Jim,

I have re-attach the paper again. See if you can download it.

Regards

James

All that Glitter is not Gold.pdf (532 KB)

Jim,

I have re-attach the paper again. See if you can download it.

Regards

James

All that Glitter is not Gold.pdf (532 KB)

Jim,

Although it remains a secret how they does it, the stat arb strategies at Medallion Fund (Renaissance Technologies) includes different types of strategies such as index arbitrage, basket trading and delta neutral strategies, not simply paris trading + leverage. Their statistical arbitrage trades were mainly market neutral which explains its low standard deviation. RT also empahsis on strategies with high risk adjusted return due to its use of high leverage in the Medallion fund.

Regards

James

James,

Thank you.

I find the Sharpe ratio interesting too. I did not mean to minimize its importance. I should have only emphasized that I am still trying to figure out the best way to use this. IN FACT, I ALREADY USE THIS FOR INVESTING. I use it but I think I have a lot to learn. For example, I do not (yet) have a formal way of excluding things with low expected returns, like bonds.

Already, I invest in a minimum variance portfolio as calculated by modern portfolio theory. But each ETF in this minimum variance portfolio has done about as well as the S&P 500. I use the Sector SPDRs to construct this portfolio.

So I agree this is important. I just do not yet have a formal way of excluding things like bonds. Thing that have low volatility but the returns are too low.

Perhaps, a formal way to exclude bonds would be to select that Tangency Portfolio (again from MPT). This selects the portfolio that maximizes the Sharpe Ratio and would exclude bonds.

Instead, I have taken ETFs that have performed about as well as the S&P 500 and selected the Minimum Variance Portfolio using these ETFs. There isn’t really much separation of these portfolios (the Tangency portfolio and the minimum variance portfolio) along the efficient frontier as you probably already know.

So I think I mostly agree with you. And in fact, my belief that the correlation is not so low in this paper actually adds importance to your idea, I think.

There are some papers that support this. It seems we are not that good at prediction returns but the volatility does persist whether we try to predict it or not. Minimum variance portfolios tend to outperform other portfolios out-of-sample in those studies. The volatility drag plays a role in producing improved out-of-sample returns in these studies.

This mirrors the interest in low volatility stock portfolios that are probably accomplishing the same thing, in practice, but without a formal calculation of the Tangency or Minimum Variance Portfolio.

Thank you again.

-Jim

James,

yes you are right! I cuts out the up vol (which is good) and only measures the down vol.

Sharpe measures both sides and therfore punishes for upside vol, which I think is crazy.

Best Regards

Andreas

James,

I am sure you are aware that Ed Thorp did something very similar. He did very well until Rudy Giuliani brought racketeering charges against his fund in one of the worst cases of prosecutorial excess IMHO. Ed Thorp was never charged and the charges stemmed from “parking” which is a questionable way to avoid taxes.

BTW, the “basket trading” you mentioned has caused the IRS to bring a case for billions of dollars against RT. Something that is still being litigated…

-Jim

Jim,

Basket options enabled Medallion to wager far more capital than it controlled (leverage something like X10 times capital) and seriously boosting the funds returns. Also unlike more conventional leverage strategies, such as those used by LTCM, the risk remained mostly with the banks. The most Renaissance could lose was the option premium and its collateral.

This strategy also helped Medallion avoid paying short-term capital gains taxes since the average holding period of the fund is only 2 days. Barclays/Deutsche has stopped selling basket options to Medallion and other hedge funds since 2013 due to the ligation from IRS. It is unclear how Medallion obtains its high leverage since then but the fund continues to provide above 65% annualized returns (before fee) since 2013.

Regards

James

James,

One lesson I have learned is that if you hedge you have to hedge ALL RISKS. Or, perhaps, just keep the leverage at a reasonable level that will not make you unable to continue trading if the unexpected occurs.

Ed Thorp provides an example. At one time he was shorting copper. For his long hedge he had real cooper stored in a warehouse.

Well the copper was stolen from the warehouse. His strategy worked because he had insured the copper (a type of hedge) and he ended up making money from the insurance payoff.

Similarly, RT must be doing well about hedging all possible outcomes.

Long-Term Capital Management did not do so good as far as hedging against the Russian Bond default.

Very interesting and indeed a proven way to make money if you hedge against all of the potential risks.

Thank you for the link and the interesting discussion.

-Jim

Not at all crazy and in fact, extremely sensible, in fact, inevitable.

The so-called punishment for upside volatility is only relevant when looking at the past. It tells you what happened to the stock in one specific time period. But unless we can invent a time machine and go back and trade as of the starting day of the period measured in Sharpe, we learn nothing about what can happen in the future.

Let’s not get carried away with what a statistic is. The Sharpe ratio, like other statistics, has no existence in and of itself. It’s just a number we use to tell us about something else. When investing for the unknown future, we need to be thinking about the “something else” that made the shapre ratio what it was.

The “something else” here is the collection of company characteristics that caused the profit to be what it was, and that cause the set of investment community expectations around it to be what it was. When you look at this, you wind up thinking about the kinds of things that cause business stability or volatility. What’s the business? How steady or volatile is demand for the company’s products or services? What’s the internal structure of the business? How large a portion of total costs is fixed. Etc., etc. etc.

When you look at it this way, what you discover is that the factors that caused a stock to exhibit extreme upside volatility are EXACTLY the same as those that can lead to comparable downside volatility, and vice versa. A high Sortino tells you that the company had big swings when things went well for it in the past. But that same high Sortino, if you read it correctly (which means ignoring it, knowing its garbage, and going back to Sharpe) also tells you that if things go less well down the road, you can expect the company and its stock to get horrifically hammered.

Sortino is absolutely positively the stupidest ratio I have ever seen and is an example of the raw idiocy that can result when quants and statisticians run around like lunatics without “domain knowledge.” I haven’t seen the actual Sortino paper so I don;'t know how the ratio was presented to the world, but if he suggested there was such a thing as a stock with inherent asymetrical future volatility potential, then he should have been fired rather than published.

If one wants to put this in statistical terms, looking ahead, ex ante probabilities for companies are symmetrical with variations mainly in the 4th moment of the distribution. But after we pass through time and look back ex post at the one scenario that actually occurred, we can see things that if we forget where we started may lead to the illusion that the distribution was asymmetrical. IOW, with company-stock analysis, its always symmetrical ax ante and asymmetrical ex post. But we can only invest ex ante.

Moral of the story: If you load up on high-Sortino stocks and get hit with a bad market, expect extreme damage to your portfolio.

Marc hides his quant abilities for a legitimate reason that I do not fully understand. Perhaps to appear humble or perhaps because he does not think we will understand.

Indeed, I have quant aspirations but do not know what the 4th moment is. He is right, I do not understand.

Others show great talent in machine learning and quant abilities over on SeekingAlpha. Only to demean it here on the Forum.

Sometimes they are marketing something they do not want you to do yourself so that you will pay them. Sometimes it is to win a debate and appear to be the smartest person in the room which, again, can help with marketing.

A successful debate-winning fallback position here at P123 is to say you only believe in fundamental analysis and say something like: Anyone who uses the quant skills I display and write about over on SeekingAlpha is making a mistake. Some on the forum are fooled time and time again.

I wish it would stop. P123 needs to stop supporting it.

I THINK MANY ARE NOT FOOLED. They just do not want to enter into such a debate and are silent. In fact to put it in quant terms, there is an inverse correlation between how good of a quant a member is and how much they wish to post here. Many people understand.

I know what this inverse correlation says about my quant abilities and I say: Right again. But I do not try to hide what limited abilities I may have.

-Jim

I don’t try to “hide” whatever quant skills I have. As to the nature of my skill set, it’s high or low enough to have developed an understanding of when things are applicable to a particular problem and when they are not, and to recognize good quant versus bad quant.

Over the years, I’ve noticed on the forum that many seem to operate from an implicit assumption that more quant is better than less quant, and I’ve seen it elsewhere too. That’s completely wrong and is why the quant community is now in the throes of an existential crisis as an increasing number in the media are openly attacking the competence of the field.

That needs to be edited. Here goes.

A successful debate-winning fallback position here at P123 is to say you only believe in statistical analysis when combined with “domain knowledge” and say something like: Anyone who uses quant skills unaccompanied by domain knowledge is making a mistake. Some on the forum seem to believe this. That’s unfortunate. They are wrong and to the extent they are investing real monet based on such beliefs, they are endangering their financial well being.

It’s up to Marco to choose what P123 will or will not support but speaking for myself, I strongly encourage P123 to never stop reminding quants of the importance of domain knowledge and to encourage them to take advantage of opportunities to obtain and improve upon it, which is something any skilled quant should desire.

I stick with the original: no edit needed as I was not referring to you Marc.

Hence the use of the word ‘others’ in this sentence after discussing your legitimate reasons for not using statistical terms in general:

I stand by everything I said. Will document if you wish.

-Jim

Not sure who the others are. But if anybody is under the impression (hopefully not from me) that quant/statistics is of no use, well, it is possible to invest without it. But my commitment to p123 and platforms like it reflects my belief that it can enhance the heck out of domain knowledge. I can travel from NY to LA by horseback (or walk), but as long as airplanes have been invented, I’d rather use one of those.

It would appear that Andreas is the only one in this post who does not believe in statistical method nor risk adjusted measurments like Sharpe.

Regards

James

Jim,

Instead of investing in a minimum variance ETF portfolio that does not beat the benchmark. You should check out OMFL (Russell 1000 Dynamic Multifactor ETF). This ETF has been extensively researched and its holdings rotate between Recovery (Size,Value), Expansion (Size, Value, Momentum), Slowdown (Low Volatility, Momentum) and Contraction (Momentum, Low Volatility, Quality) based on different economic conditions. Attached is a research paper by London School of Economics/Oppenheimer Funds for this ETF.

Regards

James

James,

I will definitely check out the ETF you suggest.

The cool thing about minimum variance is that that the returns are usually better out-of-sample. Often because of the reduced drawdown and reduced volatility drag.

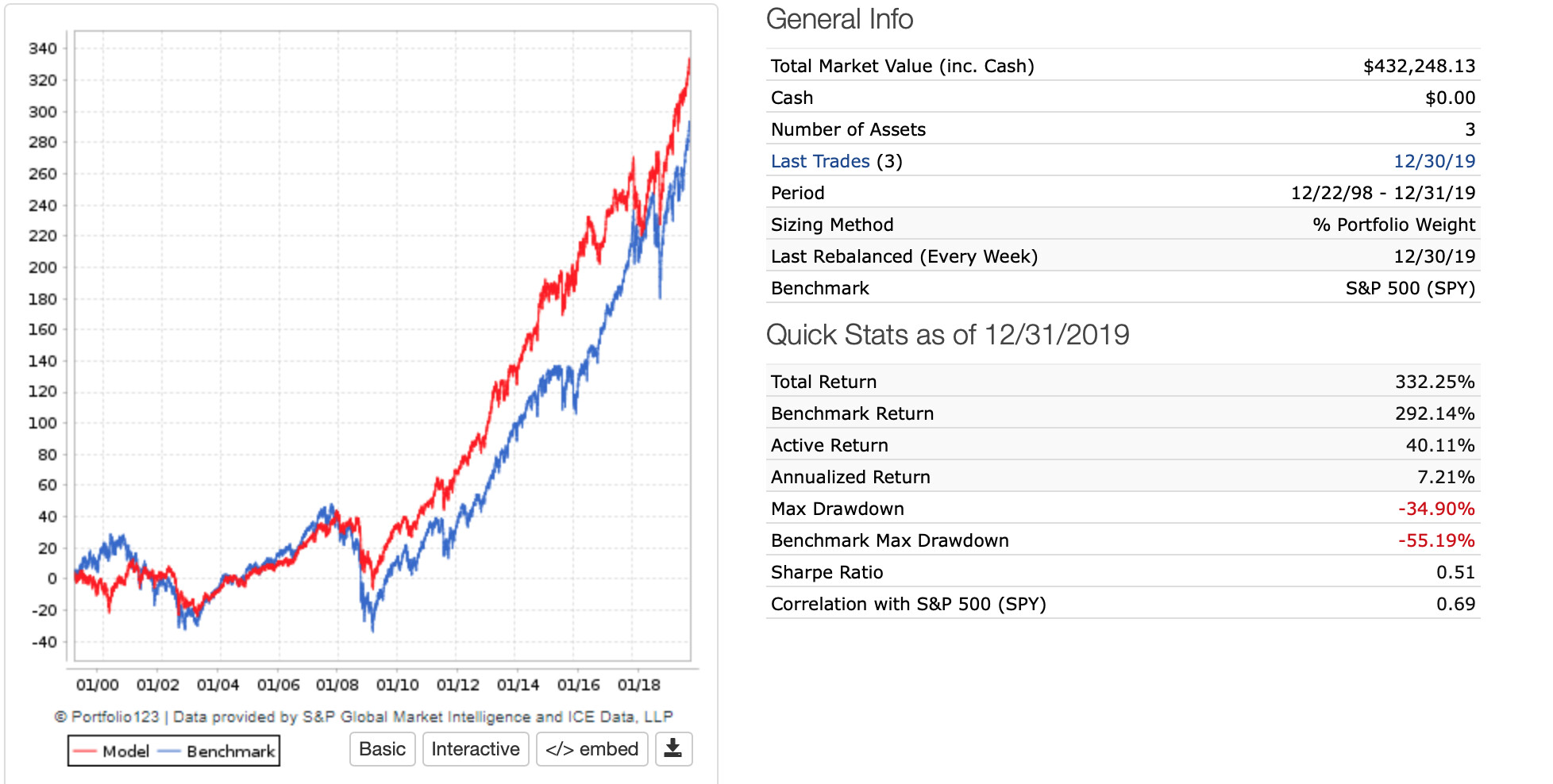

This is what I have some of my money in now and it does beat SPY. This is the minimum variance portfolio made up of the sector SPDRs as calculated in Python. Better returns than SPY and less drawdown.

-Jim

Jim,

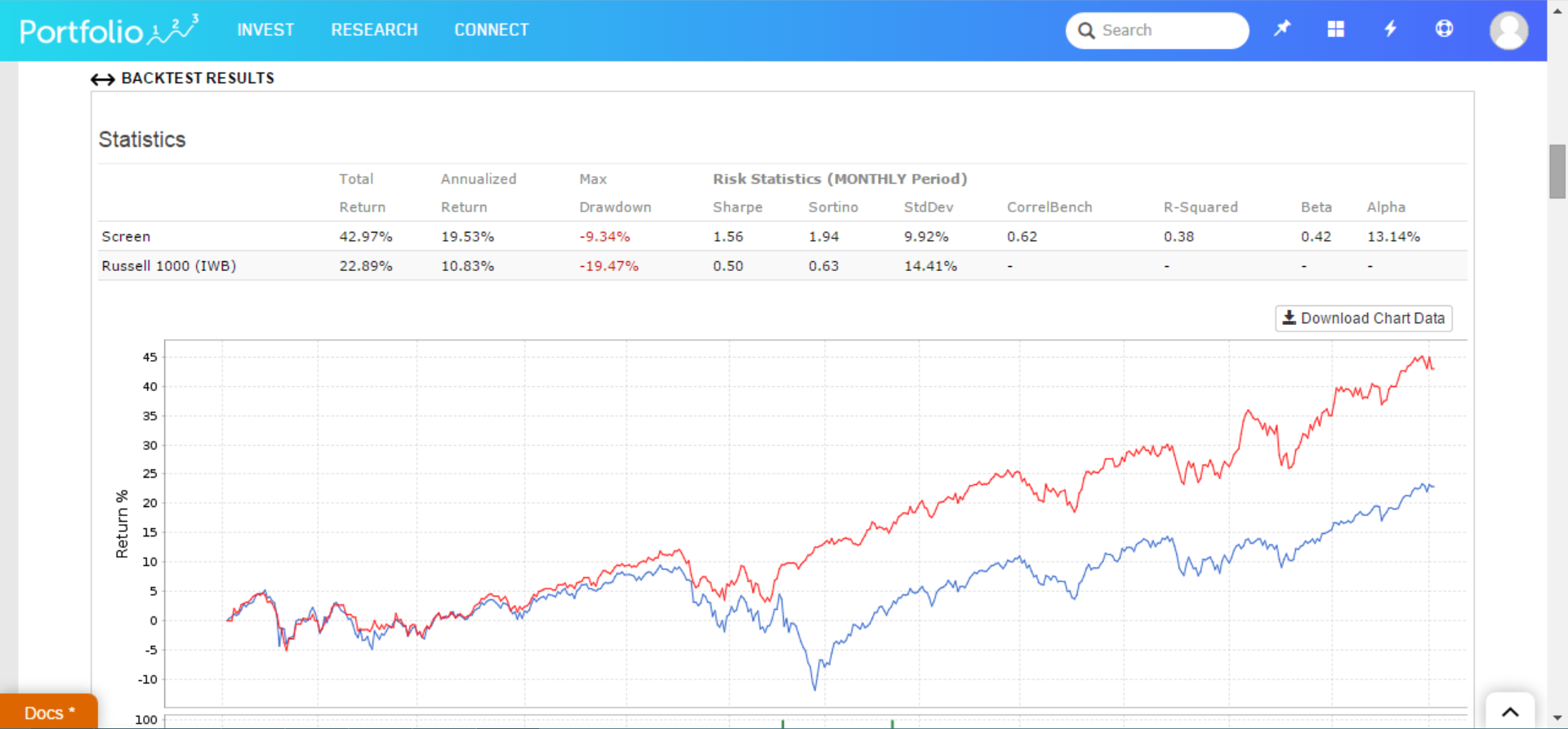

This is the performance of OMFL (which has only been officialy launched for 2 years) together with a market timing rule that will switch to GLD when Aaa US treasuries and BBB corporate bond spreads widened by a certain amount. The annualized return is nearly doubled the benchmark (IWB) with a standard deviation that is 30% smaller.

Regards

James

James,

I will definitely look into the ETF. If nothing else, I will probably add it into the equation of a minimum variance portfolio—especially considering the low volatility of this ETF. Low variance that may persist according the paper cited in your post.

Clearly my minimum variance portfolio could use some more ETFs. I need to work on which ones to add (beyond the one you suggest).

The idea of reducing the variance is pretty new to me. I am still trying to sort out what lessons to take from your posts, the paper and the Modern Portfolio Theory.

What do you look at when deciding to invest in something now? Are you using some of the methods of RT like pairs trading? Actually, any additional ideas welcome.

Thank you.

-Jim

Hi James and All,

Yes, I simply do not get myself to use statistics that have an assumption of the normal distribution of returns. I just do not want to make that first order thinking mistake!

And as the paper says, Sharpe has not a good prediction for OSS (at least that is what I have understood).

What is important to me: how does the system react / behave after a DD, does it have “ZING” (which I define how long it takes to make a new high relative to the market).

But there is another, very important of topic philosophy side of it:

Because I do not define risk = price volatility. Especially not on a stock basis, but also not on a portfolio basis.

I go with Mr. Buffet here: Risk for Mr. Buffet is losing everything or missing out long term total return (I use loose market timing, but only because it increases total return). BC only with (total) return I can buy stuff.

The Porsche dealer does not tell me, “hey I only take your 200k for a Porsche Turbo S if you have reached it with a strategy that is risk adjusted.” He or she will take the 200k, but he or she will not give me a discount if I only have 100k reached with a risk adjusted return strategy.

So why does the world try to learn from Buffet (on value and quality, compounding, moats, you name it), but that very important part (“risk is not price volatility”) the world does not try to learn from him?

The answer is, because one would have to change to be mentally tough and independent, change is what people fear the most and that edge for the small group of tough ones will never go away. That mental toughness is 80-90% of the game! (For me its 100% because I have already a good enough total return strategy).

Risk adjusted return is fine if you are already rich (let’s say north of 10 Million, for me it would be 100 Million, for Mr. Buffet that is probably never the case and I guess that is a big reason for him to be pretty rich), but if you want to have life changing returns (in one lifetime not spreading out to generations) for you and your wife and your kids you got to “eat some grass” (or be a genius, which I am definitely not, I know that and I admit that to me!).

I have four choices:

Trade my total return strategy today and do not miss out total return: For that I need to develop a psychological edge that I have to develop and meditate (working out and good foods, good relations friends and family help too) on it every day, that is much easier to develop then what you need for option 4, being a genius, so it’s a rational decision to get a high mental fitness.

A. Being not a genius and try to find the holy grail (let’s say 50% ann. with a max DD of 12.5%) until I am blue in the face and miss out total return in the meantime or (better)

B. search to get better and still work on my mental fitness and trade the total return stuff (which is kind of what I am doing too and that helped to develop a strategy which is better than I ever dreamed of).

Or trade lower risk-adjusted strategies and losing out total return (just because I can not get my self into a mental stage to trade a good total return? I must admit, that is not my tee).

Be a genius, find and trade the holy grail (I am not a genius, so that is out of reach for me).

The other big advantage of Option 1 and 2.b (with discipline!): I will not go into the curve fitting risk (because I think I am a genius, when I am not), just because I want to reach a perfect capital curve, just because I cannot toughen up.

Millions fool themselfes and try option 4. and they miss out total return at the same time (Option 1) just because they can not get themselves to work on their mental fitness and trade total return with hefty DDs.

There lies an edge for us (!!!):

To choose Option 1 or 2.b (without going into the trap to overfit and use statistics to fool us that have a wrong first order assumption, e.g. prices have normal distributions and have no fat tails).

Best Regards

Andreas

James, thank you for the tip on OMFL (could be an ETF to buy when my market timing tells me to exit), looks a lot like the strat from hedgeye (the call the different market regimes Quads).

Do you have a link on the research of the OMFL ETF?

Best Regards

Andreas

Andreas,

I respect that and have no reason to make you change.

But I have never understood why you started your investing by placing so much emphasis on statistics i.e., the FAMA and FRENCH papers which are only statistics. Academics doing statistics.

I do not understand how you can rationally value their statistics so much and then discount every other statistic you encounter afterward.

Not that it is wrong, I just cannot understand it.

-Jim