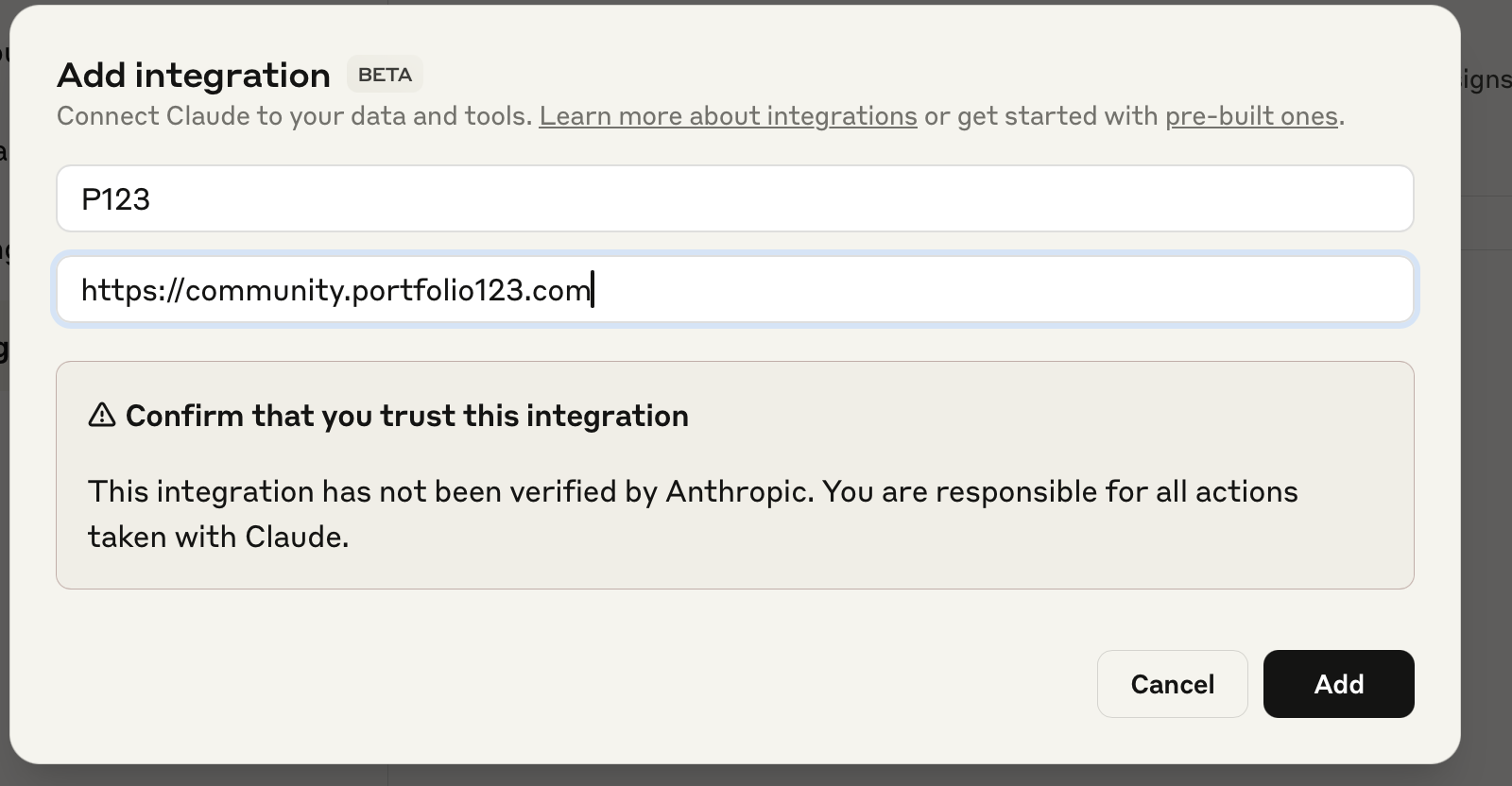

Using integrations you can "integrate" GitHub for example and add additional URL sites like P123's forum:

I just added both (GitHub and P123) and am beginning to explore this. It can be turned on or off easily. I would be interesting in whether others find this useful.

Also I'm not sure if P123 would find something similar to be helpful for integrating AI into its platform but it may be worth taking a look— perhaps integrating additional data beyond the forum. Anthropic considers Claude 4 Opus the best coding LLM (this week) which does not come as a surprise. But maybe there is something useful here.

Make sure to turn on Research if you use integrations in Claude 4.

I asked Claude Sonnet this:

What are some ideas for stock features in machine learing. Feel free to use the portfoliio123. com integration.

Then this:

Okay using the forum integration focus on suggestions by @yuvaltaylor

This seems positive and not something P123 would mind having as the result of a search on its site. I leave it to Yuval to determine if it is too brief of a summary, not accurate or not current. Also, I think a newby might need to ask the LLM about specific factors that belong in a ranking system. It remains to be seen if Claude 4 can search with that kind of depth. But ChatGPT can search the P123 forum too and I have not seen it go into this kind of depth. So maybe this is something we can use at home for now. Anyway this was the final Claude 4 Sonnet output:

Stock Features for Machine Learning: @yuvaltaylor's Portfolio123 Insights

@yuvaltaylor's approach to stock features for machine learning at Portfolio123 represents a sophisticated blend of fundamental analysis and quantitative rigor, drawing from his role as Product Manager at Portfolio123 and personal 44% CAGR track record. His recommendations center on a seven-category framework that emphasizes multifactor ranking systems over single-factor approaches, making it particularly relevant for ML applications.

Yuval Taylor joined Portfolio123 as Product Manager after four years as a successful user, bringing deep expertise in microcap investments and strictly quantitative methodologies. His fundamental philosophy advocates for evaluating stocks "from every angle" using multiple factors simultaneously, which aligns perfectly with machine learning's ability to process numerous features concurrently.

@yuvaltaylor's seven-factor framework for ML models

Taylor's systematic approach organizes stock features into seven distinct categories, each addressing different aspects of stock performance prediction that machine learning models can effectively utilize.

Value factors form the foundation of his approach, with net free cash flow to market cap being particularly emphasized as equally productive as traditional value ratios. His value framework includes price-to-sales ratios, book-to-market ratios, and various price-to-earnings variants, providing ML models with comprehensive cheapness metrics.

Growth factors require careful consideration due to what Taylor calls "misbehaving factors." Sales growth deserves special attention, as extreme values often indicate unsustainability rather than opportunity. His growth framework includes earnings growth and margin changes, with specific warnings about interpreting extreme values in ML training data.

Stability factors represent a critical component often overlooked in traditional analysis. Taylor recommends low price volatility (standard deviation of daily/weekly returns), low volume volatility, and low share turnover as foundational stability measures. These factors help ML models identify consistent performers rather than volatile outliers.

Quality factors focus on financial statement integrity, with particular emphasis on M-Score for detecting financial manipulation. Taylor warns about the unreliability of financial data due to discretionary accounting practices, making quality factors essential for ML model robustness.

Sentiment factors incorporate market psychology through short interest levels and changes in analyst coverage. These factors provide ML models with insights into market sentiment that purely fundamental metrics might miss.

Momentum factors and size factors complete the framework, with Taylor noting that size factors (smaller stocks) have been particularly strong performers in post-pandemic markets, though he emphasizes that factor relationships can be disrupted during market regime changes.

Low-volatility model specifications

For ML models focused on low-volatility strategies, Taylor recommends six basic factors: low price volatility (standard deviation of returns), low volume volatility, beta correlation to market movements, low share turnover, alpha measurements, and risk-adjusted performance metrics. This focused approach makes it particularly suitable for ML implementations where feature selection is crucial.

Misbehaving factors and ML considerations

Taylor's concept of "misbehaving factors" is particularly relevant for machine learning applications. Change in profit margin often shows that middle values perform better than extremes, challenging traditional linear assumptions that ML models might make. Similarly, extreme sales growth values can indicate unsustainability, requiring careful feature engineering to capture these non-linear relationships.

Portfolio123's ML integration architecture

Portfolio123's AI Factors system represents a comprehensive ML framework that builds on Taylor's factor philosophy. The platform offers machine learning algorithms including XGBoost, Random Forest, and Neural Networks that can process hundreds of factors simultaneously, making Taylor's multi-factor approach practically implementable.

The AI Factors feature allows users to import features from existing ranking systems and supports sophisticated normalization options beyond cross-sectional normalizations. This technical infrastructure enables the practical application of Taylor's seven-factor framework within ML models.

Portfolio123's data foundation includes over 500 fundamental factors powered by FactSet data, providing institutional-grade quality with no survivorship or look-ahead bias. This extensive factor library supports Taylor's philosophy of comprehensive stock evaluation while maintaining the data integrity essential for ML model training.

Advanced ML implementation insights

The platform's hyperparameter grid search capabilities and automated model validation address Taylor's emphasis on avoiding overfitting and data mining. The AIFactor() function can be integrated throughout Portfolio123's ecosystem, enabling ML predictions in ranking systems, screens, and buy/sell rules.

Training infrastructure includes cloud-based processing with CPU/GPU options and queue management for high-demand periods, supporting the computational requirements of Taylor's comprehensive factor approach. The system implements proper data leakage prevention through training/validation period separation, addressing his concerns about robust backtesting.

Performance measurement and validation

Taylor's performance measurement philosophy emphasizes omega ratios over Sharpe ratios for risk-adjusted performance and recommends trimmed alpha as a more predictive performance measure. For ML applications, he suggests 9-12 year lookback periods for backtesting, with 25-year lookback periods for enhanced predictiveness.

His validation approach warns against data mining and over-optimization, recommending testing model robustness through stress testing and using more stocks in backtests than in final portfolios. These principles are particularly relevant for ML models, which can easily overfit to historical patterns.

Market regime considerations

Taylor's post-pandemic market insights highlight how traditional factor relationships have been disrupted, with riskiest stocks outperforming safe ones since 2020. This observation is crucial for ML models, as it suggests the need for dynamic retraining and regime-aware modeling approaches.

His documentation of lack of factor persistence over time supports the ML community's emphasis on regular model retraining, recommending focus on factors that "work well in general" rather than attempting to predict short-term factor performance.

Conclusion

@yuvaltaylor's approach to stock features for machine learning represents a sophisticated synthesis of fundamental analysis and quantitative rigor. His seven-factor framework provides a structured approach to feature selection that addresses the key challenges of ML model development: avoiding multicollinearity, handling non-linear relationships, and maintaining robustness across market regimes.

The Portfolio123 platform's AI Factors system successfully implements Taylor's philosophical approach within a practical ML framework, offering the computational infrastructure and data quality necessary for sophisticated quantitative strategies. His emphasis on comprehensive factor evaluation, careful validation, and regime awareness provides valuable guidance for practitioners developing ML-based stock selection models.

The combination of Taylor's theoretical framework and Portfolio123's technical capabilities creates a compelling approach to machine learning in quantitative finance, emphasizing both the art of factor selection and the science of model validation.