Has anyone performed analysis or found research papers on where to split your strategies?

For instance, it seems to me that US and Ex-US are reasonable splits, but should that be more like US, Canada, EUR, and China, where common tax and laws are applied, as such each should have its own strategy?

What about by market cap size, e.g., should we just filter by Small (<2B) or should Nano, Micro, and Small each get their own strategies?

What about combinations between location and size?

What about splits between Value and Momentum? e.g., since these are targeting different market inefficiencies, shouldn't we ensure that these indicators are not in the same ranking system?

Finally, what about hedging? Puts? TWM? or Shortable Stocks?

It seems to me that there is an enormous ocean of possibilities for where to split strategies and then recombine back at the book layer that would enable better overall results vs trying to fit everything into a single AI or Ranking strategy?

I don’t think of this question as one of splitting something up explicitly, but of how to productively combine smaller pieces, each with a different view on a market subset, into a portfolio. I’m at a Screener membership level and use a NOOTC based universe with a $50M market cap and $200K median daily volume which is about 3300 stocks.

What has EVOLVED is a set of small screens, currently 22, with between 7 members (2 screens) and 2 members (9 screens). Overlapping holdings are allowed. What has made the difference is the money management rules where I use a weighted return metric focused on more recent periods which in turn gets mapped to money allocation weighting so the top return metric gets a 4X weight, decreasing by 0.5X weight until 1X is reached. Below a 0.6X metric level the screen gets defunded and below 0.75 it is put on probation at 0.5X weight. Weights are multiplied by screen holding size, summed, divided into the allocated equity amount to determine the X position dollar amount. This approach allows catching rising screens and stepping away from falling ones. Unfortunately, one of the trade-offs is turnover of roughly once a month. This approach is roughly your book question.

I caught a Morningstar podcast last fall which defined the smallest 10% of cumulative market cap as starting at $12B. I have not found limiting by market cap to be effective. The micro-cap screen is barely hanging in as probationary and the large cap only somewhat better.

Combining multiple style factors in a screen is more productive than just one as some such as Momentum, Quality, Sentiment, and Volatility play better in a supporting role.

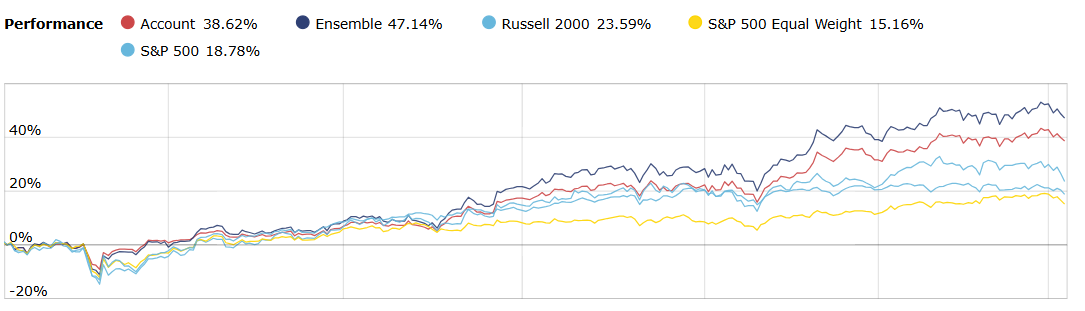

These are my results over the last year with Ensemble being the equity only portion of the account. I more than doubled the number of screens last summer with the weighting picking up and running with the precious metals run.

Let's take Value and Momentum as you said; why not build a value system and a momentum system, combine them in a book, and rebalance periodically?

In my head (e.g., not tested), if inefficiency is present, it should be exploitable, and rebalancing via a book would enable uncorrelated strategies to deliver higher overall returns.

Then expand that idea to the entire ocean of potential strategies, locations, sizes, etc.

Well, if you're splitting, as the topic head suggests, how would you decide which stocks were in each system? What if a stock is in both? Or neither? I'm a bit confused by this.

If you're not splitting, you can certainly choose the best value stocks and the best momentum stocks and combine them in a book, but the returns are almost certainly going to be lower than if you choose the stocks that have both value AND momentum.

This approach could work in AI systems and clustering, not easy anyway. In linear as @yuvaltaylor pointed out I doubt it. You can see studies of that as well in bibliography " What works on Wall Street" for example

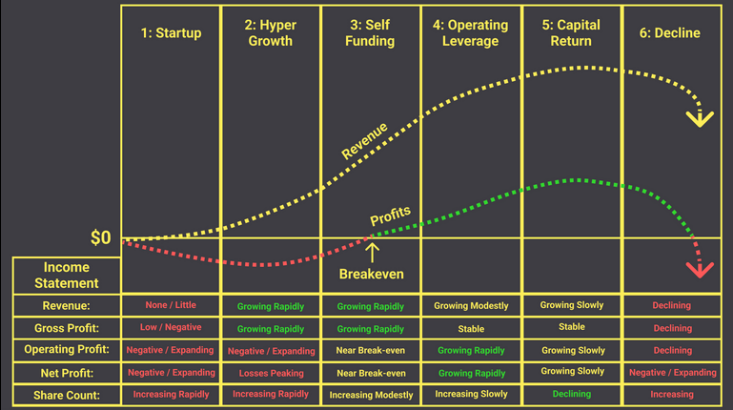

I find the Corporate Life Cycle a good guide to split strategies.

I think most of us invest between cycle 2 and 5, but to find the winning hyper growers and while comparing with undervalued stocks in the capital return phase is very compromising in a ranking system.