Hi all,

I've been playing around with ways to test the hypothesis that companies that pay less (or more) tax outperform companies that pay more (or less), given the same level of profitability.

The way I approached this was to create 5 universes out of the Easy to Trade Universe as follows.

Frank("NetIncBXorTTM / asttotttm") >= 80

IncTaxExpTTM/ asttotttm

Basically, this looks at the 20% of companies with the highest net income relative to their assets and excludes companies for which income tax to assets is unavailable.

Then I would do the same for the next 20% of companies as follows.

Frank("NetIncBXorTTM / asttotttm") < 80

Frank("NetIncBXorTTM / asttotttm") >= 60

IncTaxExpTTM/ asttotttm

And similarly for the other 3 subuniverses.

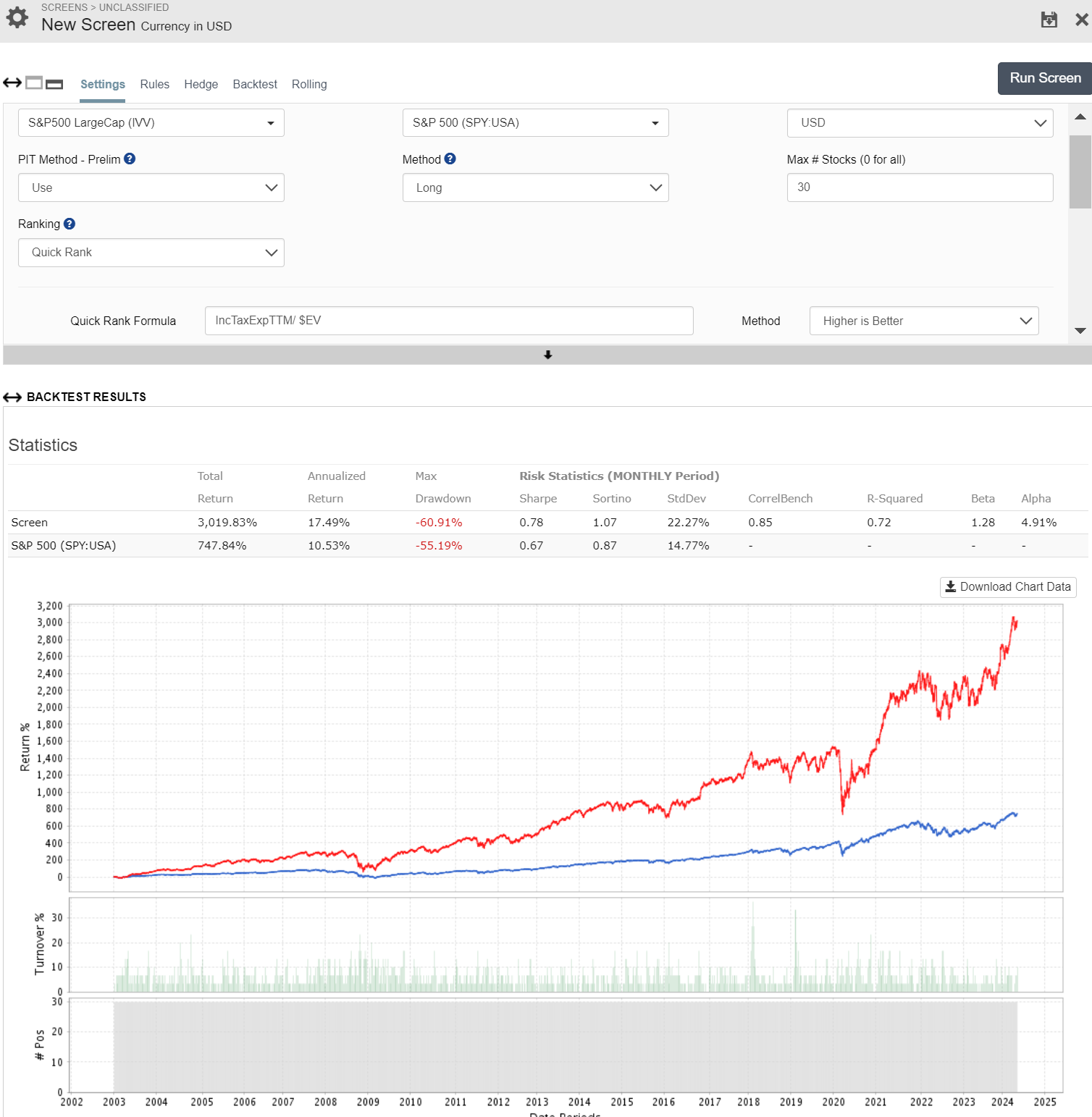

I then rank the companies in each subuniverse by IncTaxExpTTM/ asttotttm against companies in the same industry, lower is better. Hence, favouring companies that pay little tax relative to their peers.

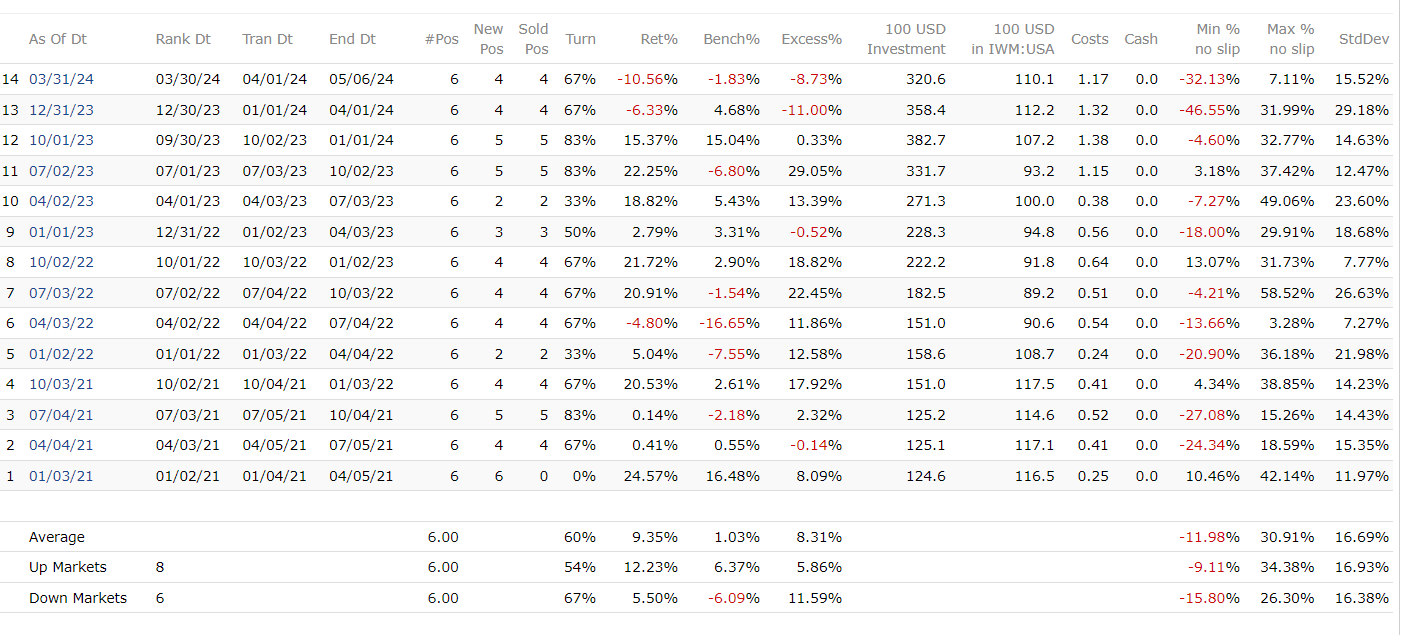

For example, for companies in the subuniverse with the highest net income to assets, I found the following:

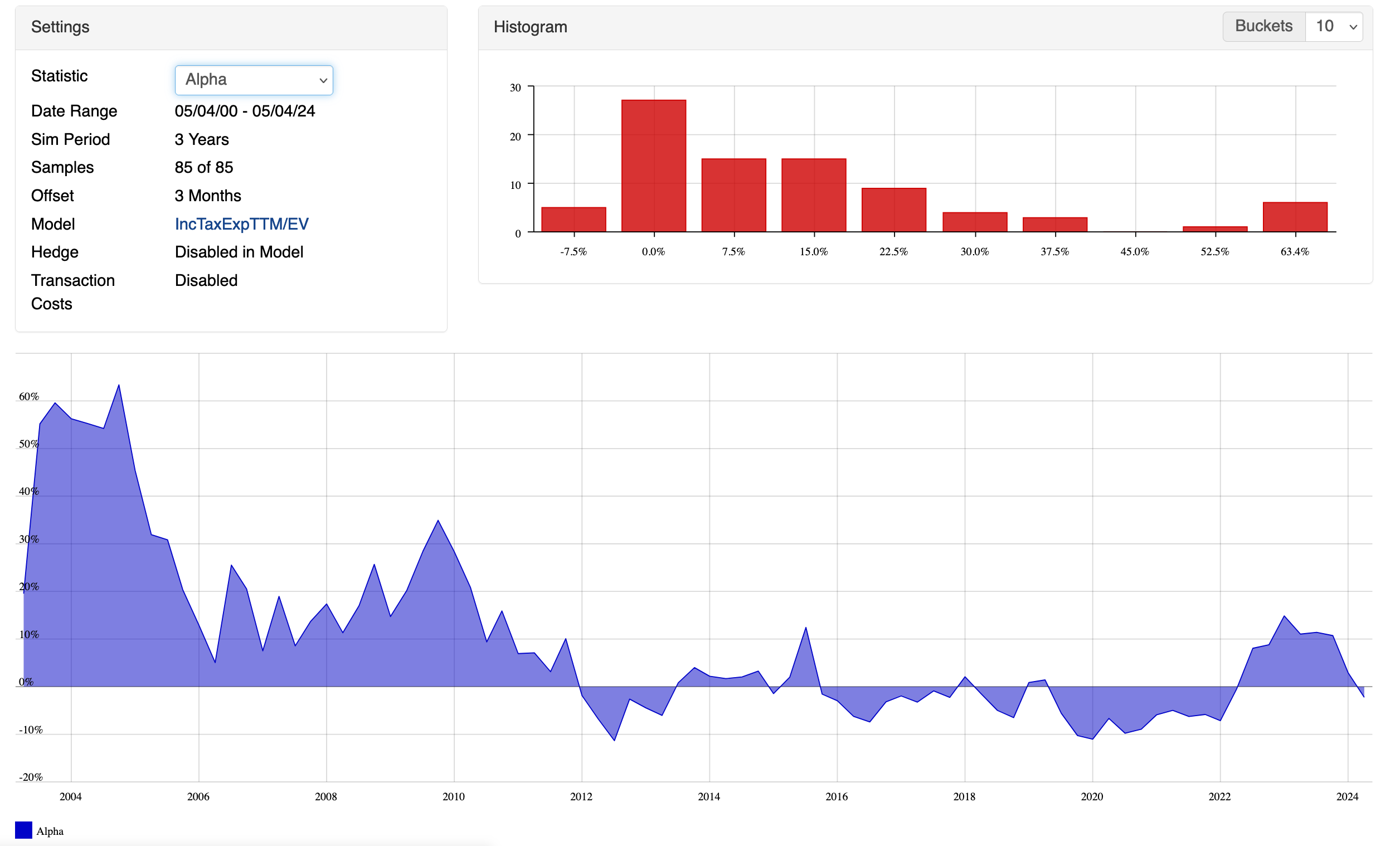

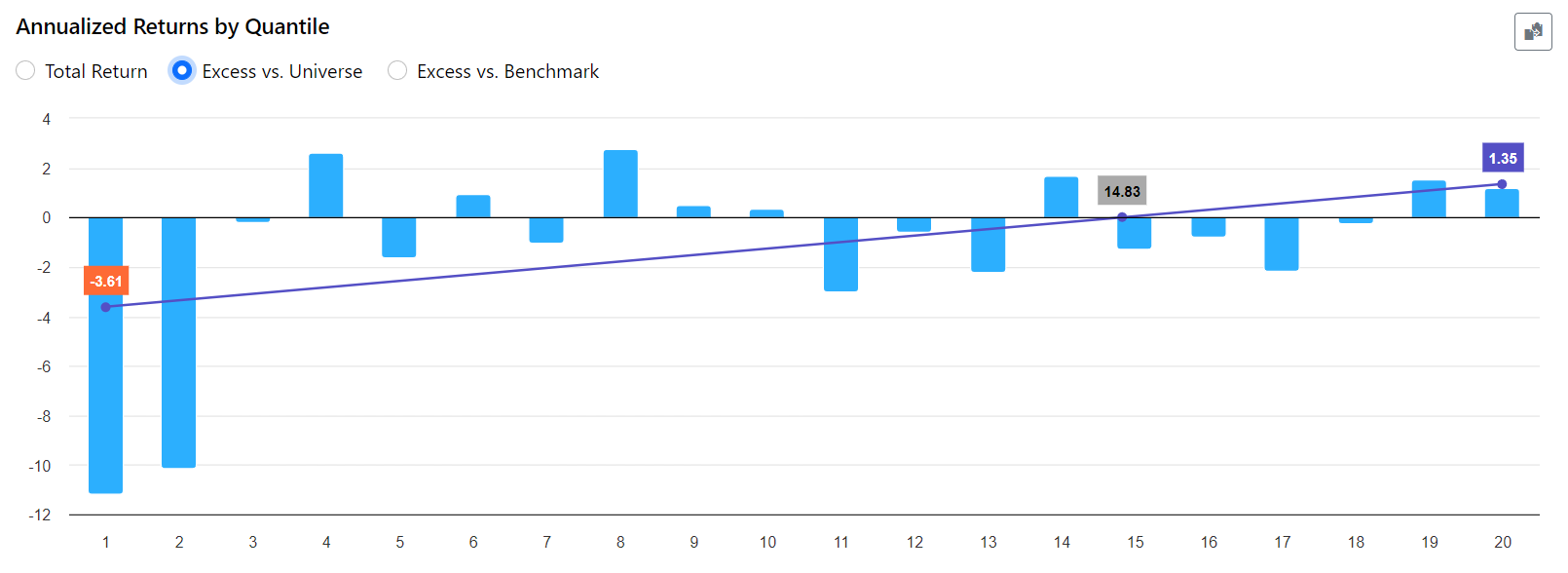

For the second highest, I found this:

This would indeed seem to validate that companies that pay high taxes given their profits should probably be avoided.

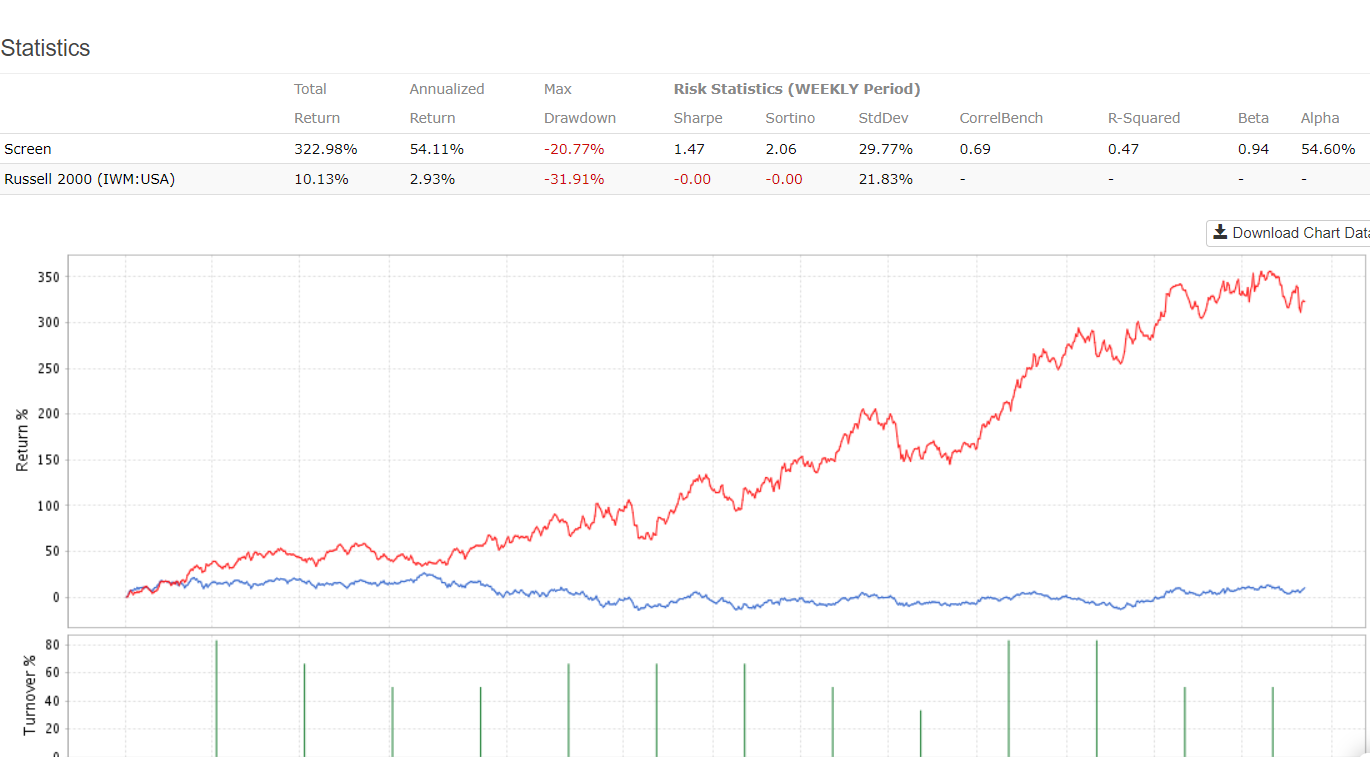

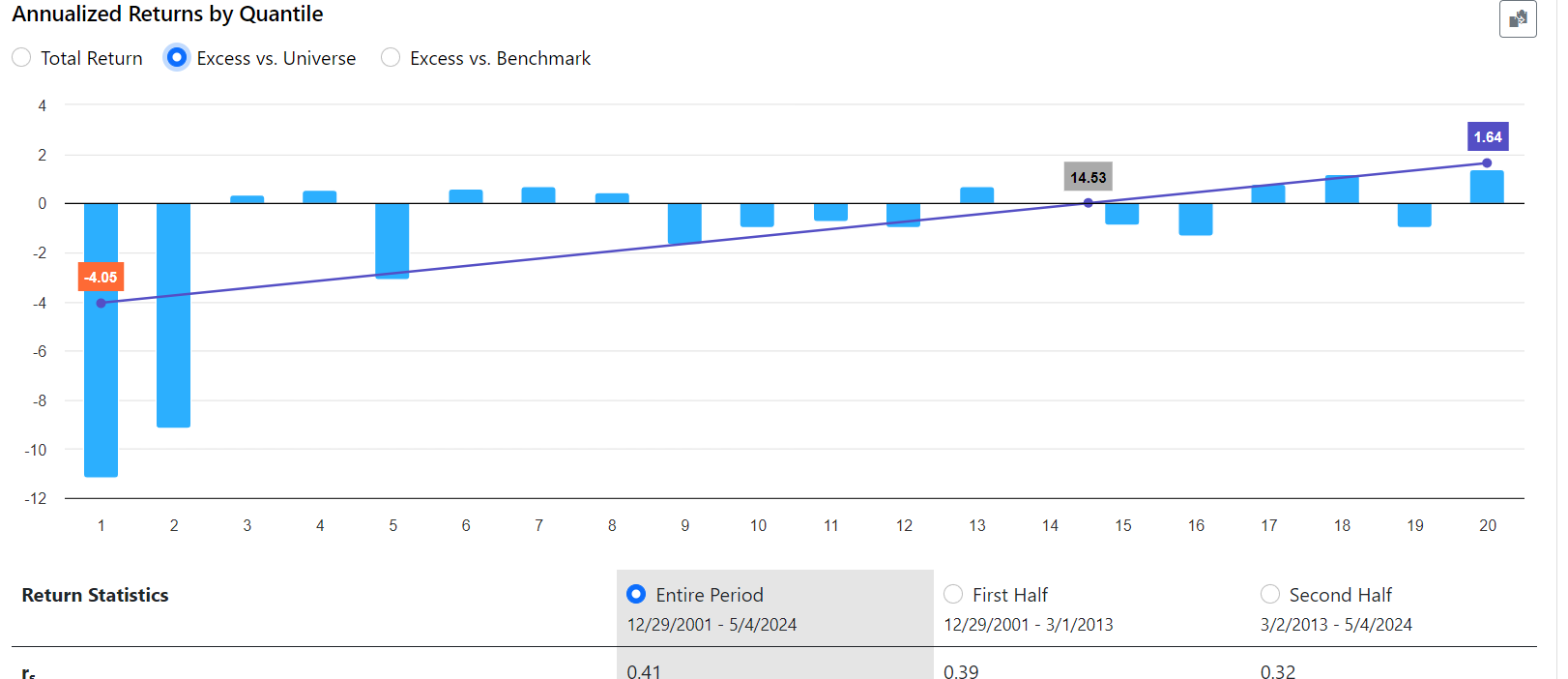

However, flipping the factor to higher is better (and actually favouring companies that pay high tax relative to their peers with similar profits), I obtain this for the top quantile:

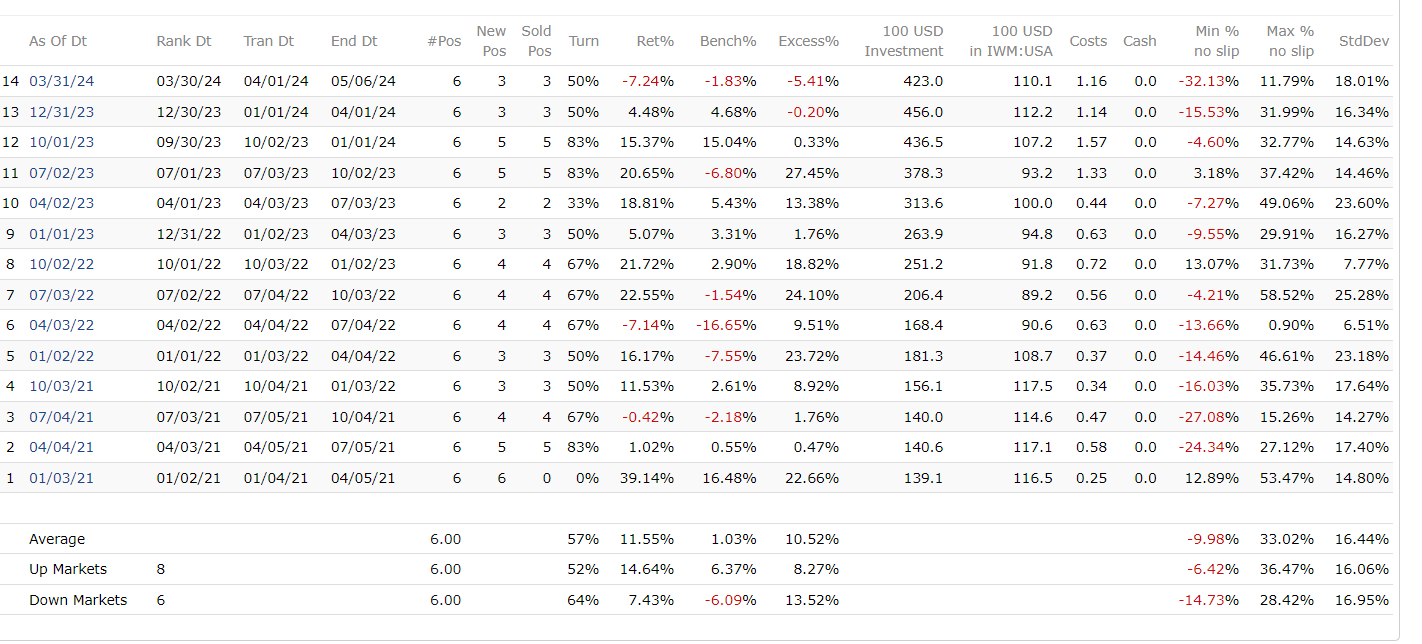

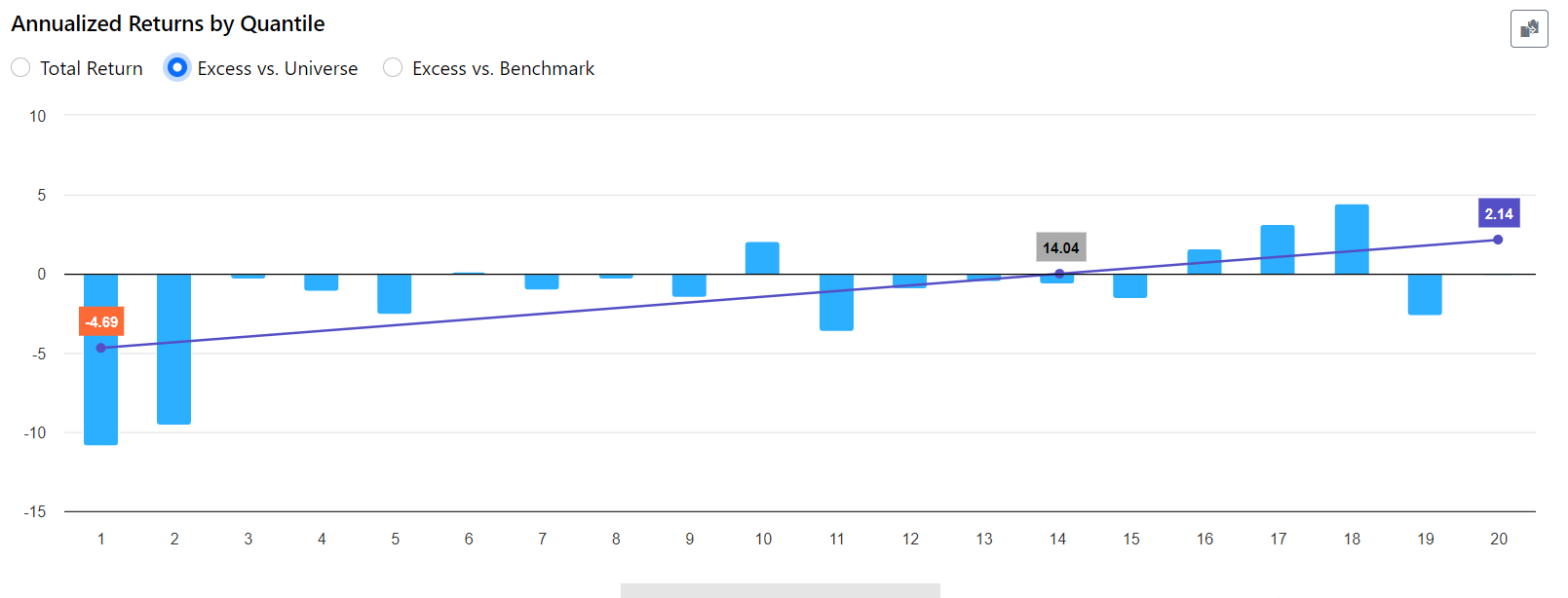

and this for the second highest quantile:

... which would actually be more of a validation of the contrary.

This leads me to two questions:

- First of all, why does this happen and what do I make of this?

- Secondly, what would be a 'better' way to test this idea?

Best,

Victor