Just want to share a thought on something I'm trying to figure out for myself. Note that most of my capital is in tax-advantaged accounts where it is not allowed to buy options.

Here is a theory. Can I:

Use market timing to give me entry/exit signals on my P123 portfolio.

e.g. exit on close below 200DMA, re-enter on close above 200DMA.

Note: I appreciate the above is too simplistic and there would be too much chop, so the P123 portfolio entry/exit signals need to be more sophisticated.

I think one core reason why "market-timing" doesn't beat "buy and hold" is because when market-timing is "out of the market", it does not generate any return. Because it just goes to cash.

So, can we use trend-following via TAA (Tactical Asset Allocation) to buy assets to generate return during the "out of the market" periods. Assets like gold, bonds, commodities, real estate which can go up during market corrections (when our P123 strategy will likely be out of the market).

So for example, buy some combination of gold, bonds, commodities or real estate based on simple trend following. This is to generate return while P123 is out of the market.

So as I said, I don't have a system that can do this but am trying to figure something out. Even if, on a backtest this generates me say 20% less annual return versus buy and hold my P123 portfolio, but gives me significantly lower max drawdown (say 25% max drawdown), I think I'd implement it.

One variation could be a simple trend filter over the asset. If it is above, then buy the asset. If not, then short-term bonds.

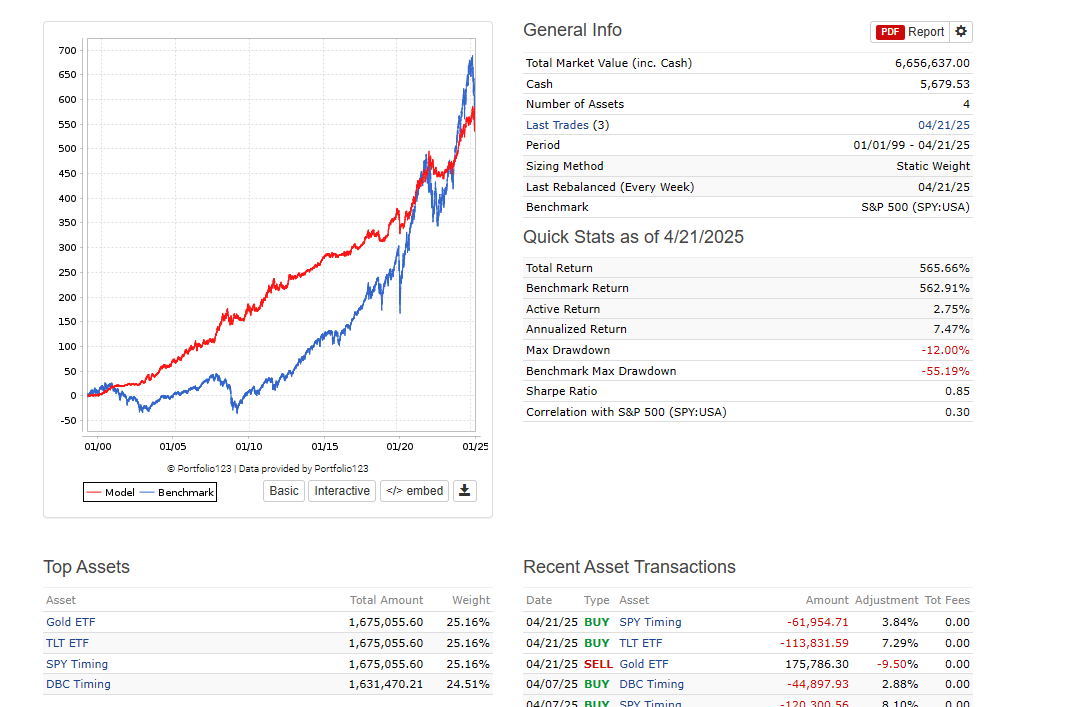

Do this for gold, tlt, spy and DBC (commodities). You really miss out on when the market is hauling butt...but it is fairly steady at around 7.5% annual return and -12% max DD.

I am not promoting this model but it is just a random idea of how you could structure it. On the other hand, your trend filters might not work. You could get whip-sawed on all the assets. Maybe they all go up like mad at the same time well above their moving average. Then crash. It is far from fool proof.

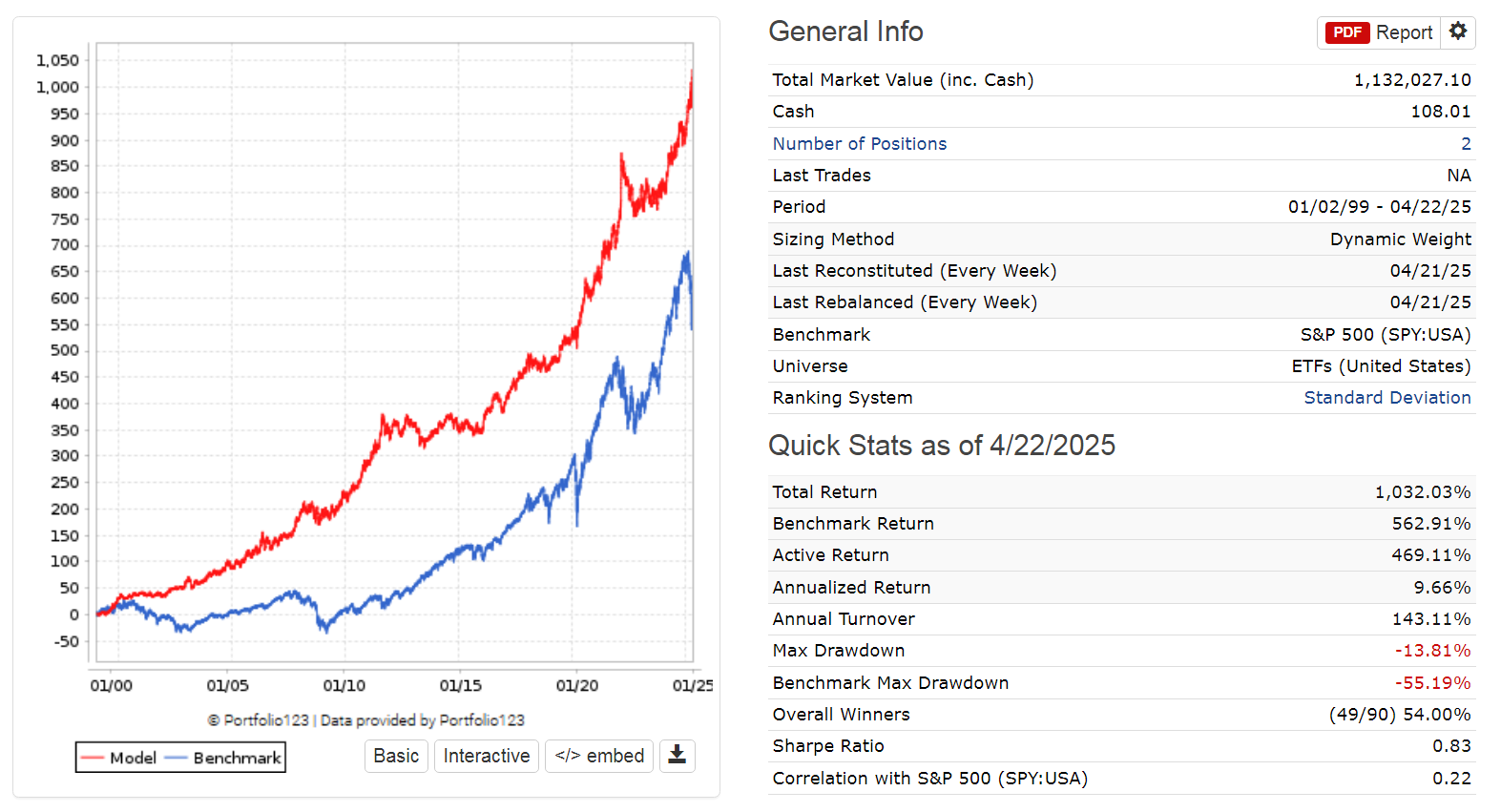

Why not use the Hemmerling Risk Meter model?

BUY: Eval( $Hem_Risk , Ticker("qqq dbc gld ief"),Ticker("shv gld "))

SELL: $1stWeekofMonth & nodays>25

Select 3 positions with a standard deviation based ranking system.

I don't know if I would have the guts or will to trade this, but using the market-timing rule set I juggle between the two allocations you have outlined. And then add a couple simple trend-following filters to ensure they are moving upwards.

It looks good but takes weekly rebalancing as well as guts of steel to go all-in on a single ETF at times. If anyone has the fortitude to go for it...keep me posted please.

Thanks all for your responses and I will take a look!

Just to be clear, my theory is to have my P123 individual stocks portfolio to be my default stocks portfolio, not QQQ or SPY. If my P123 stocks portfolio is performing ok then I'll be 100% invested in that.

Only when my P123 stocks portfolio is doing poorly (which is normally during a stock market correction), instead of just going to cash I want to pick between gold, bonds, commodities, real estate and cash. Probably 2 or 3 positions between those 5 but can opt for 100% cash.

That way, if

"buy and hold P123 portfolio" gives me say 30% annualised return but with 50% drawdown

"market timing with cash as the only other option" P123 portfolio gives me say 18% annualised return but with 20% drawdown

MAYBE

"market timing with gold, bonds, commodities, real estate and cash" as the other options can give me 25% annualised return with 25% max drawdown.

I made those numbers up to show the difference between the options. They objective is to get close to the "buy and hold P123 portfolio" returns but limit the max drawdown.

Stated another way, it's like Tactical Asset Allocation (TAA) but with my P123 individual stocks portfolio as the replacement for SPY/QQQ/Other stock market index.

At the moment, it's all theory and trying to figure it out. Open to suggestions.

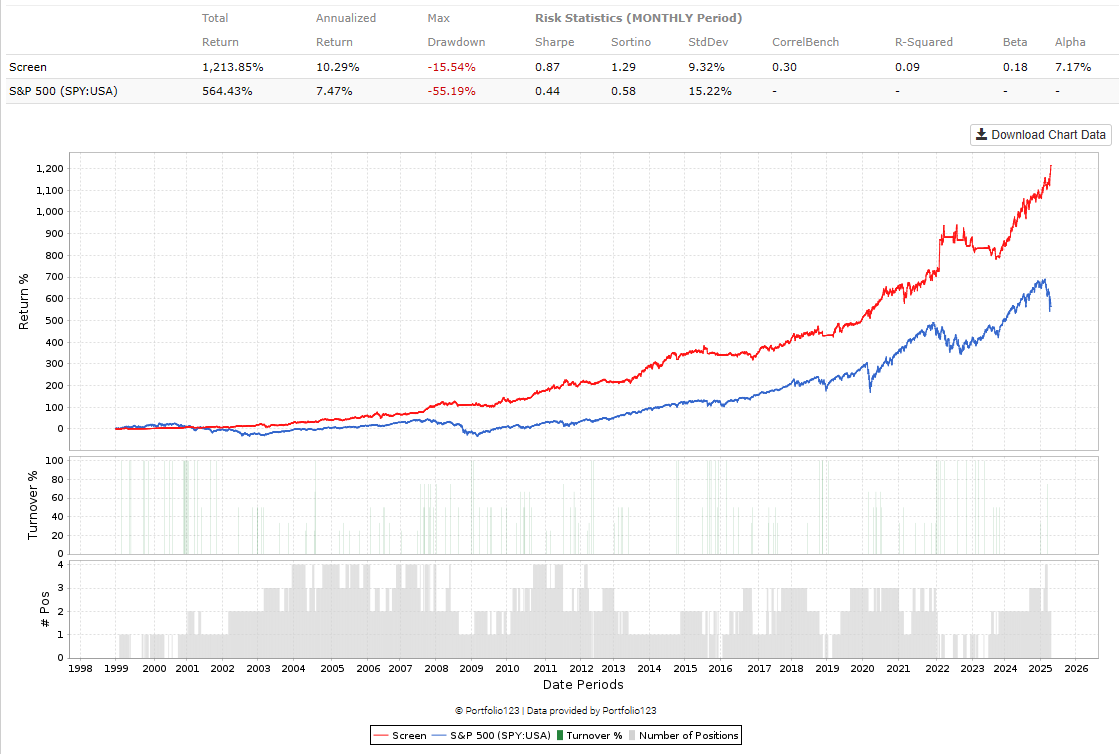

Anything that gives a 20% annualized return with a max D/D of less than -30% is great. If you could make 20% a year you would double your investment every 5 years. What more do you want?