TL;DR:

If you form a group, each individual gets to the best solution— MUCH faster than they could by themselves--using the best algorithm available. What more could you ask for?

Background:

Historically, these are called multi-armed bandit problems—think of a row of slot machines (“arms”), each with a different (unknown) payout frequency. You have 500 pulls and keep what you win. Your goal is simple: make the most money possible. To do that, you want to find and pull the arm that pays out best as often as possible—but you need to experiment a bit to discover which one that is.

Thompson Sampling is a proven optimal algorithm for solving this kind of problem: it explores to learn, then exploits to maximize rewards. In real life, Amazon and other companies use similar algorithms for things like testing which web page or ad works best, by showing different users different options and counting “successes.”

For trading, you might use this to find the best trading algo or strategy (e.g., best fill rates)—the idea is exactly the same.

How to use this code:

- Set the true_success_rates list to whatever probabilities you want (these are the hidden win rates).

- Run the code (no seed, so you can see different results each time).

- See how quickly the algorithm finds and sticks to the best arm—visualized and in stats.

Enjoy!

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

# Configuration

true_success_rates = [0.10, 0.25, 0.15, 0.40] # True success probabilities

n_arms = len(true_success_rates)

n_rounds = 500

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

# Set random seed for reproducibility

#np.random.seed(42)

# Set style for prettier plots

plt.style.use('seaborn-v0_8-darkgrid')

sns.set_palette("husl")

# Set random seed for reproducibility

#np.random.seed(42)

# Configuration

true_success_rates = [0.10, 0.25, 0.15, 0.40] # True success probabilities

n_arms = len(true_success_rates)

n_rounds = 500

# Color scheme

colors = plt.cm.viridis(np.linspace(0, 0.9, n_arms))

optimal_arm = np.argmax(true_success_rates)

# Track successes and failures for each arm

successes = np.zeros(n_arms)

failures = np.zeros(n_arms)

# Track choices and rewards

arm_history = []

rewards = []

cumulative_rewards = []

# Run Thompson Sampling

for i in range(n_rounds):

# For each arm, sample a probability from its Beta distribution

sampled_probs = [np.random.beta(successes[j] + 1, failures[j] + 1)

for j in range(n_arms)]

# Choose the arm with the highest sampled probability

chosen_arm = np.argmax(sampled_probs)

arm_history.append(chosen_arm)

# Simulate pulling the arm

reward = np.random.rand() < true_success_rates[chosen_arm]

rewards.append(reward)

cumulative_rewards.append(sum(rewards))

# Update successes or failures

if reward:

successes[chosen_arm] += 1

else:

failures[chosen_arm] += 1

# Calculate final statistics

arm_counts = np.bincount(arm_history, minlength=n_arms)

estimated_rates = successes / (successes + failures)

# Create figure with subplots

fig = plt.figure(figsize=(14, 8))

gs = fig.add_gridspec(2, 2, hspace=0.3, wspace=0.3, height_ratios=[1.5, 1])

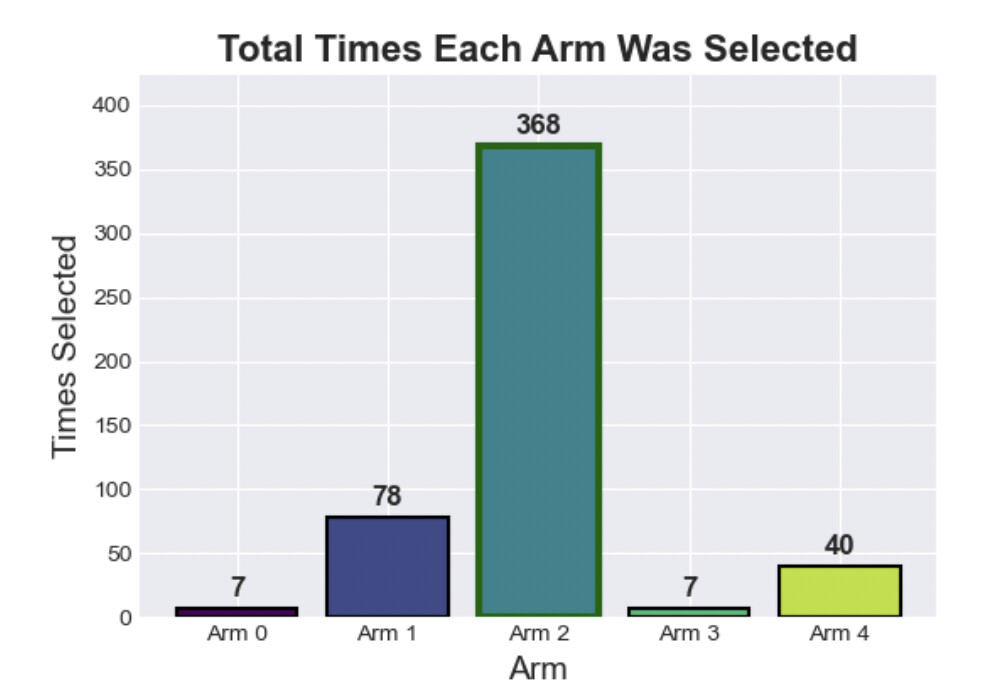

# 2. Total arm selection frequency (top right)

ax2 = fig.add_subplot(gs[0, 1])

bars = ax2.bar(range(n_arms), arm_counts, color=colors, edgecolor='black', linewidth=1.5)

# Highlight the optimal arm

bars[optimal_arm].set_edgecolor('darkgreen')

bars[optimal_arm].set_linewidth(3)

# Add value labels on bars

for i, (count, bar) in enumerate(zip(arm_counts, bars)):

height = bar.get_height()

ax2.text(bar.get_x() + bar.get_width()/2., height + 5,

f'{count}', ha='center', va='bottom', fontsize=12, fontweight='bold')

ax2.set_xlabel('Arm', fontsize=14)

ax2.set_ylabel('Times Selected', fontsize=14)

ax2.set_title('Total Times Each Arm Was Selected', fontsize=16, fontweight='bold')

ax2.set_xticks(range(n_arms))

ax2.set_xticklabels([f'Arm {i}' for i in range(n_arms)])

ax2.set_ylim(0, max(arm_counts) * 1.15)

# 2. Summary statistics table (bottom)

ax3 = fig.add_subplot(gs[1, 0])

ax3.axis('tight')

ax3.axis('off')

# Create table data

table_data = []

headers = ['Arm', 'Times Pulled', 'True Success Rate']

for i in range(n_arms):

row = [

f'Arm {i}',

f'{arm_counts[i]}',

f'{true_success_rates[i]:.3f}'

]

table_data.append(row)

# Create table

table = ax3.table(cellText=table_data, colLabels=headers,

cellLoc='center', loc='center',

colWidths=[0.3, 0.35, 0.35])

# Style the table

table.auto_set_font_size(False)

table.set_fontsize(12)

table.scale(1.2, 1.8)

# Color code the cells

for i in range(n_arms):

# Color the arm column

table[(i+1, 0)].set_facecolor(colors[i])

table[(i+1, 0)].set_text_props(weight='bold')

# Highlight the row of the optimal arm

if i == optimal_arm:

for j in range(3):

table[(i+1, j)].set_facecolor('#90EE90') # Light green

table[(i+1, j)].set_text_props(weight='bold')

# Style header row

for j in range(3):

table[(0, j)].set_facecolor('#4472C4')

table[(0, j)].set_text_props(weight='bold', color='white')

ax3.set_title('Summary Statistics After 500 Trials', fontsize=16, fontweight='bold', pad=20)

# Add main title and key insight

plt.suptitle('Thompson Sampling: Learning Which Arm is Best', fontsize=20, fontweight='bold')

# Add text box with key insight

textstr = f'Key Insight: Thompson Sampling quickly identified and focused on Arm {optimal_arm} (40% success rate)\nwhile still exploring other options. It pulled the best arm {arm_counts[optimal_arm]} times out of {n_rounds}!'

props = dict(boxstyle='round', facecolor='wheat', alpha=0.8)

fig.text(0.5, 0.02, textstr, transform=fig.transFigure, fontsize=14,

horizontalalignment='center', bbox=props)

plt.tight_layout()

plt.show()

# Print simple summary

print("\n" + "="*50)

print("THOMPSON SAMPLING RESULTS")

print("="*50)

print(f"\nAfter {n_rounds} trials:")

print(f"- Best arm (Arm {optimal_arm}) was pulled {arm_counts[optimal_arm]} times ({arm_counts[optimal_arm]/n_rounds*100:.1f}%)")

print(f"- Algorithm achieved {sum(rewards)} total rewards")

print(f"- Average reward per pull: {np.mean(rewards):.3f}")

print(f"- Optimal average would be: {max(true_success_rates):.3f}")

# Calculate what random selection would have achieved

random_expected_reward = np.mean(true_success_rates)

random_total_expected = random_expected_reward * n_rounds

print(f"\nComparison with random selection:")

print(f"- Random would pull each arm ~{n_rounds/n_arms:.0f} times")

print(f"- Random expected total rewards: {random_total_expected:.0f}")

print(f"- Random expected average reward: {random_expected_reward:.3f}")

print(f"- Thompson Sampling improvement: {(sum(rewards)/random_total_expected - 1)*100:.1f}% better!")

print("\nThe algorithm successfully learned which arm was best!")

Key takeaways:

- Thompson Sampling finds and focuses on the best option with remarkable speed and efficiency, while still checking the others occasionally.

- The plots and stats show, at a glance, how well it works.