Dear all,

Selling double down iron condors to collect premium seems like a good idea until it isn’t. Here is something interesting from Bloomberg.

Pls check out the article below just published today.

Regards

James

‘Captain Condor’ Wipeout Offers Harsh Lesson in Managing Risk

Takeaways by Bloomberg AI

-

David Chau, a 32-year-old day trader, and his followers lost tens of millions on Christmas Eve due to the Martingale strategy.

-

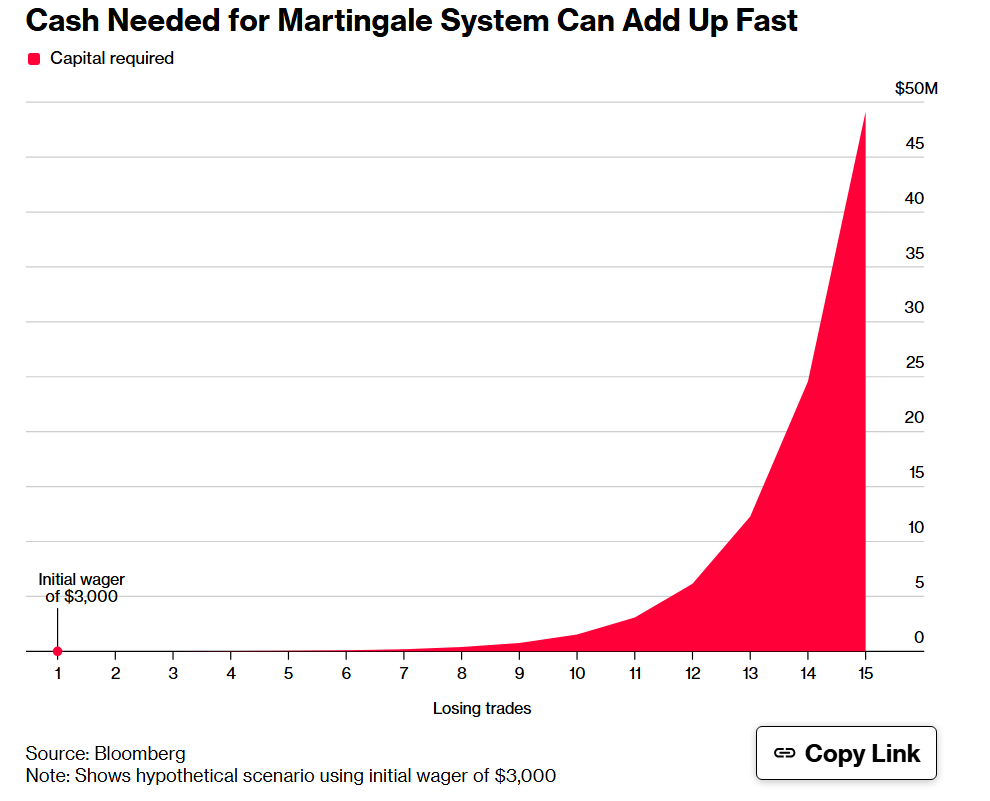

The Martingale strategy, which involves doubling the size of bets each time it loses, caused the size of the trade to balloon in a market with low liquidity.

-

Chau's losses were a result of selling iron condors, a trade that appears on a chart like the wings of a raptor, and doubling down on the position size each time the S&P 500 had a bigger move.

It wasn’t some YOLO trade that took down a successful options trader over Christmas, but a centuries-old gambling strategy popular with amateur blackjack players.

David Chau, a 32-year-old day trader, and his followers lost tens of millions on Christmas Eve in a blowup that exposed the perils of the Martingale strategy, which appears in the memoirs of notorious Venetian romantic Giacomo Casanova. The money was his own, capital entrusted to his hedge fund SPX MGMT, and that of a band of small-time investors paying $5,500 a year to have access to his trading plans.

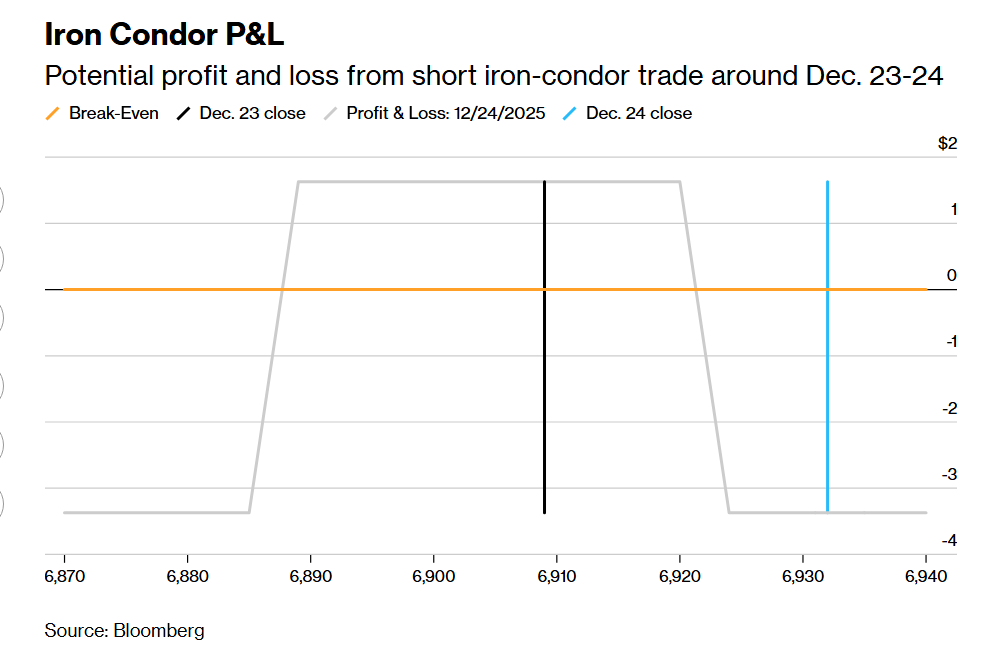

Chau is better known in the S&P 500 Index options market by the moniker “Captain Condor,” a reference to his trade of choice — the “iron condor” — that appears on a chart like the wings of a raptor. The trade itself — buying or selling a call spread above the current market and a put spread below it — is a relatively modest bet on whether or not a market will stay within a range. It’s become popular with retail trading sites, with sales of iron condors touted as a way to collect premium if markets stay rangebound.

Options commentators say that used correctly, condors can be a useful trading tool. But the Martingale strategy of doubling down, borrowed from casinos, caused the size of the trade to balloon in a market where many traders had already gone offline for Christmas. S&P 500 Index options volumes were their second lowest of the year on Christmas Eve, with only Black Friday on Nov. 28 being quieter.

“This was just a trade that was so large and the timing of it poorly chosen,” said Jason Coogan, a trader in the Cboe Options Exchange S&P 500 pit. “During the holidays there are less traders working and less liquidity in the market in general.”

The group had repeatedly sold iron condors over several days, betting the S&P 500 would remain in a tight range, and doubling up the position size each time when the index had a bigger move. By Dec. 23, the position in condors expiring the next day was up to some 90,000 contracts. The US options market is one of the world’s most transparent. Exchange-traded positions are visible to market participants, so the strategy’s vulnerability to a sizable loss was noticed even before it occurred.

The call and put spread strikes were only 5 points apart — the move on Dec. 24 that sunk the trade was only 0.3%, hardly a spectacular swing. Selling the 6890/6885 put spread and the 6920/6925 call spread netted about $13 million in premium, and inflicted the maximum net loss, about $32 million, according to Bloomberg calculations. Chau appears to have paused his trading activity since Christmas Eve.

“The problem is when you’re doubling things it gets unbearably huge,” said Matthew Amberson, founder and CEO of Option Research & Technology Services.

Some options pros even speculate that market makers deliberately “pushed” the S&P 500 by taking a long position in stocks or futures to deliberately wipe out Chau and his followers.

“During times like these, there is a greater chance for market manipulation,” said Coogan. “Not in a devious way: The world knew about this position.”

With less liquidity over the holidays, “everyone on the other side of it was able to have more influence over where they could push the market in the short term,” said Coogan.

Other participants dismissed the possibility that anyone can push around the S&P 500, given the depth and complexity of the market.

In any event, it’s the Martingale technique — which involves doubling the size of bets each time it loses — that led to Chau’s catastrophic losses on Christmas Eve.

In a sense, the Martingale strategy destroys the statistical-arbitrage nature of systematic trading by turning many small edges into a single path-dependent gamble. Modern risk management tends to work in reverse: it cuts exposure during losses, controls tail risk and preserves capital, to let incremental trading advantages compound over time. Without these safeguards, what looks like steady income is just leveraged speculation.

“Martingale isn’t a source of edge — it’s a way to turn frequent small gains into rare catastrophic losses,” said Jason Trost, founder and chief executive of Smarkets, a sports prediction market. “You’re doubling risk to earn a capped payoff, and in real markets you hit capital, margin, or liquidity limits long before the math ‘rescues’ you.”

Zero-day and other short-term options trading has exploded in popularity since the Covid pandemic, driving overall options volumes to a record each of the past six years. Option-selling strategies, especially on near-term contracts, has been credited with dampening stock-market volatility.

Read more: Popular Zero-Day Option Strategies Keep Lid on Stock Rallies

Chau expressed remorse for the collapse of his portfolio. “I do feel guilty for what occurred, but at the same time feel optimistic that there is room for improvement,” he wrote in an emailed statement.

“I use a probability based approach and although I understood this was a possible outcome, this issue did not exist for this specific model over the last 3 years,” he said. “I already identified what had occurred and I’m actively patching and updating the model.”

Captain Condor’s blowup, previously reported by Marketwatch, underscores the risks from option-selling strategies — where gains are limited and potential losses are far larger — and echoes huge losses from the past. Back in November 2018, a slump in oil and spike in natural gas caused millions of dollars in losses for clients of James Cordier, whose firm Optionsellers.com touted selling options on commodity futures contracts.

The firm’s customers — many of whom were retirees — were wiped out. Cordier posted a mea culpa video to YouTube that went viral, apologizing to individual clients and lamenting the “rogue wave” that “capsized our boat.” He has since made a comeback, releasing a book in 2024.

Casanova also came unstuck doubling up every time he lost.

According to his memoirs, his luck ran out following a winning streak playing the Martingale technique during the Carnevale in Venice and he lost all his money. He ended up selling his lover’s diamonds, dashing their hopes of running away together.

The Captain Condor saga highlights to Amberson a basic difference between investing and gambling.

“If you have a losing streak, you have a losing streak, but you don’t try to make it all back in one,” he said. “That’s a gambler’s fallacy.”

— With assistance from Matt Turner and Christian Dass