It seems there are large number of models that using timing / trend following to switch in and out of assets. (Dual momentum, etc.). What are people’s thoughts on for example a 70/30 stock/bond allocation when the market is above some timing metric and a 30/70 allocation when it’s below. Obviously the timing mechanism and allocation ratio can vary, but this seems to be a good combination of trend following and “buy and hold” allocation that would reduce whipsaws and drawdowns associated with a timing system that zigs when it should zag during a sideways / choppy market. I have modeled this in excel a bit and it seems pretty solid. It has you in a more conservative allocation during a big bear market, but still has you in some equity when things turn.

Yes, you can model this easily in P123 with the new rebalancing module:

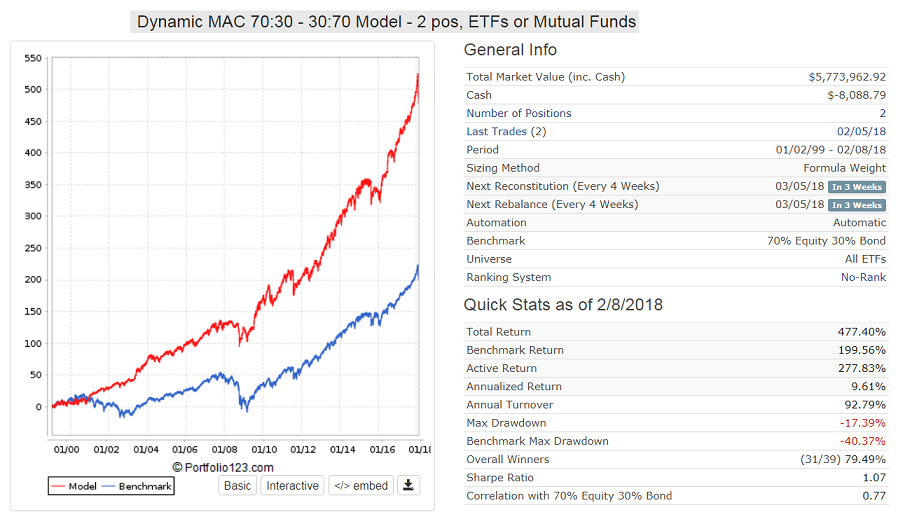

Here is such a model which uses a 50/200 MAC of S&P500

Georg,

Can you share the formula you used in the Rebalancing module to achieve this result (or do you consider it proprietary)?

Thank you,

Chris

Glad to share:

This model uses 2 bond and 2 stock ETFS: it holds 70%VTI + 30%BND during up-markets, and 70%BIV + 30%VIG during down-markets. In the current interest rate environment it is perhaps advisable to use shorter-term bond funds.

Buy rule: eval(sma(50,0,$sp500)>sma(200,0,$sp500),ticker(“VTI,BND”),ticker(“BIV,VIG”))

Sell rule: eval(sma(50,0,$sp500)<sma(200,0,$sp500),ticker(“VTI,BND”),ticker(“BIV,VIG”)) & nodays>60

(nodays>60 is specified so that mutual funds can be used as well)

Rebalance Sizing Method: Formula Weight

Ideal Number of Positions: 2

Reconstitution Frequency: Every 4 Weeks

Allow Immediate Buyback: Yes

Rebalance Frequency: Every 4 Weeks

Max Portfolio Drift: 0% From Ideal Weights

Position Weight Formula: 70Ticker(“VTI”) +30Ticker(“BND”) +30Ticker(“VIG”) +70Ticker(“BIV”)

Max Position Drift: 0% From Ideal Weight

Min Rebalance Transaction: 5.00%

Since the model can use mutual funds, trading costs and slippage are taken as zero. Annualized Return from 1999 to 2018 is a respectable 10% with max D/D of -17%, better than most mutual funds. This is a good retirement investment strategy for min anxiety.

I just wish P123 enable the formula in Book - so I can combine my stock stimulation (instead of stock etf) portfolio with bond etf portfolios

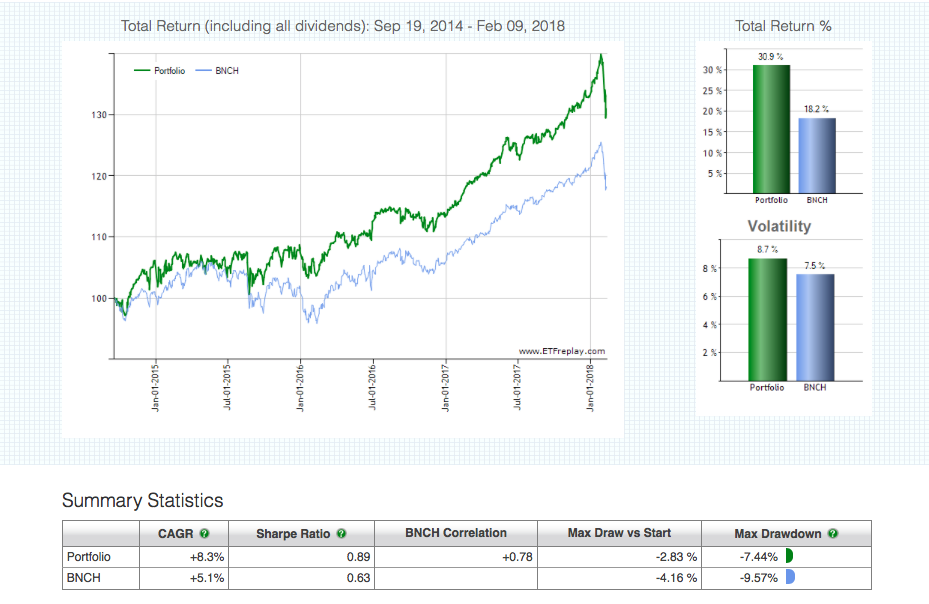

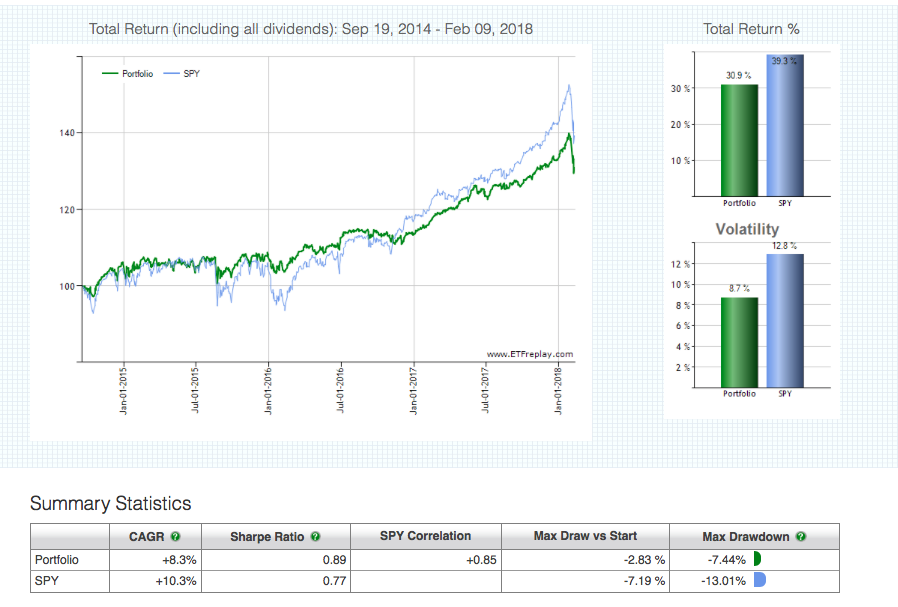

Here’s simple 1/3 allocation to QQQ, RSP and BTAL since September 2014.

Crushes a 60-40 benchmark with similar volatility and less drawdown.

Better risk adjusted returns and much better drawdown vs SPY.

The one very large thing that would be good to fit in with all of this is the ability to optimize based on mean variance. I do not know of any way this can currently be done in the variable weighting formula. But to have the ability to mix and match correlations - either with stocks or just ETFs - would be powerful indeed. A great strategy overlay to ‘book formula weighting’.

Hi guys. I am experimenting with multiple ETFs not just the two from Geov’s example. I need some help as I cannot find the error here:

70ETFAssetClassSet(EQUITY) + 30ETFAssetClassSet(FIXINC) - 40Ticker(“VIG”) +40Ticker(“BIV”)

@P123: Not sure why this weight rule gives an error. if this is not allowed for the weight rule, why is it? Could you please allow it?

This discussion is really helpful. I’d like to use these ideas to implement a dynamic allocation into treasuries for a stock strategy but I don’t see how.

Suppose I have a custom formula $market that gives the market climate as a score 0-10. For an ETF strategy I could use for custom weights:

$market*Ticker(“SPY”) + (10-$market)*Ticker(“IEF”)

This works well, but how can I use the is the context of stocks?

One possibility would be to have a stock universe that includes IEF, but I’m not sure ETFs and stocks can be together in a universe. If it were possible, an allocation could be implemented using something like:

$market*MktCap/MktCap + (10-$market)*Ticker(“IEF”).

Any ideas?