Let's say a company issues an interim earnings report and FactSet simply ignores it. In that case, there's no way for Portfolio123 to know about it, and no way for the report to be mentioned anywhere in the system.

On the other hand, let's say a company issues an interim earnings report and FactSet takes four weeks to process it. As soon as the report is issued and FactSet records that fact in its database (which is usually very quickly), Portfolio123 gives the stock a StaleStmt = 1 until the report is processed.

DaysLate is quite different. This is populated when it has been a certain number of days since the latest (FactSet-acknowledged) earnings report. So you will see some companies who have issued reports but whose reports have been ignored by FactSet with DaysLate > 0. However, DaysLate was designed for US stocks and really shouldn't be used for European stocks.

If you want to avoid stocks whose data FactSet has not yet processed, use StaleStmt = 0 in your buy rules or universe rules. But there's no way to automatically avoid stocks whose earnings releases FactSet missed altogether.

However to finish this discussion I would like to show an interesting case that faster processing is possible (though this is a case for domestic market).

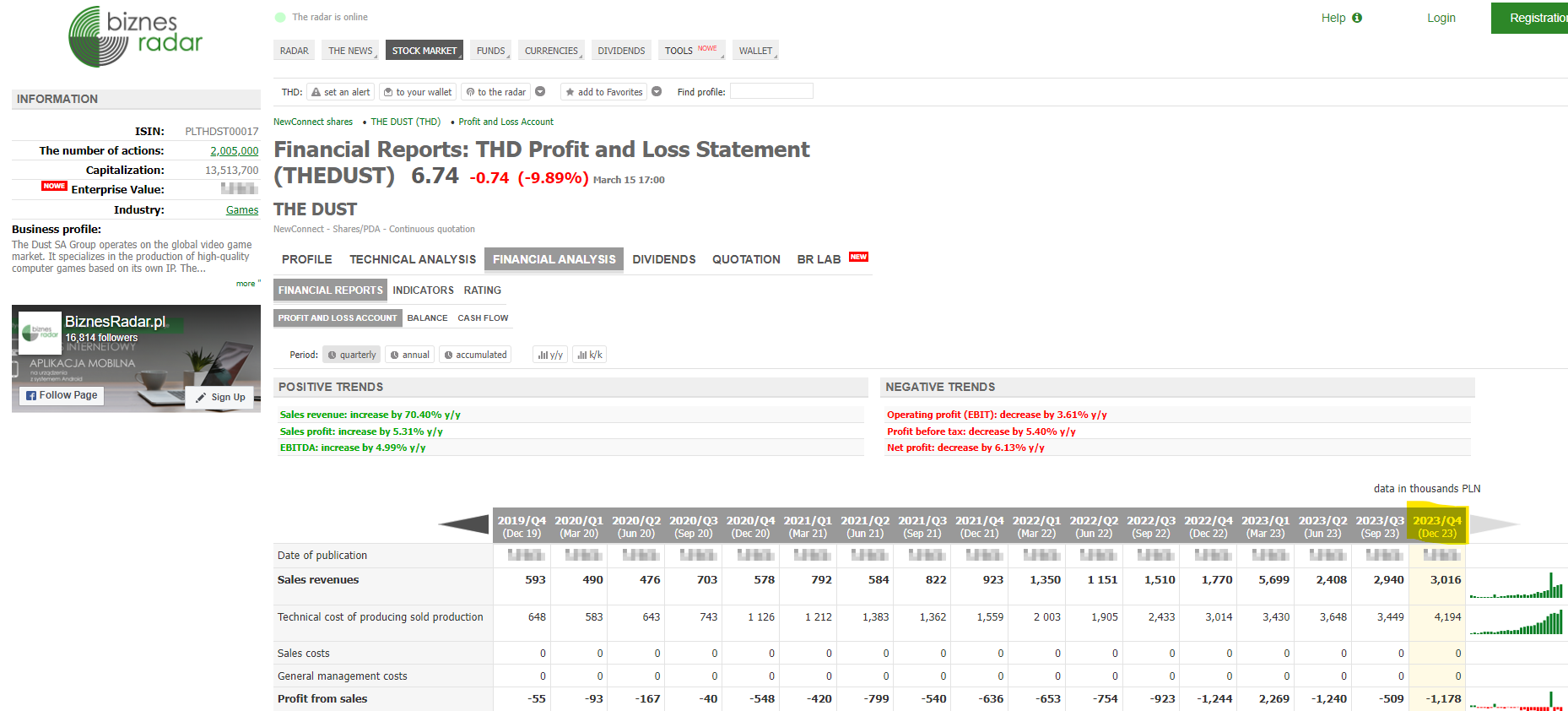

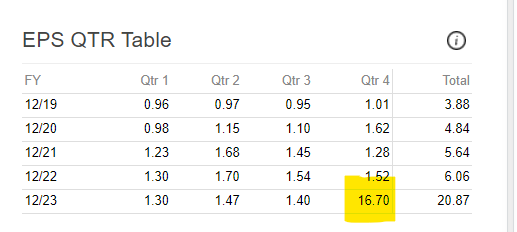

Super tiny Polish stock: The Dust SA , THD:POL, $3m mktcap,

How is FactSet processing ... lets see...the last figures in P123 are for Q2 2023, the stock published Q4 2023 earnings on 14 March 2024.

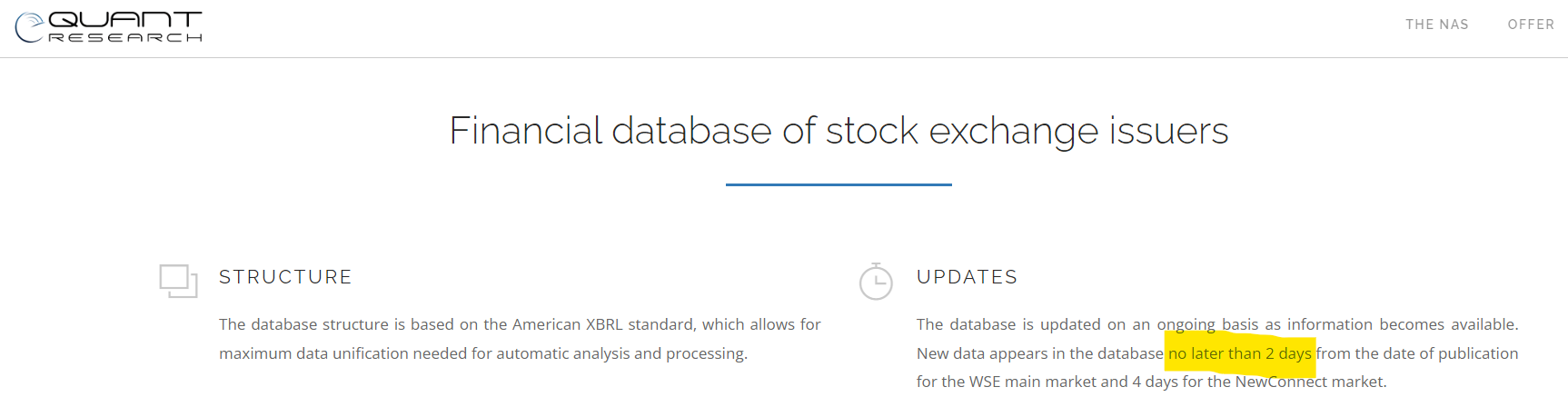

Is it possible to process fundamentals faster ? Yes it is.

There is a data provider who process fundamentals for Polish stocks in max 2 days:

!(PeriodDateQ<PeriodDateA) can be used to avoid investing in stocks where FactSet ignored the Q4 results. It looks like that the most common report they ignore is the Q4 when it's embedded in the annual report.

Got two stocks that released Q1 reports 10 days ago but the reports are not registered with FactSet (MTHH:DNK and B2I:NOR).

Both is indicating that the report is late in P123 (DaysLate>0). And both has Actuals that are quite fresh.

So one way to find these two companies could have been to use the formula LatestActualDays<DaysLate

Since we can assume that the Actuals contains information about the quarterly report and we can assume that the market know more than us, we could chose to listen to the market and sell the stock if the market reacted negatively to whatever was said in the Actuals. Could use a sell rule like this -

LatestActualDays<DaysLate and Ret%Chg(5)<0

In this case both holdings are actually showing StaleStmt=1, so we could again chose to listen to the market and sell the stock if the market reacted negatively to whatever was said in the report in a similar manner like -

StaleStmt=1 and Ret%Chg(5)<0

If anyone has any other ideas to how to deal with the fact that FactSet is not always very timely, please share your ideas.

For polish stock, flag LatestActualDays is very often N/A and, in addition, I do not trust this flag. Maybe for Swedish market this flag works better.

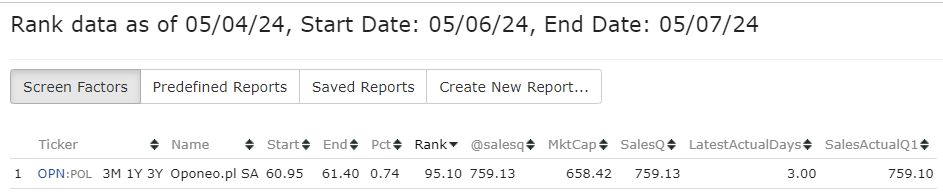

For example, OPN:POL, the Q3 sales in 323.47 and Q4 sales is 759.10. The Q4 report was published on 29/04/2024.

Based on the example below, between these two days LatestActualDays flag was N/A.

Then, LatestActualDays showed reported sales (SalesQ).

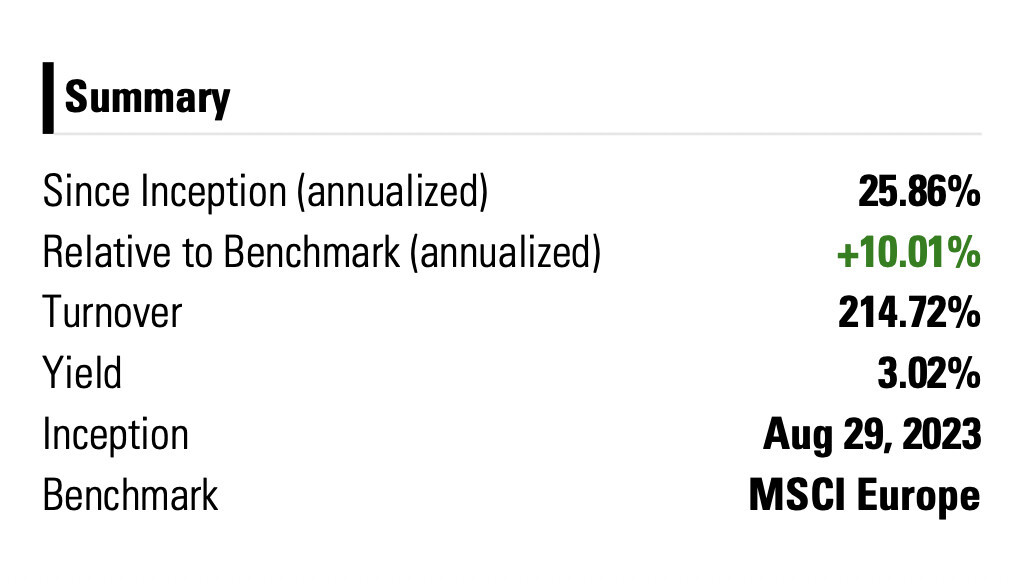

I trade both US/Can and Nothern Europe in the one Universe and with the same strategies. It can be a bit frustrating when noticing that some data is not beeing updated properly and in a timley manner. However, it does not seem the effect the result much for me. I have only been trading live with my P123 strategies for one year and Europe has given me higher returns than US so far (except Finland).

About 26% this year. Been increasing my positions slowly over the year, since Mars I have had about 95% of the capital in that account in the market. I guess on average 40% of my stocks are European. And I do my best to quantify my strategies, so I think I’m holding way more stocks than the average P123 investor, >135