According to this article from Alpha Architect, both stop loss and stop profit is a bad thing, comparing to buy & hold or regular rebalancing.

It also ties into whether there is autocorrelation of returns which was discusses in another thread. This article might suggest there is not much correlation of returns either way–except possible in certain market downturns.

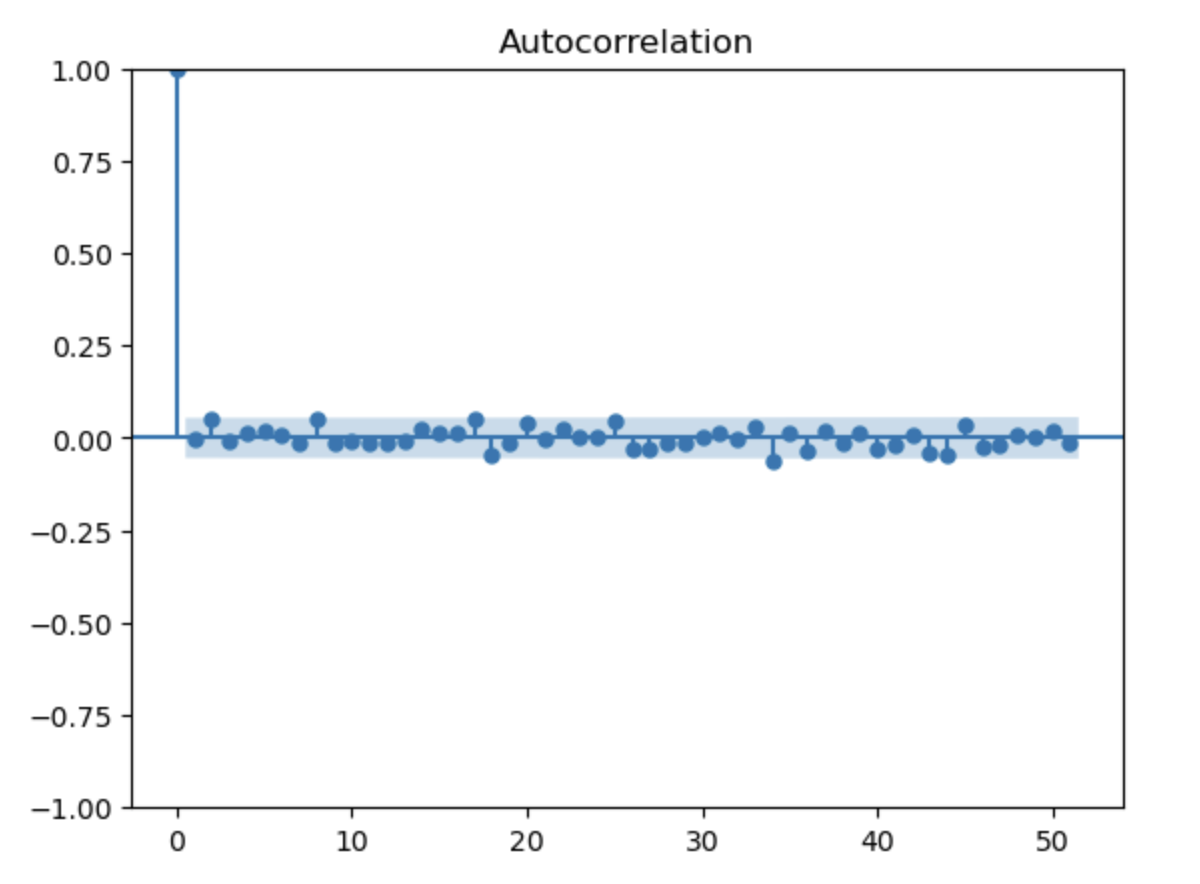

FWIW, I don’t find much autocorrelation of returns—even for my port and not for large-cap sector ETFs like the SPDRs either. If an aggregation of large-cap stocks in the same sector does not have autocorrelation (check this for yourselves), it argues for an efficient market, at least, and possibly suggests a low return using momentum strategies for large-caps.

Not surprising that the individual stocks in this study did not show autocorrelation, I think.

Here is the code where people can test this for themselves:

Here is an example, for my port I think but I forget what I uploaded with the code above (‘TimeLag.csv’) Being outside of the shaded area would suggest statistical significance for each lag period: