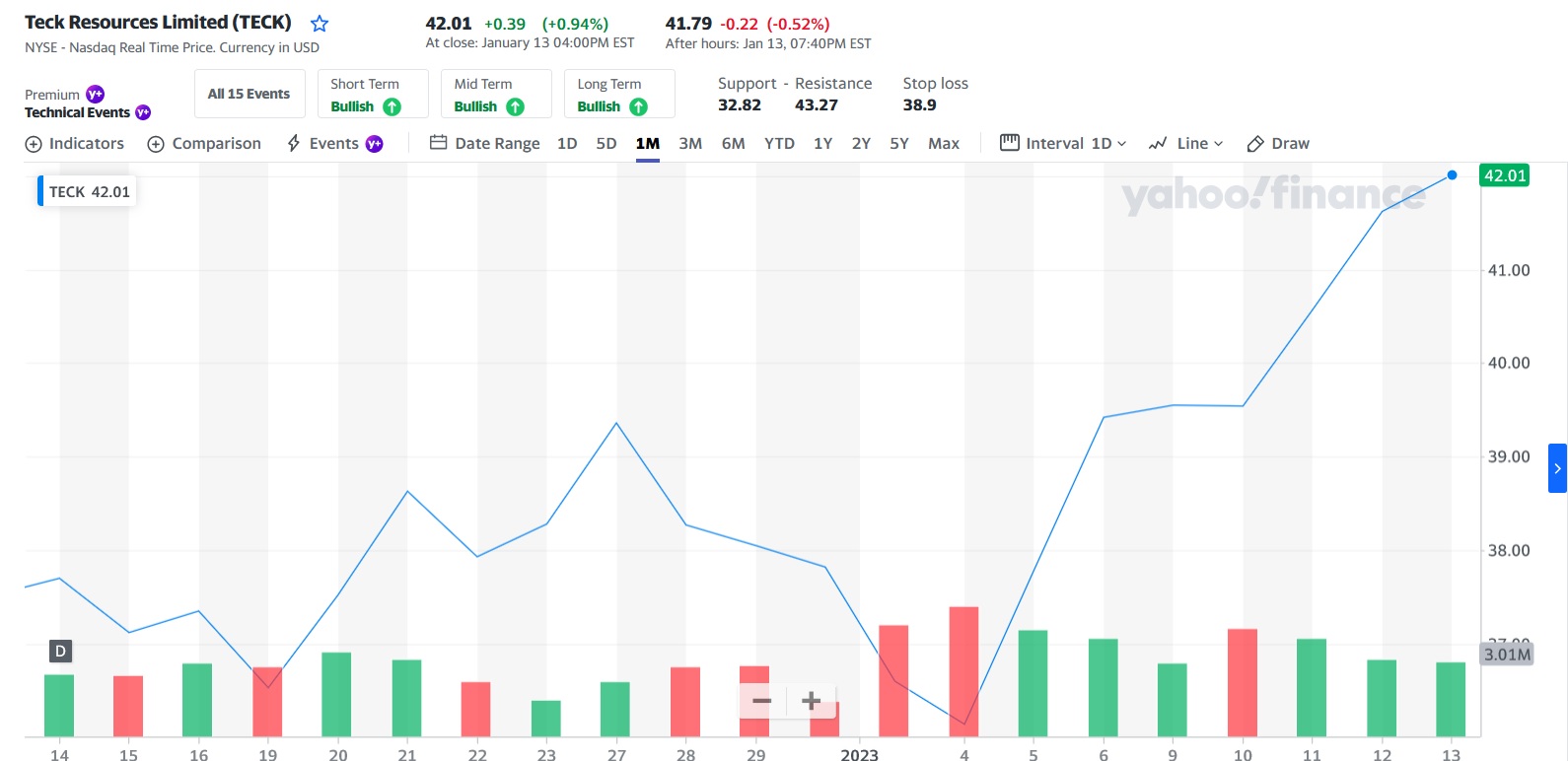

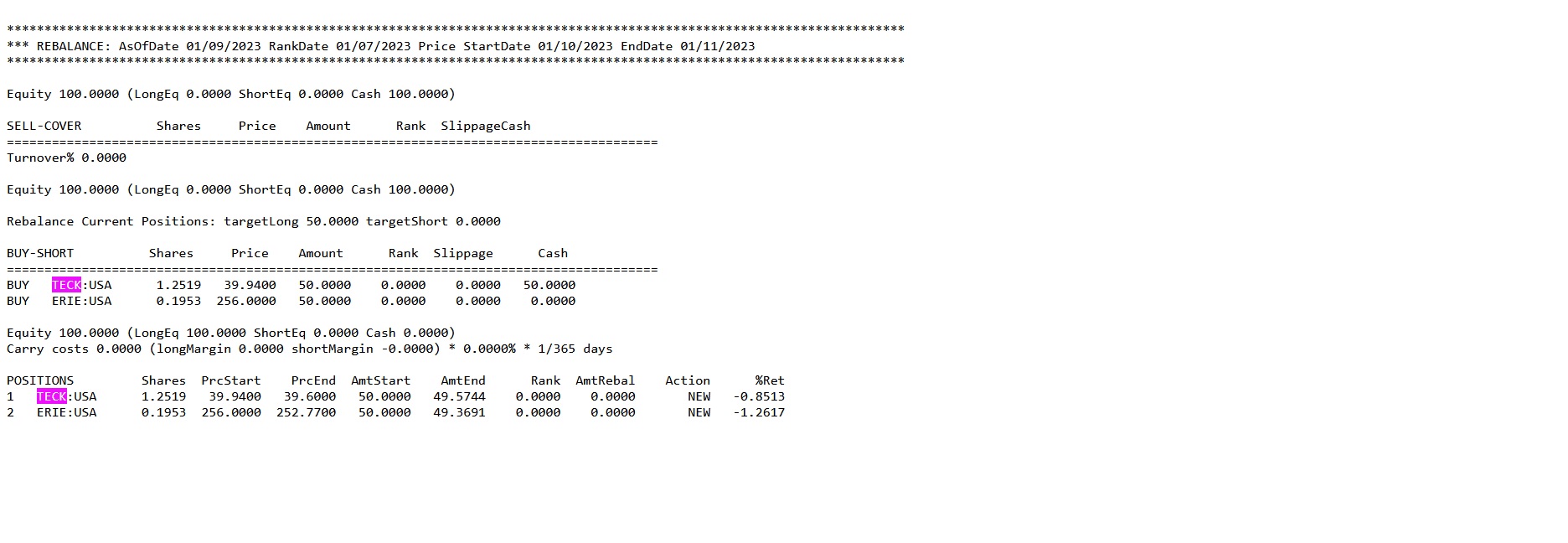

Here’s a simple screen which buys a stock after 5 down days followed by 3 up days.

It seems to me the backtest is buying on the day the criteria are satisfied . Shouldn’t it be buying at the next open after the criteria pass? log and chart attached

// last 3 days up and previous 5 days down

LoopSum(“Close(CTR)>Close(CTR+1)”,3)>=3

LoopSum(“Close(CTR+3)<Close(CTR+4)”,5)>=5

Here’s a simple screen which buys a stock after 5 down days followed by 3 up days.

It seems to me the backtest is buying on the day the criteria are satisfied . Shouldn’t it be buying at the next open after the criteria pass? log and chart attached

// last 3 days up and previous 5 days down

LoopSum(“Close(CTR)>Close(CTR+1)”,3)>=3

LoopSum(“Close(CTR+3)<Close(CTR+4)”,5)>=5