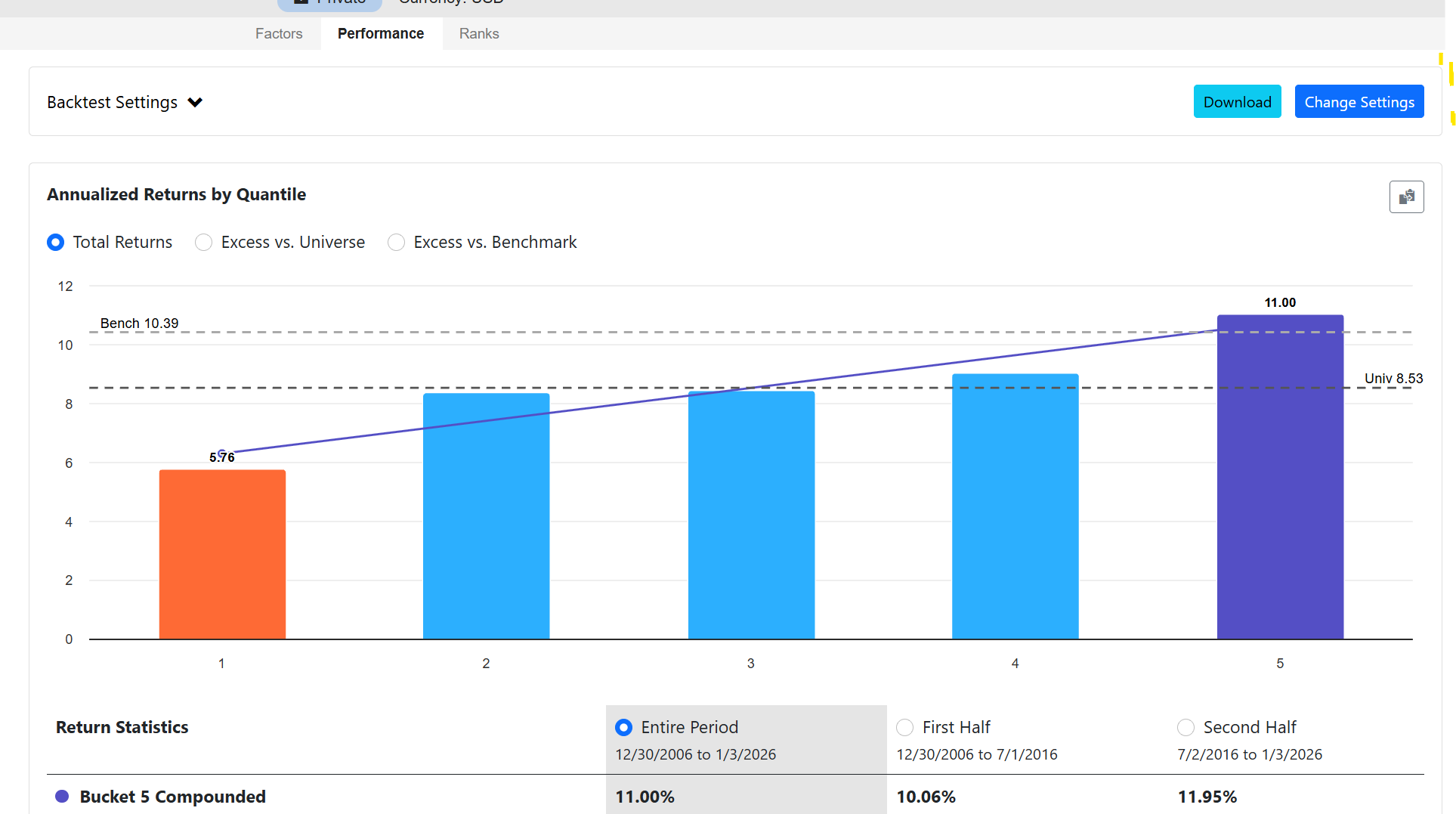

I'm not sure about the 'Cash Runway' factor (the second one). Maybe @rtelford or @yuvaltaylor will revise it.

3 Likes