I have an existing IB account that I want to leave alone. I would like to carve off a second (and potentially third) account with the goal of automatically trading it. I hate IB customer service. Can someone that has done this tell me the best setup process so I don’t mess it up? Master acount and sub accounts? or just new account, new number, link that to Portfolio 123?

You’ll want to set up a new separate account with IBKR and link that account number to p123. I have two taxable accounts and two IRAs at IBKR and only link one of the taxable accounts and one of the IRAs to p123. That way, I can trade unsupported securities like options in one of the unlinked accounts without having to constantly enter reconciliations into the p123 ledger.

Note that you will split up your portfolio margin by having multiple accounts, so be mindful of that. It may be a plus or minus depending on your point of view. With multiple IBKR accounts, you can also select your market data billing account in your IBKR account settings. This will select where market data fees are debited from, and I set this to my most actively traded taxable account, which happens to be the p123 linked account, so that I hit the commission minimums for waived market data fees.

IBKR posts fees/credits on I think the 4th or 5th trading day of the month, so expect to see reconciliation notices about differing account balances at that time. As I mentioned in another thread, it takes me about 5 minutes once a month to enter the various IBKR fees (margin interest, short interest credit, borrow fees, foreign dividend withholdings) as p123 journal entries. Note that commissions and dividends are tracked automatically.

I had looked at setting up a non-professional advisor account so I could trade through a single master account (F account) and control the allocations to the underlying U accounts: my IRA and my wife’s IRA for example. But this isn’t possible today through p123 linked accounts.

thank you. Appreciate it. Are you brave enough to trade european stocks? since markets are open at different times, wouldn’t that make it almost impossible to manage trading multiple markets?

I could not disagree with this any more. IB platform (Trader Workstation) looks like it was built in 1989 for MS-DOS. It has a huge and unwieldy learning curve. Maybe it has something for advanced traders that I don't understand but for us lowly retail investors, I think all other platforms I have used are superior: Schwab, Ameritrade, Think or Swim, etc...

The bureaucracy at IB is at world record levels.

My most recent frustration happened a month ago when my son turned 18.

They locked his Uniform Gift for Minors account and told us we needed to transfer it to a new regular IB account. The next day we made him a new account and initiated a transfer (IB to IB). Two weeks later, nothing. I called in to see what the hold up was and they told me it could be months before they got around to it. They said it had to go through multiple committees or some nonsense. I told them "Never mind, I'll liquidate all his holdings. Send us a check. Surely that can be done faster." They told me even that had to go through a review process, implying that it could fail the review process, in which case.... they will keep his life's savings? Its been more than two weeks and still nothing. You can't actually speak to anyone with any authority so calling them is pointless. They have effectively hijacked my son's account for an indefinite amount of time. As a side note, they also will not give my 20 year old or my 18 year old a margin account.... just because. That makes it much more difficult to use the P123/IB semi-auto method. This is one of many examples of the kind of thing you have to deal with at IB. Tradier is a dream in comparison and I plan to move most of my accounts to Tradier.

Yes, I do trade both Canadian and European stocks, but directly in my non-linked IBKR account and not through p123. I have a couple live Canadian and European live books/strategies but linked trading of those markets is not yet supported by p123. I’ve been waiting a while for that feature but last I heard, it was pushed back to focus on the ML features first.

Since I’m manually entering orders, I don’t trade all names that my strategy holds because I don’t want to manage so many positions manually. IBKR knows market hours and holidays for each security so I can generally just submit an algo order and not need to worry about it. But algo orders are not always available for some of the smaller EU markets, e.g. Poland for example.

I also use VWAP but it’s next to useless for stocks with low liquidity. For stocks with more liquidity I have heard that Fox River VWAP is truly excellent. Then there’s the accumulate/distribute algo, which seems complex at first but is actually quite intuitive. It takes some work to set up so I haven’t done it yet and since I’m probably going to stop using IB in a month or two I doubt I’ll get around to it. But I’ve heard excellent things about it and it looks like a terrific tool.

I personally use Percent of Volume for orders in my linked IBKR accounts. First, it’s one of the few IBKR algos supported by p123 (adaptive is not one of them). But it tends to favor more immediate execution than VWAP orders. Keep in mind that different algos may have different benchmark prices that they are trying to achieve or beat. VWAP orders are designed to achieve or beat the VWAP benchmark price over the order’s duration. For day orders, the VWAP order will likely spread execution over the entire day’s volume curve. Algos like Arrival Price or POV are benchmarked against the current price. Others like Target Close are trying to achieve the closing price.

So why do I favor more immediate execution? There are a couple reasons, but first check your strategies and see how they react to “Price for Transactions”. If “Next Open” strongly outperforms “Next Close”, you certainly have an argument for trying to achieve the arrival price over the closing price. But what about VWAP price? It’s not currently available in p123, so I view “Average of Next Open, Close, and 2X High” as a poor man’s proxy for the VWAP price. Again, if “Next Open” outperforms, you have an argument for more urgency. Maybe there’s some short-term alpha there, maybe you’re just benefiting from more immediate execution of long orders in the prevailing tide of rising markets. Either way, I don’t argue with the data.

For trading in my IRA, more urgent execution is even more important. Since only limited margin is available, I can’t simultaneously execute all my buy orders and my sell orders – I need some sells to fill first. If I were to send my sell orders as Day VWAP orders that executed over the entire trading day, I may not be able to submit the last buy order until the next day.

All that being said, my use of POV orders is more of a marriage of convenience than anything else. There are several things I do not like about IBKR’s POV algos.

They only participate in IBKR’s ATS (dark pool). Roughly 40-45% of US trading is off-exchange, typically on various brokers’ dark pools, but the IBKR ATS is only ~2% of that off-exchange volume. These are aggregate market statistics of course, but you’re missing out on a lot of liquidity.

They do not participate in opening or closing auctions, which can be about 10% of volume. I haven’t checked but I would expect their VWAP orders to participate.

Even with attempt to never take liquidity set as an option, they don’t seem to do a great job of getting passive fills.

IBKR exposes an “attempt to match block trading volume option” which p123 does not support. It doesn’t appear to be documented anywhere, but presumably the default behavior is to not follow off-exchange trading volume reported to the TRF, which means the POV order is potentially tracking the 55-60% of lit volume, which leads to…

POV orders feel slow to fill. My executed volume is sometimes well under my target percentage of market volume.

I do plan to explore other execution options, though it’s not my lowest hanging fruit at the moment. Fox River has had a very good reputation for execution, so they’re at the top of my list to try.

Let’s take this argument to its logical conclusion. I assume the reason “next open” would outperform “next close” would be that the price is closer to the price upon which the ranking and buy/sell rules are based. If this is indeed the case, then “next open” would outperform “next close” if the simulation is a strong one and would not if the simulation gives you crappy results. Furthermore, “previous close” would outperform “next open,” since that would match the ranking precisely. And that is what other users have found: when using a heavily backtested simulation, “previous close” gives you the best result, “next open” gives you the next best, and “next close” gives you the worst. Therefore, the aim should be not to fill at the next open, but to fill at a price very close to previous close. However, all this assumes that you trust a backtested simulation to answer this question rather than what might work best out of sample.

The reason for the assumption that led the previous paragraph is that if opening prices always provided better fills than closing prices, you should stop stock-picking and simply buy AAPL at open in one account and sell AAPL at open in another, then reverse that the next day. Since your fills will be better at open than they would be at any other time of day, this neutral position will make you a lot of money.

Obviously, I’m kidding. You can see how illogical that is. So the only possible explanation for better performance with open prices than with close prices is fidelity to the model, and for that the ultimate goal should be to get fills close to the previous close. (And yes, opening prices are closer to the previous close than closing prices.)

The problem, then, is twofold. 1. Can you apply this logic to out-of-sample buys and sells? 2. What about market impact?

I’m agnostic regarding the first question. But as for the second, the whole idea behind VWAP orders is to evade market impact. In my experience they do so quite successfully. My transaction costs for non-VWAP orders are significantly higher than they are for VWAP orders. If you’re buying very liquid stocks or buying very small amounts, you don’t have to worry about this and you can stick to your market-on-open orders. But if you’re worried about moving the market even a little, then VWAP orders have some very nice features.

I’ve been using Fidelity for decades and see no reason to stop now. My wife’s and kids’ accounts, my cash account, my 401K, and my private foundation are all at Fidelity. I have a relatively small account at IB for Canadian and European trades and I’m going to close that since I’ll be moving all my IRAs to my hedge fund, which will be using Goldman Sachs as its prime broker. Goldman doesn’t service quite as many European countries as IB (I’ll definitely miss my Polish stocks!), but I’m pretty sure it’ll be less of a headache to trade with them, and I’ll finally be able to trade on the Oslo exchange.

What percentage of daily volume are you willing to max-out at for a strategy’s holdings. Are you willing to purchase 30% of the total volume for a ticker, for example? Or do you hold it at 20% or some other number?

Perhaps your calculations are more complex than that. My question may oversimplify what you do but I would be interested in what kind of percentage of daily volume you are comfortable with when buying a micro-cap stock. Assuming it can be simplified to maximum percent of daily volume.

I’m afraid it depends on a number of things:

a) am I doing a rebalance of existing holdings? or am I injecting or withdrawing a great deal of money from my portfolio? if the former, my limit is going to be higher than if it’s the latter.

b) the volatility of the stock. If it’s low I’ll have a higher limit than if it’s high.

c) how much I would like to buy if I were unconcerned about transaction costs and delay costs.

Lately I haven’t been buying more than about 60% of daily dollar volume. But back in June I bought 200% of the daily dollar volume of ELTK in one day. That cost me more than 2% in transaction costs. But it might have been worth it.

I’m not sure I buy in to the explanation that “previous close” outperforms because it is a better match to the ranking system. I think it outperforms primarly because it cheats. In practice, our p123 factors and ranks aren’t recomputed and available at 16:00 ET Friday afternoons when the closing auctions occur. Even if were to build infrastructure to compute factors/ranks in real-time, by the time the closing price posted and I made a decision to trade or not, it would be too late for me to participate in that closing auction. I’d have to trade in the post-market session or wait until the Monday open.

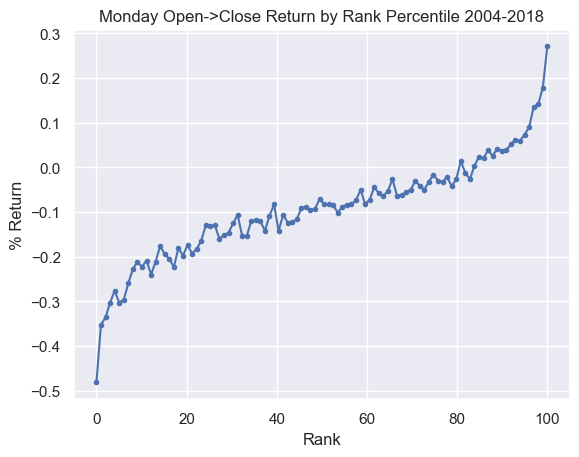

I looked at the data more, and I do believe in the case of my particular ranking system and universe that I do have some intraday alpha for my top-ranked stocks that merits more urgency in execution. I examined the intraday returns (opening price to closing price) for all Mondays (the days I initiate trades) over my 15-year in-sample period of 2004-2018. Grouping by rank percentile, the 100th percentile stocks return 0.27% from Monday’s open to close; the 0th percentile returns -0.48%.

I will concede market impact is an unknown here, and the lack of VWAP prices in p123 further complicates the analysis. For now, let’s assume that our VWAP prices are the average of the open and close. In that case, my VWAP prices on my trading days would still be 0.135% higher than the opening price on average for my top-ranked stocks that I’m buying. So, in theory for my buy orders, I would prefer an execution algo achieving the arrival price over a vwap algo as long as its slippage wasn’t 13.5 basis points worse than the vwap algo. And there’s no way to answer to that question without testing them out empirically yourself.

What “non-VWAP” orders are you referring to here? Is it another Fidelity algo or are they orders that you manually worked yourself?

Doesn’t this mean that you should buy at Monday’s open and sell at Monday’s close? I’m sure the stocks you’re selling still rank higher than 80. Would you then take this logic further and sell on Tuesday or Wednesday? What about Friday? Just use margin to tide you over! After all, margin rates are less than 0.05% per day.

OK, I’m being a bit facetious here, but using intraday price moves is always a double-edged sword. The only scenarios in which your logic holds are a) you buy a lot more than you sell due to a rapidly expanding AUM or b) the difference in rank between the stocks you buy and sell is very large. If neither of those is the case, then buying at open and selling at close (or a few days later) will be better for you than placing all your trades at the open.

They’re limit orders I’ve placed manually or using one of IB’s pegged orders.

To be clear, I was only claiming in my above post that my buy orders should be higher urgency at the open. I looked at this strategy’s orders, and its average closing rank is 96 – on average, stocks at that rank return 0.14% from Monday’s open to close over the in-sample, so I would be better off trading those with less urgency or towards close if I expect these results to hold up. It’s a high turnover strategy, about 14x/year, so that change would have yielded up to 2 percentage points of excess return over the in-sample assuming similar transaction costs.

I trade a different, lower turnover strategy in my IRA, but there I have to execute sell orders, at least partially, before I submit buy orders to open new positions. Presumably, some of your trading is in a tax-sheltered account. If so, how are you sequencing those trades? Assuming your account is fully invested, some of your buy orders would have to be either: a) delayed to a subsequent day, b) submitted later in the day as sell orders liquidate, or c) submitted for smaller amounts and modified up as sell orders liquidate.

It doesn’t surprise me that your transaction costs for VWAP orders are lower than your “non-VWAP” manual order working strategy, but it’s possible your transaction costs could be even lower with other non-VWAP algos.

That’s not a knock against VWAP orders at all. I think it’s a fantastic default for many cases, and I think most users would be better of using them over manually working orders, in both time and lower costs. Brokers employ teams of researchers and developers to build these execution algos and smart order routers to lower transaction costs and market impact, so why not avail that as much as possible. That applies doubly so if you’re trading through GS.

That said, in addition to exploring Fox River algos through IBKR, I’m also going to experiment with the VWAP and TVOL algos in my Fidelity account. Looking at the most recently quarterly SEC 606 filings from IBKR and Fidelity, it looks like Fidelity does a better job at sourcing off-exchange liquidity. For 2023 Q4, IBKR routed ~80% of non-S&P500 orders to exchanges while Fidelity only routed ~40% of non-S&P500 orders to exchanges. That’s a stunning difference, a lot of which is due to the PFOF providers like Citadel that Fidelity has agreements with, but Fidelity also executed 12.8% of those orders in their ATS while IBKR only executed 3.7% of orders in their ATS. This seems consistent with my anecdotal experience of the IBKR smart order router doing a poor job at sourcing liquidity for lower liquidity stocks.