Just curious, I love chatting with people in person about this stuff. Are there any in person meetings that happen currently? Anyone around Ontario, Canada?

I’ve read/reviewed the results of 500+ financial studies, completed my own 100-year long backtest simulations in python on huge stock databases, plus configured 5000+ simulations on portfolio123. Experience with data analysis, coding, research, web programming etc. Finished my BBA several years ago, now working in healthcare lol (also fun to me). If anyone’s interested in meeting up, let me know.

I used someone else’s for a few weeks. Unfortunately no more access now. They usually only sell to corporations or schools I think so hard to get your hands on it.

It was interesting while testing, it seemed like factors go in and out of favor for very long periods sometimes. So even if a factor appears invalid for the last 20 years, it might still be working, just it’s in a temporary long term down trend. A factor’s alpha can be negative for 20 years, then be 5-10% excess a year for the next 20 years.

Also sometimes fairly minor changes in my models would keep the same returns in the long term, but the last most recent 20 years could have vastly varying results.

I wonder if a 20-25 year backtest is ideal with portfolio123, given that some factors fall temporarily out of favor for decades sometimes.

I was reading a machine learning study recently also that said that 20 years is possibly not long enough for testing machine learning because it picks up on more noise and short term trends.

It’s funny to think of 20 years as short term though.

Maybe that means we should weight longer history more?

For example, PB ratios are unpopular recently but we should add them because they are effective in the past tens of years?

Or, do we need to assign more weight to the value factor, despite the recent better performance of the growth factor?

I've heard before that 20 years is short as well, but the rolling validation of the P123 AI tool seems to indicate that even 1 year of data can yield some meaningful results, albeit not so much. So I am confused!

I never thought a year's worth of data was even enough for machine learning

Hmm interesting, maybe 1 years worth of data is helpful for certain types of factors that can be picked up on in a short term time frame - I would think short term reversal and momentum perhaps.

But yeah I think using long term trends in returns rather than short makes sense. Ideally backtesting with as many years as possible. I think most trends don’t disappear too quickly in small micro and nano caps at least. Some studies suggest that on average after a study is released on a new factor the returns decline by 30% or so as more investor crowd the strategy.

But hard to know what the future holds. The fund AVUV is a value fund that ranks returns by predictive models and they use a lot of growth metrics as well and have excellent results since inception. But there’s also been a massive trend in growth investing lately of course.

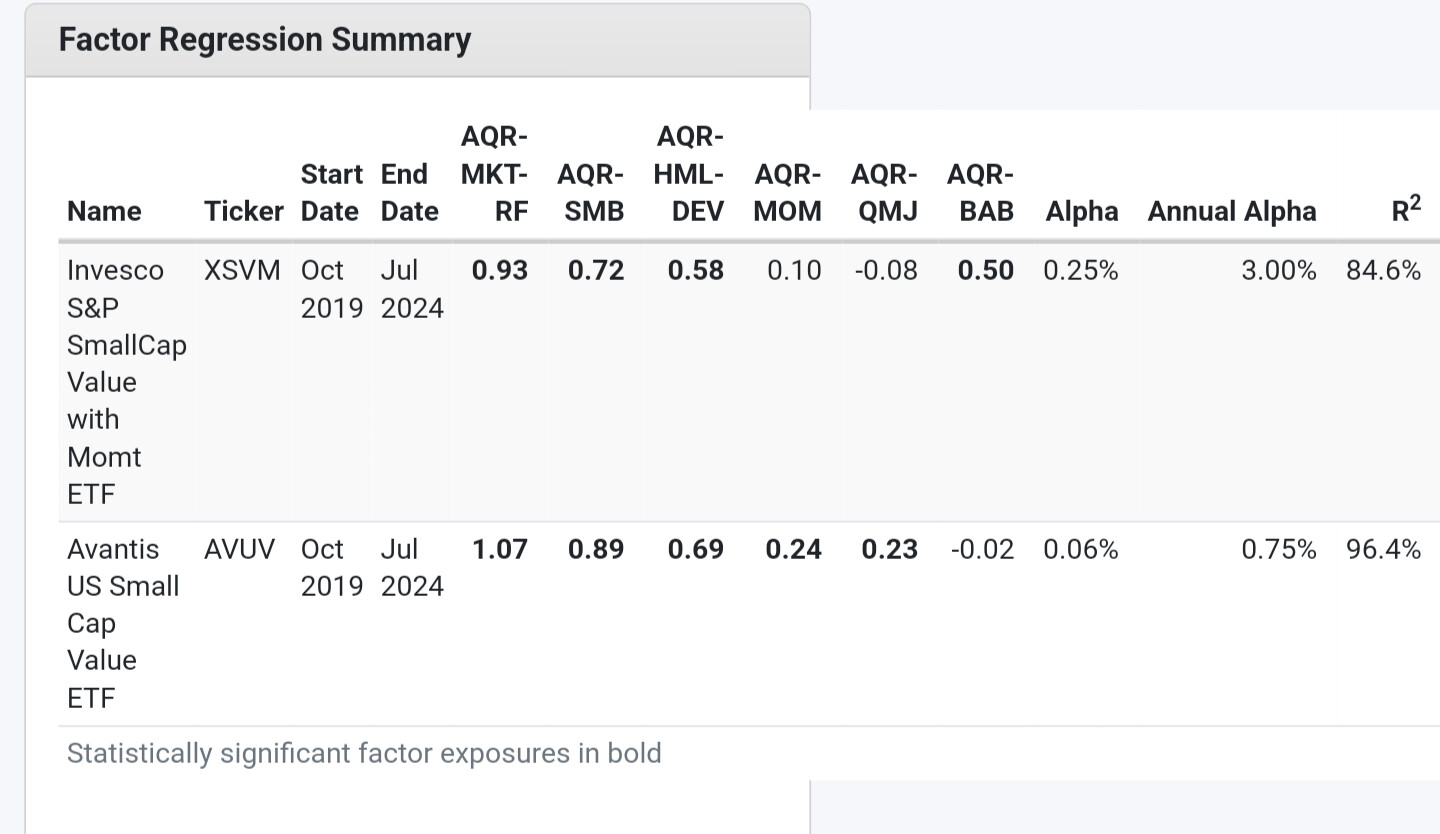

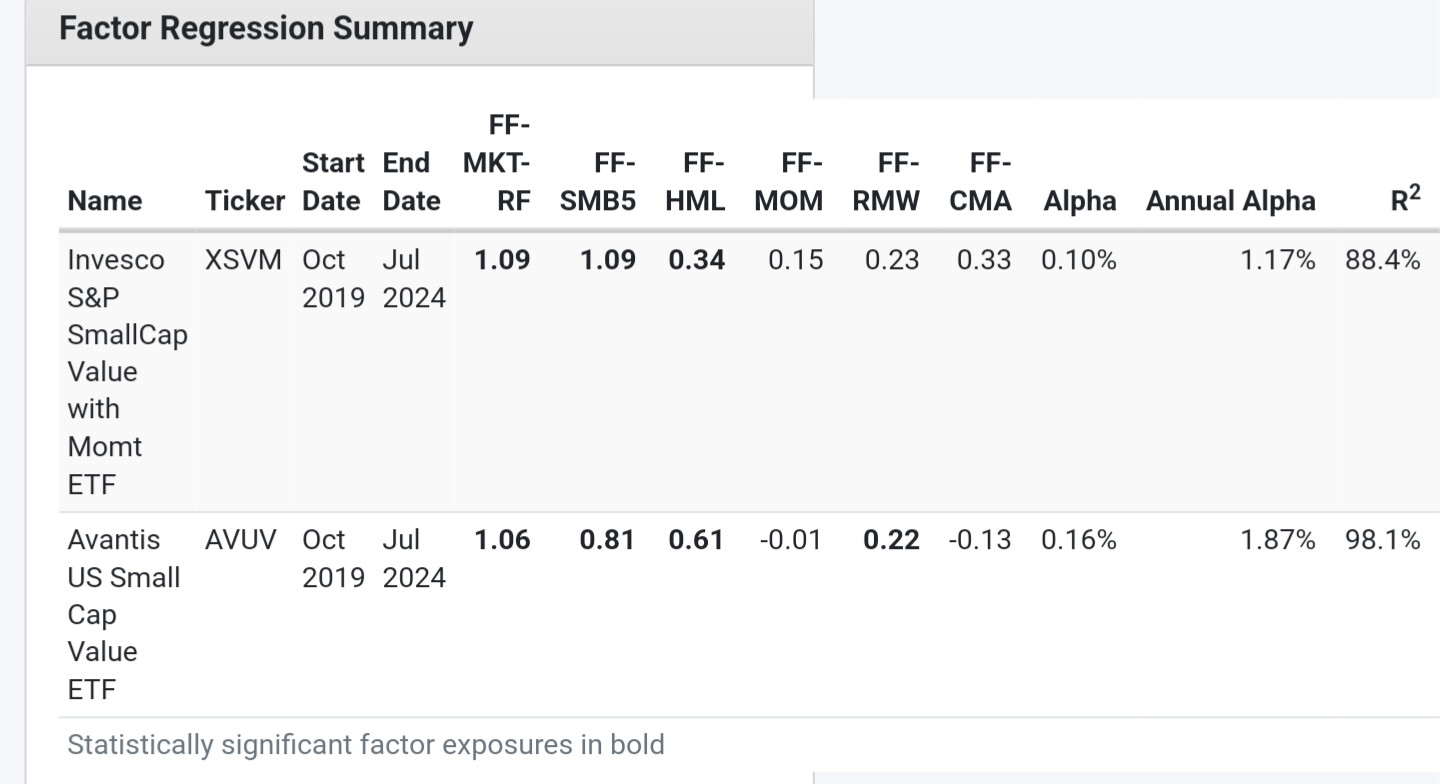

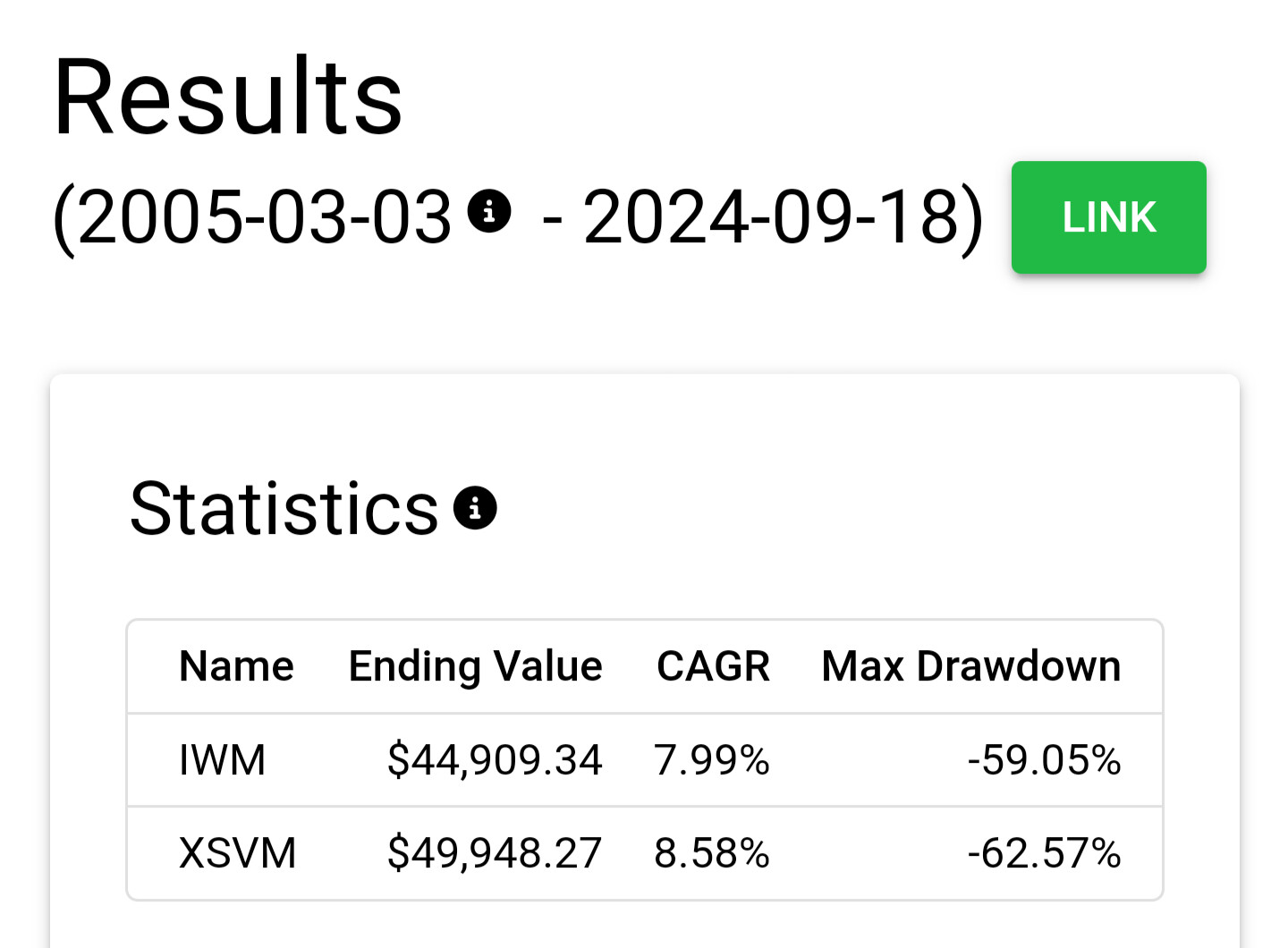

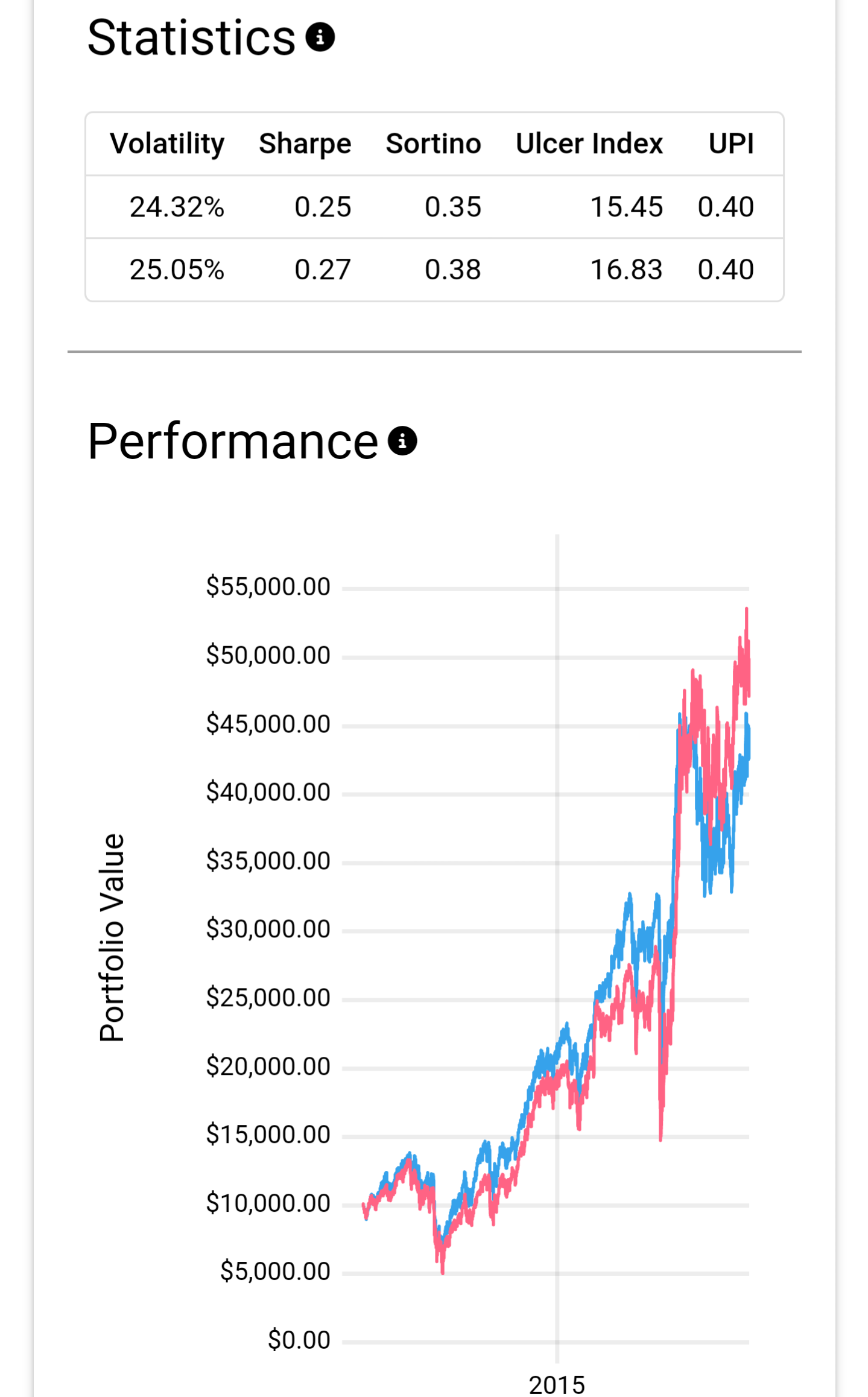

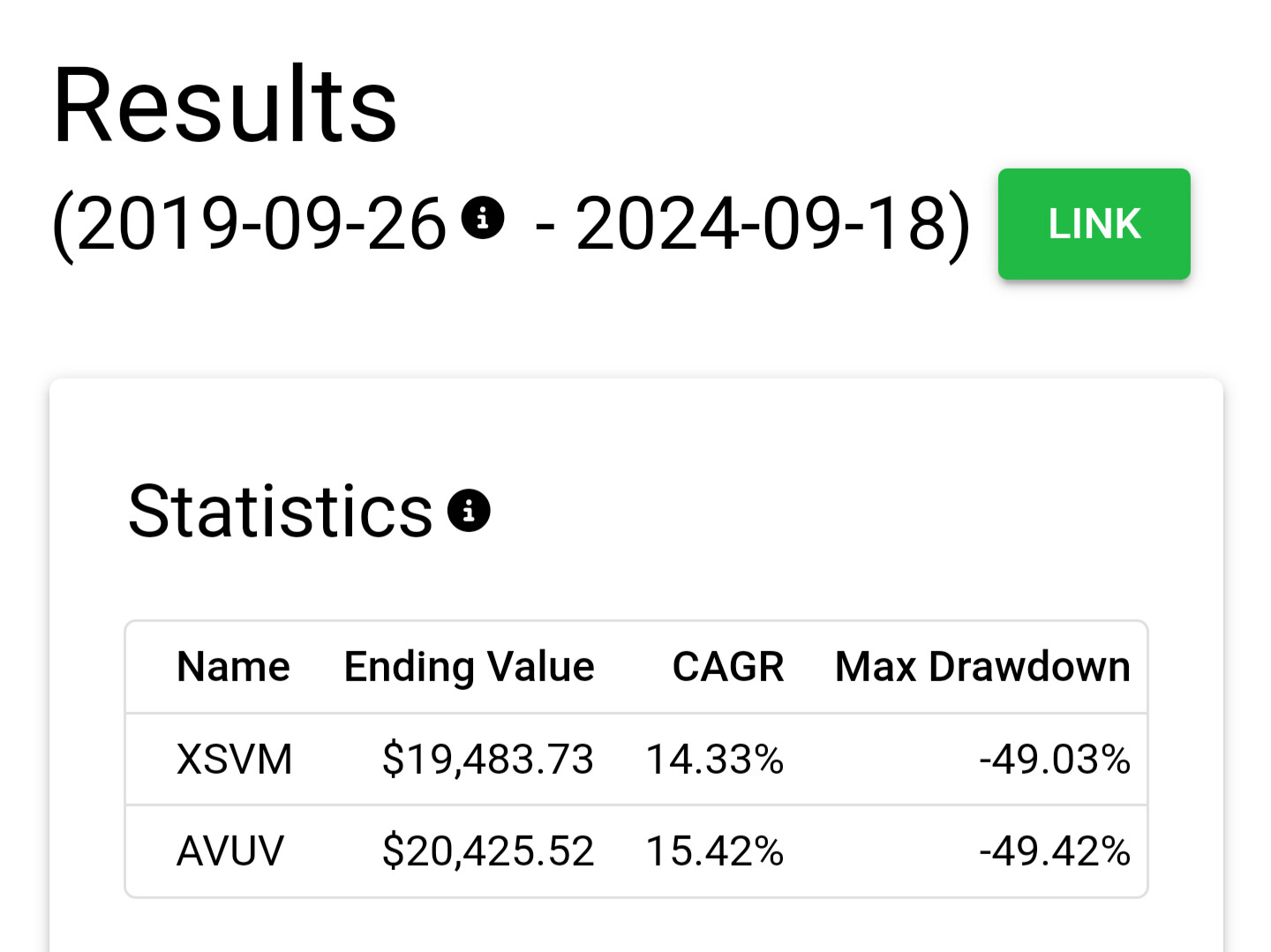

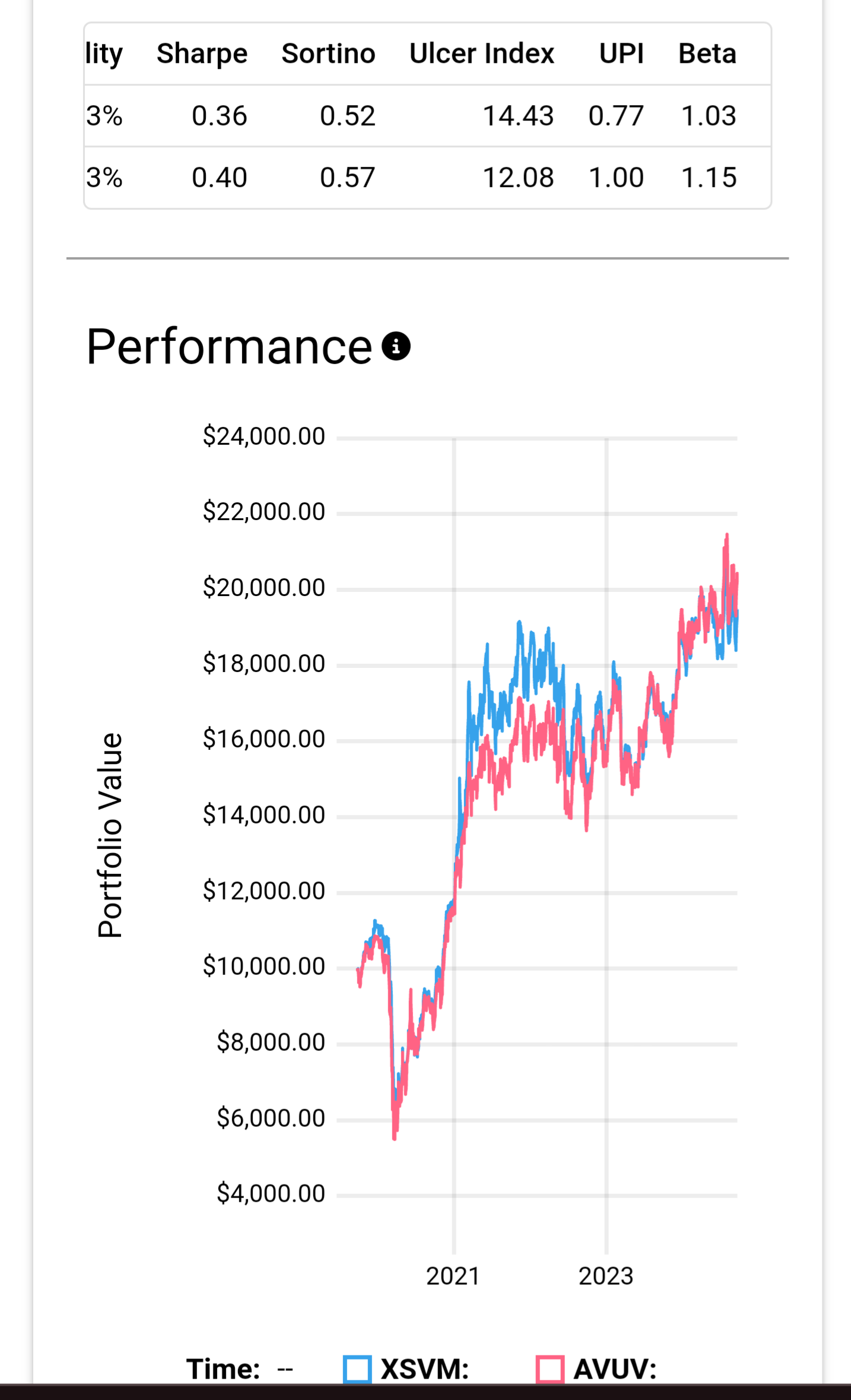

My recent test found that AVUV is not very good either. You can check out XSVM, which has similar or higher total factor loadings & alpha and AVUV, but only slightly higher long term returns and return to risk ratio than IWM.