Kelly Betting is best know for optimizing returns. But it can also be used to control risks.

The general formula for Kelly betting is edge/odds.

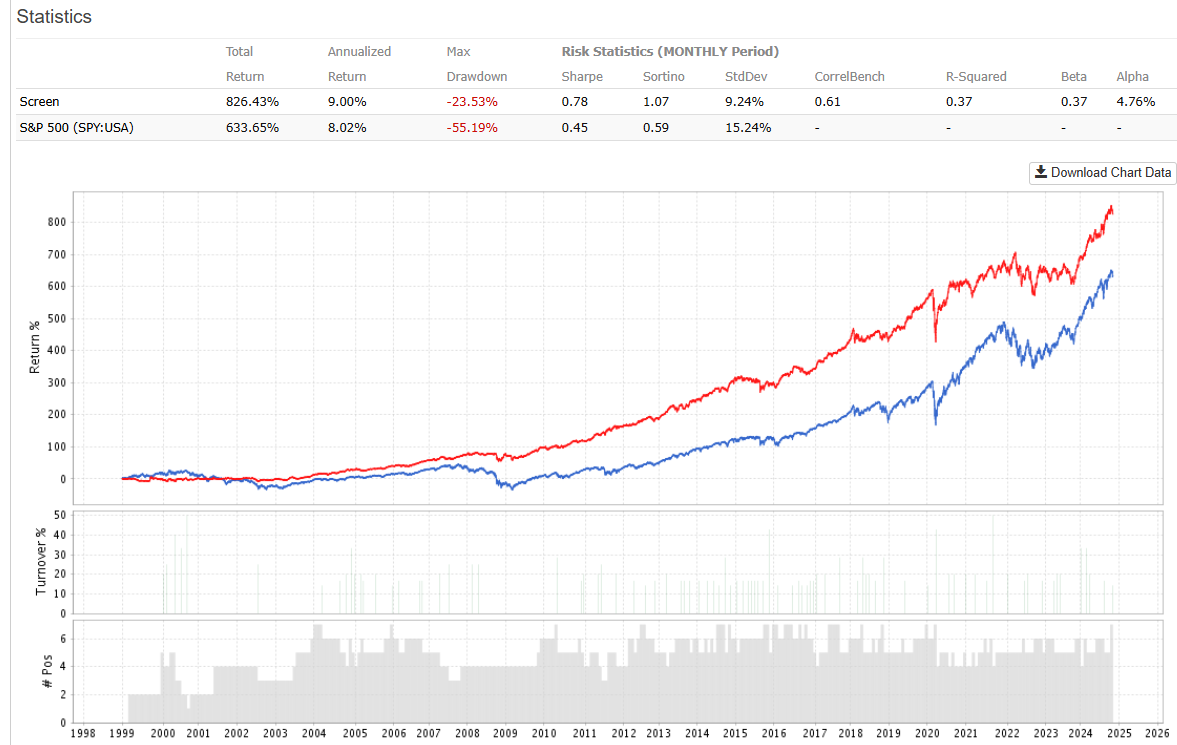

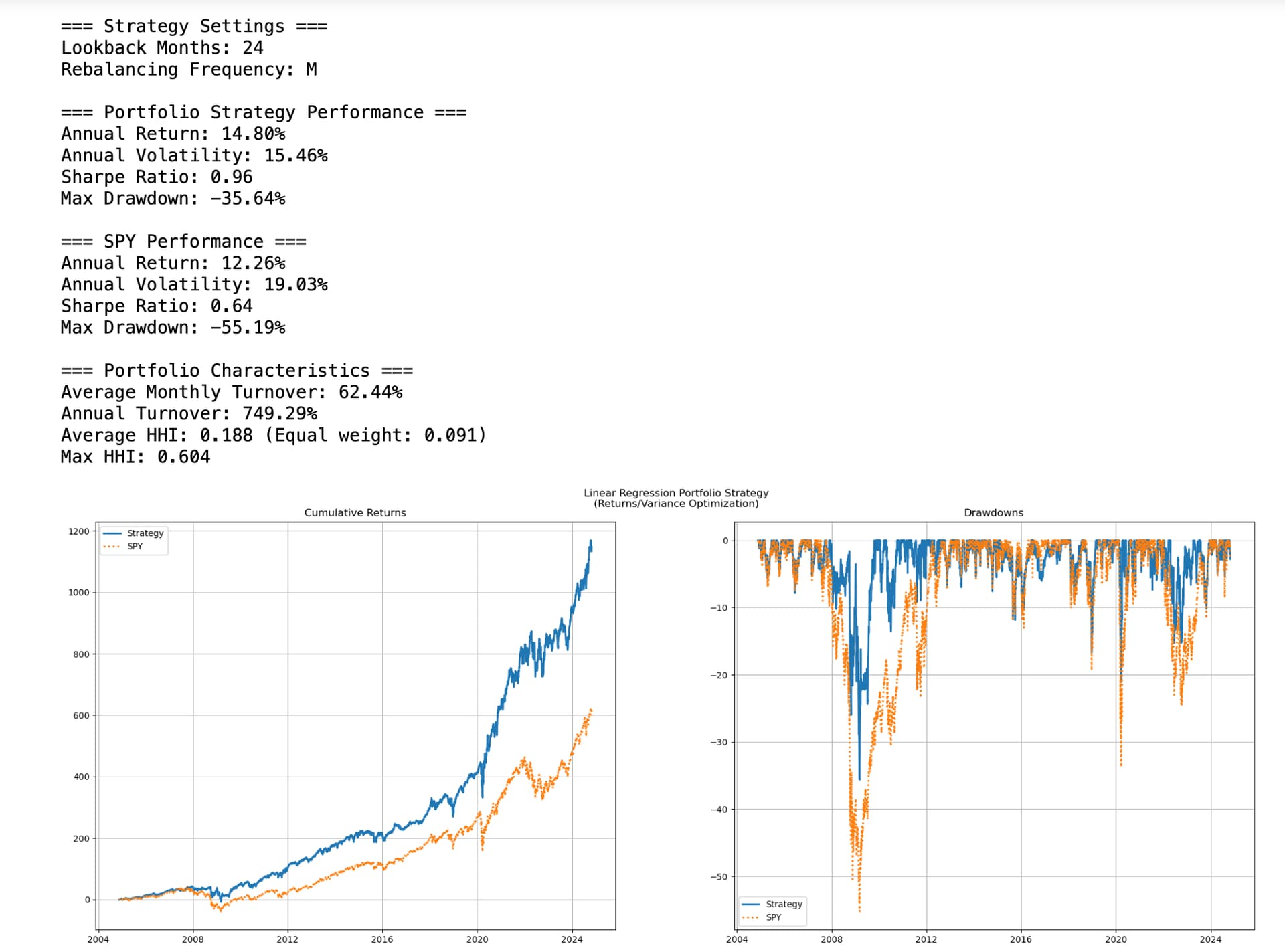

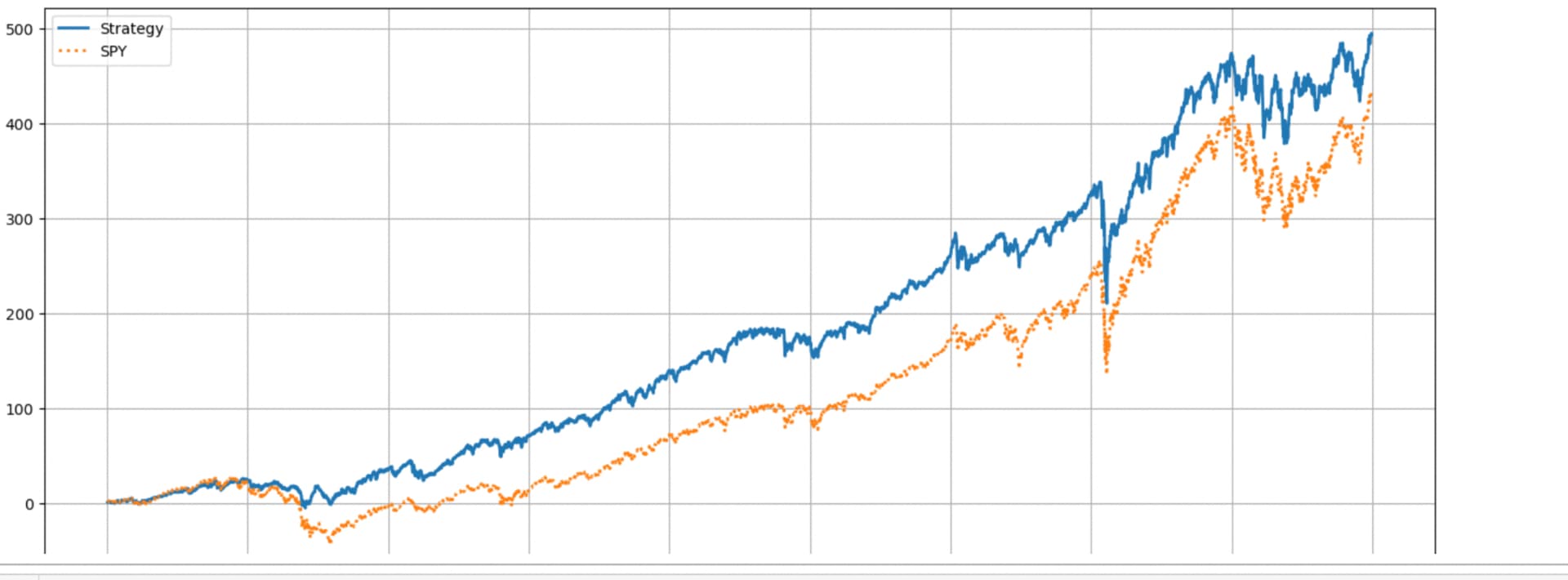

I used (Probability of beating SPY)/Variance for 10 ETFs (Nine SPDRS and TLT). with a sliding 60 trading day window, rebalancing monthly.

It did reduce risk (especially drawdown in 2008) with little loss in returns. Some could consider using some leverage to get closer to "Optimal Kelly."

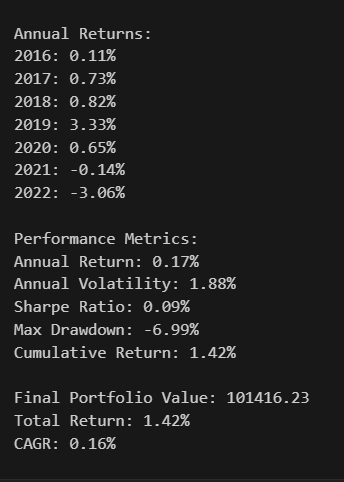

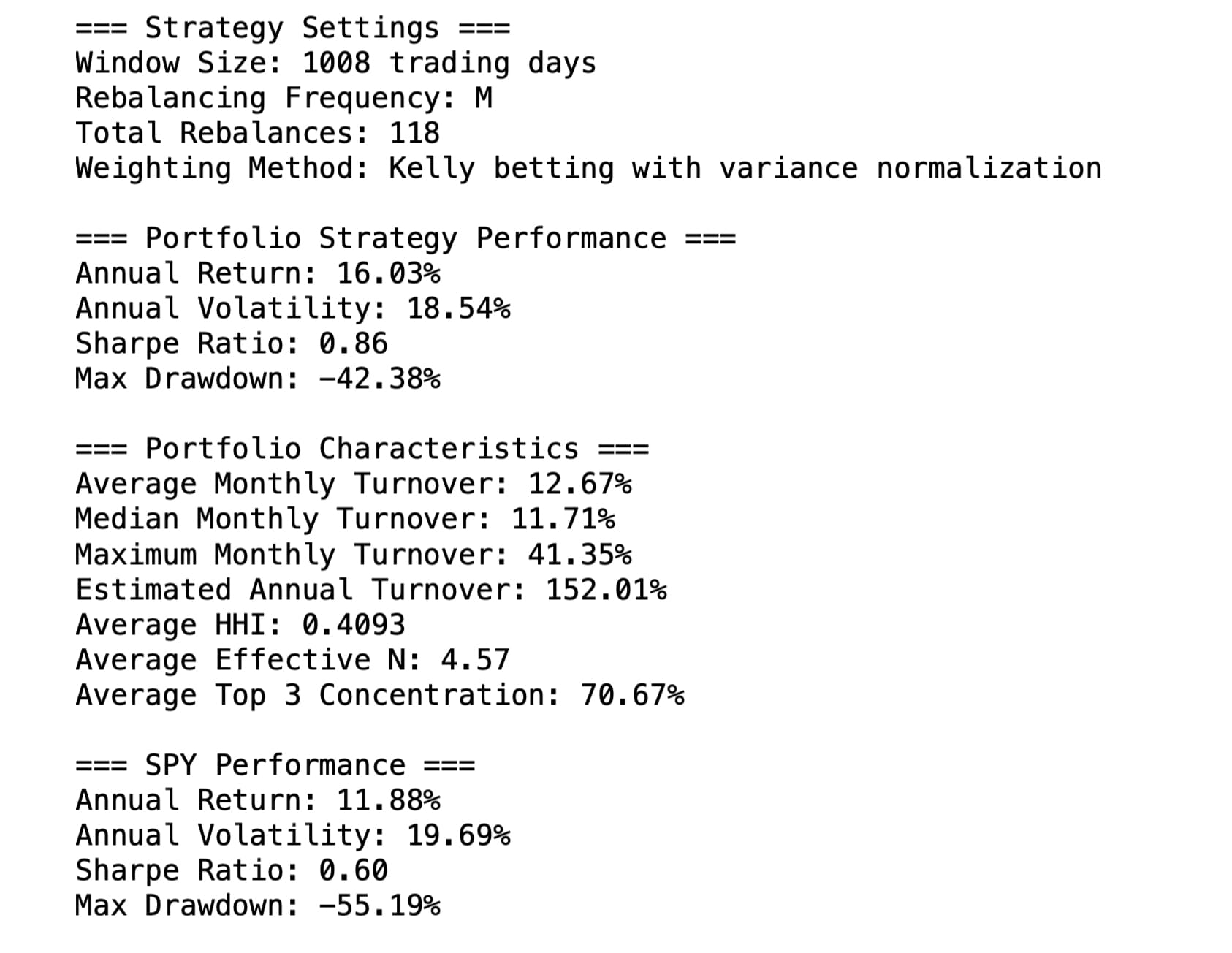

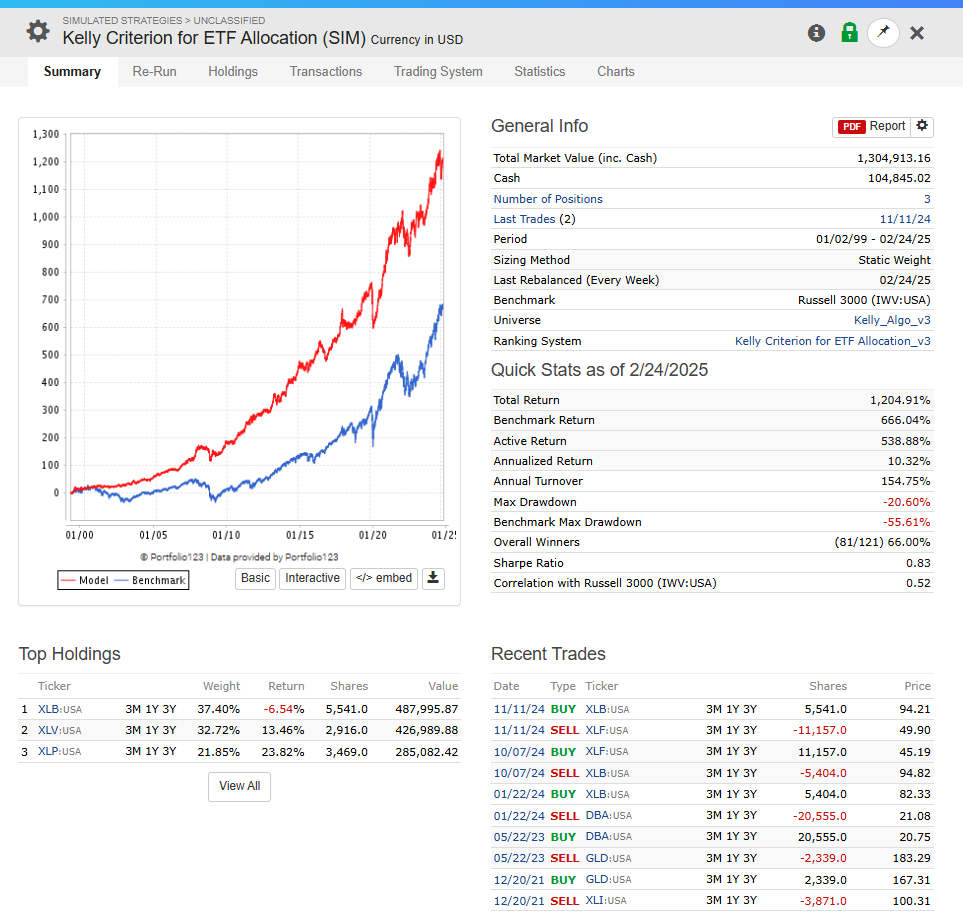

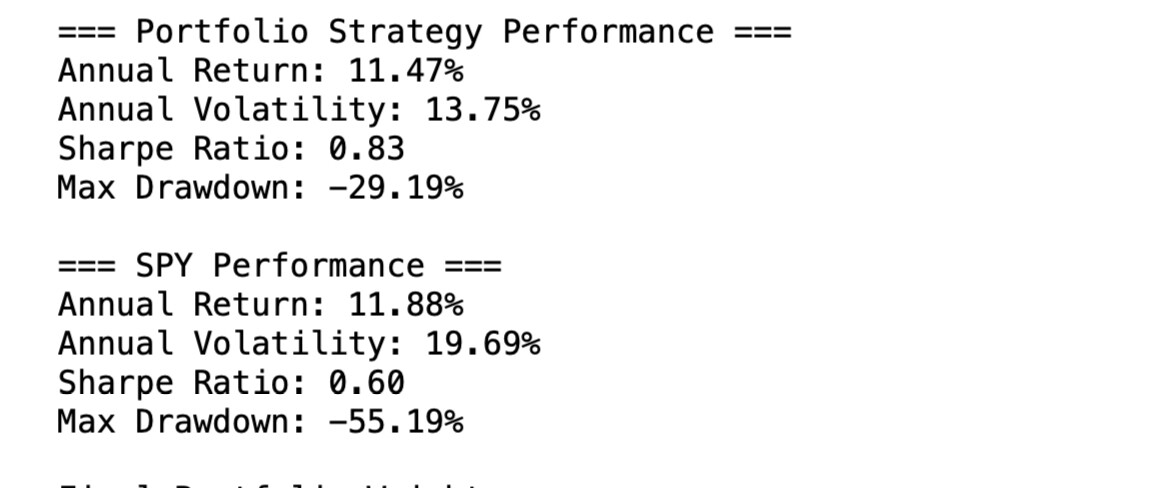

The results:

The code for those interested. You may have to use" !pip install yfinance" in a cell but it should run after doing this. You can change the parameters and the ETFs after that if you wish:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

from tqdm import tqdm

class MultiStockBPW:

def __init__(self, stock_tickers: list, benchmark: str = "SPY", n_bootstrap: int = 1000,

window_size: int = 60, rebalance_freq: str = 'M'):

self.stock_tickers = stock_tickers

self.benchmark = benchmark

self.n_bootstrap = n_bootstrap

self.window_size = window_size

self.rebalance_freq = rebalance_freq

def prepare_data(self, start_date: str, end_date: str) -> tuple:

"""Download and prepare return data for all stocks and benchmark"""

print("Downloading data...")

# Download benchmark data first

bench_data = yf.download(self.benchmark, start=start_date, end=end_date, progress=False)

if bench_data.empty:

raise ValueError(f"No data available for benchmark {self.benchmark}")

# Initialize returns DataFrame with benchmark

all_returns = pd.DataFrame(index=bench_data.index)

all_returns[self.benchmark] = bench_data['Adj Close'].pct_change() * 100

# Track which stocks have valid data

valid_stocks = []

# Download stock data

for ticker in tqdm(self.stock_tickers, desc="Downloading stocks"):

try:

stock_data = yf.download(ticker, start=start_date, end=end_date, progress=False)

if not stock_data.empty:

returns = stock_data['Adj Close'].pct_change() * 100

# Check if we have enough data

if len(returns) >= len(bench_data.index) * 0.5: # At least 50% of benchmark data

all_returns[ticker] = returns

valid_stocks.append(ticker)

else:

print(f"Insufficient data for {ticker}, excluding from analysis")

except Exception as e:

print(f"Error downloading {ticker}: {e}")

if not valid_stocks:

raise ValueError("No valid stocks found")

print(f"\nUsing {len(valid_stocks)} stocks: {', '.join(valid_stocks)}")

# Drop any remaining NaN values

all_returns = all_returns.dropna()

return all_returns, valid_stocks

def bootstrap_excess_returns(self, historical_excess: pd.Series) -> float:

values = historical_excess.values.flatten()

bootstrap_samples = np.random.choice(

values,

size=(self.n_bootstrap, len(values)),

replace=True

)

bootstrap_means = np.mean(bootstrap_samples, axis=1)

return float(np.mean(bootstrap_means > 0))

def calculate_weights(self, data: pd.DataFrame, valid_stocks: list, window_start: int, t: int) -> pd.Series:

"""Calculate weights based on probability/variance ratio"""

stock_metrics = []

for stock in valid_stocks:

# Get historical data for this window

stock_returns = data[stock].iloc[window_start:t]

historical_excess = stock_returns - data[self.benchmark].iloc[window_start:t]

# Calculate probability of beating benchmark

prob = self.bootstrap_excess_returns(historical_excess)

# Calculate variance

variance = stock_returns.var()

# Handle zero variance case

if variance == 0:

ratio = 0

else:

ratio = prob / variance

stock_metrics.append({

'stock': stock,

'prob': prob,

'variance': variance,

'ratio': ratio

})

# Create DataFrame for better visibility of the metrics

metrics_df = pd.DataFrame(stock_metrics)

# Calculate normalized weights

total_ratio = metrics_df['ratio'].sum()

if total_ratio > 0:

weights = pd.Series(

[metric['ratio'] / total_ratio for metric in stock_metrics],

index=valid_stocks

)

else:

# If all ratios are zero, use equal weights

weights = pd.Series(1.0 / len(valid_stocks), index=valid_stocks)

return weights

def run_strategy(self, data: pd.DataFrame, valid_stocks: list) -> pd.DataFrame:

"""Run the modified multi-stock BPW strategy with periodic rebalancing"""

print("Running strategy...")

n_stocks = len(valid_stocks)

# Initialize weight matrices

stock_weights = pd.DataFrame(0.0, index=data.index, columns=valid_stocks)

portfolio_returns = pd.Series(0.0, index=data.index)

# Get rebalancing dates

rebalance_dates = pd.date_range(

start=data.index[0],

end=data.index[-1],

freq=self.rebalance_freq

)

# Only keep dates that exist in our data

rebalance_dates = rebalance_dates[rebalance_dates.isin(data.index)]

# Use equal weights until we have enough data for the first window

initial_periods = max(self.window_size, 4)

initial_weight = 1.0 / n_stocks

first_rebalance_idx = data.index.get_loc(rebalance_dates[0])

stock_weights.iloc[:first_rebalance_idx] = initial_weight

# Calculate initial portfolio returns

for t in range(first_rebalance_idx):

portfolio_returns.iloc[t] = (stock_weights.iloc[t] * data[valid_stocks].iloc[t]).sum()

# Main strategy loop - only compute new weights on rebalancing dates

current_weights = pd.Series(initial_weight, index=valid_stocks)

# Track metrics for analysis

metrics_history = []

for t in tqdm(range(first_rebalance_idx, len(data)), desc="Computing strategy"):

current_date = data.index[t]

# Update weights if this is a rebalancing date and we have enough history

if current_date in rebalance_dates and t >= initial_periods:

window_start = max(0, t - self.window_size)

current_weights = self.calculate_weights(data, valid_stocks, window_start, t)

# Store metrics for this rebalancing period

metrics = {

'date': current_date,

'weights': current_weights.to_dict()

}

metrics_history.append(metrics)

# Set weights for this period

stock_weights.iloc[t] = current_weights

# Calculate portfolio return using current weights

portfolio_returns.iloc[t] = (current_weights * data[valid_stocks].iloc[t]).sum()

results = pd.DataFrame({

'returns': portfolio_returns,

**stock_weights

})

# Add metrics history to results

results.attrs['metrics_history'] = metrics_history

return results

def analyze_portfolio(self, start_date: str, end_date: str):

"""Run complete portfolio analysis"""

try:

# Prepare data

data, valid_stocks = self.prepare_data(start_date, end_date)

# Run strategy

results = self.run_strategy(data, valid_stocks)

# Calculate number of rebalances

rebalance_dates = pd.date_range(

start=data.index[0],

end=data.index[-1],

freq=self.rebalance_freq

)

n_rebalances = len(rebalance_dates[rebalance_dates.isin(data.index)])

# Calculate cumulative returns for drawdown analysis

cum_strategy = (1 + results['returns']/100).cumprod()

cum_benchmark = (1 + data[self.benchmark]/100).cumprod()

# Calculate drawdowns

rolling_max_strategy = cum_strategy.expanding().max()

rolling_max_benchmark = cum_benchmark.expanding().max()

drawdown_strategy = (cum_strategy - rolling_max_strategy) / rolling_max_strategy * 100

drawdown_benchmark = (cum_benchmark - rolling_max_benchmark) / rolling_max_benchmark * 100

# Calculate performance metrics

strategy_returns = results['returns']

benchmark_returns = data[self.benchmark]

# Annualized returns (using 252 trading days)

strategy_ann_return = (1 + strategy_returns.mean()/100)**252 - 1

benchmark_ann_return = (1 + benchmark_returns.mean()/100)**252 - 1

# Annualized volatility

strategy_ann_vol = (strategy_returns/100).std() * np.sqrt(252)

benchmark_ann_vol = (benchmark_returns/100).std() * np.sqrt(252)

# Sharpe ratios (assuming 0% risk-free rate for simplicity)

strategy_sharpe = strategy_ann_return / strategy_ann_vol

benchmark_sharpe = benchmark_ann_return / benchmark_ann_vol

# Print performance summary

print("\n=== Strategy Settings ===")

print(f"Window Size: {self.window_size} trading days")

print(f"Rebalancing Frequency: {self.rebalance_freq}")

print(f"Total Rebalances: {n_rebalances}")

print("Weighting Method: Probability/Variance ratio")

print("\n=== Portfolio Strategy Performance ===")

print(f"Annual Return: {strategy_ann_return*100:.2f}%")

print(f"Annual Volatility: {strategy_ann_vol*100:.2f}%")

print(f"Sharpe Ratio: {strategy_sharpe:.2f}")

print(f"Max Drawdown: {drawdown_strategy.min():.2f}%")

print(f"\n=== {self.benchmark} Performance ===")

print(f"Annual Return: {benchmark_ann_return*100:.2f}%")

print(f"Annual Volatility: {benchmark_ann_vol*100:.2f}%")

print(f"Sharpe Ratio: {benchmark_sharpe:.2f}")

print(f"Max Drawdown: {drawdown_benchmark.min():.2f}%")

print("\nFinal Portfolio Weights:")

for stock in valid_stocks:

print(f"{stock}: {results[stock].iloc[-1]:.2%}")

# Plot results

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(15, 18))

fig.suptitle(f'Multi-Stock BPW Strategy (Prob/Var)\n(Window: {self.window_size} days, Rebalance: {self.rebalance_freq})')

# Plot cumulative returns

cum_strategy_plot = (cum_strategy - 1) * 100

cum_benchmark_plot = (cum_benchmark - 1) * 100

ax1.plot(data.index, cum_strategy_plot, label='Strategy', linewidth=2)

ax1.plot(data.index, cum_benchmark_plot, label=self.benchmark, linestyle=':', linewidth=2)

ax1.set_title('Cumulative Returns')

ax1.grid(True)

ax1.legend()

# Plot drawdowns

ax2.plot(data.index, drawdown_strategy, label='Strategy', linewidth=2)

ax2.plot(data.index, drawdown_benchmark, label=self.benchmark, linestyle=':', linewidth=2)

ax2.set_title('Drawdowns')

ax2.grid(True)

ax2.legend()

# Plot weights

for stock in valid_stocks:

ax3.plot(data.index, results[stock], label=stock, alpha=0.7, linewidth=1)

ax3.set_title('Portfolio Weights Evolution')

ax3.grid(True)

ax3.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

return results

except Exception as e:

print(f"Error in portfolio analysis: {str(e)}")

return None

# Run the analysis

if __name__ == "__main__":

stocks = ["XLE", "XLU", "XLK", "XLB", "XLP",

"XLY", "XLI", "XLV", "XLF", "TLT"]

portfolio = MultiStockBPW(stocks)

results = portfolio.analyze_portfolio("2006-01-01", "2024-01-01")