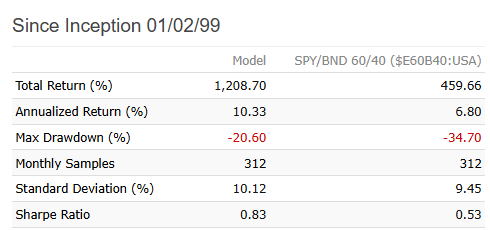

The model has hugely underperformed the R3000 since 2009. A total return of 420% versus 750%. What makes you think it's worth pursuing?

This model may be a good option for investors preferring 60% stocks / 40% other assets.

Based on my own calculation of historical allocation, a benchmark should something like 50/20/20/10 [defensive equity/ bonds/ gold/ commodities].

Volatility of this model is close to the 60% stocks / 40% bonds benchmark and outperformed the benchmark since inception and 2009.

As I said previously, it is not the perfect model, it is in fact very simple model... but you can see that p123 offer tremendous possibility in terms of developing asset allocation models.

Adding more bonds will bias the model towards selecting more bonds. TLT offers highest expected return. Did you get better risk-adjusted performance experimenting with different set of universes ?

1 Like

I have also experimented with asset allocation models within P123. It takes some time to figure things out, but with custom formulas and dynamic weighting you can basically build almost anything you want in the multi-asset space.

I think they can have a place. I mean even if you are a ‘stocks only’ person, you will probably want to diversify internationally at some point - how much do you allocate to US, how much to Europe? Do you hedge currency risk or not? Do you keep any ‘cash’ positions in US Dollars, in Euro or in gold? That’s an asset allocation question that ideally you formulate beforehand based on some idea of how you think the world works and you have tested beforehand.

If you are a retail investor that is retiring, an asset allocation strategy based on just ETFs could be an option. The returns will by far not be what you would get with individual stocks, but diversification (obviously) limits drawdowns significantly which has its place. Also, you could potentially replace the asset class of ‘US stocks’ within your asset allocation strategy by one of your multi factor ranking strategies for individual stocks, the same for Europe, REITs and potentially other equity markets. Lastly, if you have a really high amount capital to manage, a multi asset allocation approach can become relatively attractive, because the outperformance in stocks will be much harder - especially on a risk adjusted basis.

Having said that, I would always incorporate international equities in any asset allocation model, which most P123 models I see do not. If you don't, in my opinion, you will have an implicit survivorship bias in your model, because a lot of countries’ stock exchanges and/or currencies have gone to 0 historically by capital constraints, wars or inflation. The US has not. So only looking at that market would be incorporating a look ahead bias. Those are extreme examples of course, but that is the thing with asset allocation (or any quantitative approach), you want to make your model as robust as possible and think of things before they happen.

1 Like

I think it is possible to find an ETF strategy that has less drawdown than a classic 60/40 stock bond allocation and a better Sharpe Ratio. With similar returns. The SP 500 has done remarkably well recently however. So maybe lower returns on a recent backtest.

One can then add P123 small-cap strategies that diversify your portfolio into small-caps while taking on more risk with a higher return. Adjusting the risk to your personal tolerance for risk.

You can get as much risk as you want including going all P123 small-cap strategies with leverage if you want. Or all ETF strategies if you prefer. For me it is not one or the other.

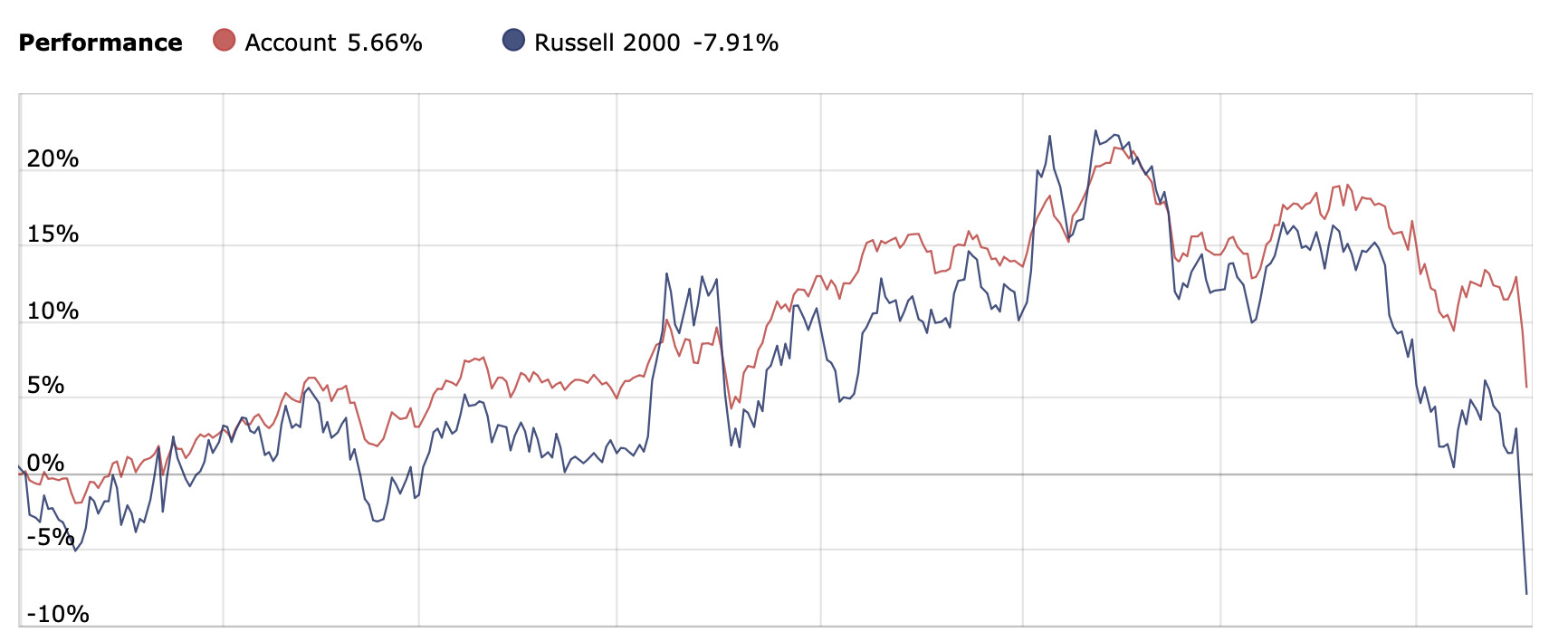

I think those near retirement can beat the Russell 2000 with considerably less risk with help from some of the ideas above. This is from 1/1/2024 to now using some of Pitmaster's ideas for a portion of the portfolio AND P123's generation of excess returns for the small-cap portion of the portfolio to be sure. An investor could consider allocating more to P123 strategies after we have reach the bottom and started a recovery—keeping some "dry-powder" and resisting the urge to capitulate:

By definition, asset allocation modeling is equivalent to futures modeling plus passive betas.

This area is not suitable for making money.

It is to mitigate risk in some occasions.

Edit: “the world works” is very counter-intuitive here, not like "how you think" or only some "tested beforehand". For example, high inflation and high unemployment are positively correlated with higher future stock returns.