I used the universe mean vs my method and get the same result! Much more succinct. I assume the lambda function will also correctly subtract the universe gains from the stock gains to get the alpha, but I did not check it.

I am personally more interested in a CAGR or alpha as my success method than an R^2 score. Partially because r2 is not intuitive for me in the sense that my model may predict well, but I don’t know what that means in terms of return on investment haha.

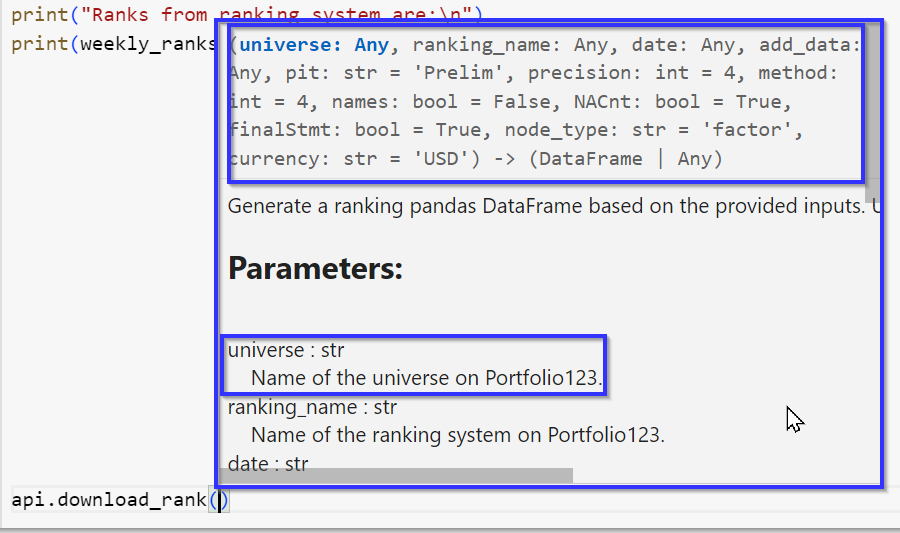

This is actually my full code if you want to run it. I only know it works in colab, but probably should locally as well. Also I used a class so running the individual functions is a little different, but it makes adding the inputs easier. Also if you use a decent editor for python code it will give you prompts as you type in the input. Dan and Portfolio123 the doc strings would be a nice update for the python api if you are ever doing one!

Note you have to go to the bottom of the long post to see the examples. I tried an expanding section, but it messed up the code…

# NOTE: Google Colab uses Python 3.7

!pip install --upgrade p123api # Install p123api if missing

import p123api

import pandas as pd

from datetime import timedelta, datetime

class Portfolio123API:

def __init__(self, api_id, api_key):

self.client = p123api.Client(api_id=api_id, api_key=api_key)

def rank_update(self, xml_str, type='stock', method=4, currency='USD'):

"""

Update or create the ApiRankingSystem using provided XML string.

Parameters:

-----------

xml_str : str

XML data containing ranking information to be updated. Like from the ranking text editor.

type : str, optional

Type of ranking data, e.g., 'stock' or 'asset', default is 'stock'.

method : int, optional

Numeric code representing the ranking update method, default is 4. 2-Percentile NAs Negative, 4-Percentile NAs Neutral

currency : str, optional

Currency for monetary values, default is 'USD'.

Returns:

--------

bool

Returns True indicating the successful update of rankings.

"""

self.client.rank_update({

"type": type,

"rankingMethod": method,

"nodes": xml_str,

"currency": currency

})

return True

def download_rank(self, universe, ranking_name, date, add_data, pit='Prelim', precision=4, method=4, names=False, NACnt=True, finalStmt=True, node_type='factor', currency='USD'):

"""

Generate a ranking pandas DataFrame based on the provided inputs. Uses 1 api credit per 25,000 data points as of Aug 2023.

Parameters:

-----------

universe : str

Name of the universe on Portfolio123.

ranking_name : str

Name of the ranking system on Portfolio123.

date : str

Date for which the ranking is being generated. Format is 'YYYY-MM-DD'

add_data : list

Additional data to be considered for ranking. like 'Close(0)' which is fridays close. Note some things may require the PIT license.

pit : str, optional

Period in time, e.g., 'Prelim' or 'Complete', default is 'Prelim'.

precision : int, optional

Number of decimal places for ranking scores, default is 4.

method : int, optional

Numeric code representing the ranking method, default is 4 which is neutral, 2 is negative.

names : bool, optional

Flag indicating whether to include ticker names in the output, default is False.

NACnt : bool, optional

Flag indicating whether to include the count of missing values, default is True.

finalStmt : bool, optional

Flag indicating whether to include if the stock has a final statement, default is True.

node_type : str, optional

Type of node for ranking, e.g., 'factor' or 'composite', default is 'factor'.

currency : str, optional

Currency for monetary values, default is 'USD'. 'USD' | 'CAD' | 'EUR' | 'GBP' | 'CHF'

Returns:

--------

pandas.DataFrame

A DataFrame containing the generated ranking data. Added the date as a column

"""

ranking = self.client.rank_ranks({

'rankingSystem': ranking_name,

'asOfDt': date, # Formated as 'yyyy-mm-dd'

'universe': universe,

'pitMethod': pit,

'precision': precision,

'rankingMethod': method, # 2-Percentile NAs Negative, 4-Percentile NAs Neutral

'includeNames': names,

'includeNaCnt': NACnt,

'includeFinalStmt': finalStmt,

'nodeDetails': node_type, # 'factor', 'composite'

'currency': currency,

'additionalData': add_data # Example: ['Close(0)', 'mktcap', "ZScore(`Pr2SalesQ`,#All)"]

},True) # True - output to Pandas DataFrame | [False] to JSON.

dates = pd.to_datetime([date]*len(ranking))

dates = pd.to_datetime([date]*len(ranking))

ranking.insert(0, 'Date', dates)

return ranking

def rank_perf(self, universe, ranking_name, start_date, end_date, slippage, pit='Prelim', precision=4, trans_type='Long', method=4, num_buckets=10, minP=3, freq='Every Week', bench='SPY'):

"""

Calculate rankings and return relevant data.

Parameters:

-----------

universe : str

Universe name same as P123

ranking_name : str

Name of the ranking system to be used, should match P123 ranking sys

start_date : str

Start date for the calculation period in the format 'yyyy-mm-dd'

end_date : str

End date for the calculation period in the format 'yyyy-mm-dd'

slippage : float

Value representing slippage for transactions. 0-1

pit : str, optional

Period in time, e.g., 'Prelim' or 'Complete', default is 'Prelim'.

precision : int, optional

Number of decimal places for ranking scores, default is 4. 2-4

trans_type : str, optional

Type of transaction, e.g., 'Long' or 'Short', default is 'Long'.

method : int, optional

Numeric code representing the ranking method, default is 4. 2-Percentile NAs Negative, 4-Percentile NAs Neutral

num_buckets : int, optional

Number of buckets for ranking, default is 10.

minP : int, optional

Minimum stock price, default is 3.

freq : str, optional

Frequency of calculation, e.g., 'Every 4 Weeks' | 'Every Week' | 'Every N Weeks' (2,3,4,6,8,13,26,52), default is every week.

bench : str, optional

Benchmark for comparison, e.g. available benchmarks on P123, default is 'SPY'.

Returns:

--------

df : pandas.DataFrame

A DataFrame containing calculated ranking data.

quota : int

An integer with the remaining quota

"""

results = self.client.rank_perf({

'rankingSystem': ranking_name,

'startDt': start_date,

'endDt': end_date,

'pitMethod': pit,

'precision': precision,

'universe': universe,

'transType': trans_type,

'rankingMethod': method,

'numBuckets': num_buckets,

'minPrice': minP,

'rebalFreq': freq,

'slippage': slippage,

'benchmark': bench,

'outputType': 'perf'}) # only perf with this function

dates = results['dates']

benchmark = results['benchmarkSeries']

buckets = results['bucketSeries']

quota = results['quotaRemaining']

# Scale benchmark

scaled_benchmark = [100 * (value / benchmark[0]) for value in benchmark]

# Create DataFrame

data = {'dates': dates, 'benchmark': scaled_benchmark}

for i, bucket_values in enumerate(buckets, start=1):

data[f'bucket{i}'] = bucket_values

df = pd.DataFrame(data)

return [df, quota]

def download_universe(self, universe, date, formulas, pit='Prelim', precision=4, names=False, currency='USD'):

"""

Generate a pandas DataFrame based on the provided inputs. Uses 1 api credit per 25,000 data points as of Aug 2023.

Parameters:

-----------

universe : str

Name of the universe on Portfolio123.

date : str

Date for which the ranking is being generated. Format is 'YYYY-MM-DD'

formulas : list

Additional data to be considered for ranking. like 'Close(0)' which is fridays close. Note some things may require the PIT license.

pit : str, optional

Period in time, e.g., 'Prelim' or 'Complete', default is 'Prelim'.

precision : int, optional

Number of decimal places for ranking scores, default is 4.

names : bool, optional

Flag indicating whether to include ticker names in the output, default is False.

currency : str, optional

Currency for monetary values, default is 'USD'. 'USD' | 'CAD' | 'EUR' | 'GBP' | 'CHF'

Returns:

--------

pandas.DataFrame

A DataFrame containing the generated ranking data. Added the date as a column

"""

ranking = self.client.data_universe({

'universe': universe,

'asOfDt': date, # 'yyyy-mm-dd'

'formulas': formulas, # ['Close(0)', 'mktcap']

'pitMethod': pit,

'precision': precision,

'includeNames': names,

'currency': currency

},True) # True - output to Pandas DataFrame | [False] to JSON.

dates = pd.to_datetime([date]*len(ranking))

ranking.insert(0, 'Date', dates)

return ranking

def download_weekly_ranks(self, universe, ranking_name, start_date, end_date, add_data, pit='Prelim', precision=4, method=4, names=False, NACnt=True, finalStmt=True, node_type='factor', currency='USD'):

"""

Download ranking from multiple dates. Note that to calculate some additional stats like alpha to the universe some additional date is required!

Uses 1 api credit per 25,000 data points as of Aug 2023.

Parameters:

-----------

universe : str

Name of the universe on Portfolio123.

ranking_name : str

Name of the ranking system on Portfolio123.

start_date : str

Start date to get data. Format is 'YYYY-MM-DD'. Note that the resulting dataframe will use the previous Saturday as the date

end_date : str

End date to get data. Format is 'YYYY-MM-DD'. Note that the resulting dataframe will use the previous SSaturday as the date

add_data : list

Additional data to be considered for ranking. like 'Close(0)' which is fridays close. Note some things may require the PIT license.

pit : str, optional

Period in time, e.g., 'Prelim' or 'Complete', default is 'Prelim'.

precision : int, optional

Number of decimal places for ranking scores, default is 4.

method : int, optional

Numeric code representing the ranking method, default is 4 which is neutral, 2 is negative.

names : bool, optional

Flag indicating whether to include ticker names in the output, default is False.

NACnt : bool, optional

Flag indicating whether to include the count of missing values, default is True.

finalStmt : bool, optional

Flag indicating whether to include if the stock has a final statement, default is True.

node_type : str, optional

Type of node for ranking, e.g., 'factor' or 'composite', default is 'factor'.

currency : str, optional

Currency for monetary values, default is 'USD'. 'USD' | 'CAD' | 'EUR' | 'GBP' | 'CHF'

Returns:

--------

pandas.DataFrame

A DataFrame containing the generated ranking data from one date to another

"""

current_date = datetime.strptime(start_date, '%Y-%m-%d')

end_date = datetime.strptime(end_date, '%Y-%m-%d')

combined_dataframe = pd.DataFrame()

required_data = ['(Open(-6)-Open(-1))/Open(-1)']# This gives a Monday to Monday open gain which is what I trade. Change if you trade another time

while current_date <= end_date:

previous_saturday = current_date - timedelta(days=(current_date.weekday() + 1) % 7) # This calculates a more accurate asofDate

previous_saturday_str = previous_saturday.strftime('%Y-%m-%d')

dataframe = self.download_rank(universe, ranking_name, previous_saturday_str, required_data+add_data, pit, precision, method, names, NACnt, finalStmt, node_type, currency)

dataframe.rename(columns={'formula1': 'MM_gain'}, inplace=True)

# Calculate the universe gain and then each stocks alpha!

univ_gain_percentage = dataframe['MM_gain'].mean() # Calculate the universe return

dataframe['univ_alpha'] = dataframe['MM_gain']-univ_gain_percentage # Calculate the alpha and add to the dataframe

combined_dataframe = pd.concat([combined_dataframe, dataframe], ignore_index=True) # Add it to the dataframe

current_date += timedelta(weeks=1)

return combined_dataframe

Here are the examples for each api function: Make sure to only run the one you want and not all of them or you will burn your credits. Also I did not add them all, just the rank related ones for now.

# Initialize the api class

api_id = 'Your api id'

api_key = 'Your api key'

api = Portfolio123API(api_id, api_key)

#-------------- Examples for each function below -------------------------------

# Update a ranking system ------------------------------------

xml_str = '''

<RankingSystem RankType="Higher">

<StockFormula Weight="0" RankType="Higher" Name="Factor" Description="" Scope="Universe">

<Formula>PEExclXorQ</Formula>

</StockFormula>

</RankingSystem>

''' # this string needs to match the format of the xml string in portfolio123 ranking system

api.rank_update(xml_str, 'stock') # note it will return True if it completes, but otherwise gives no indication it completed

print("API Ranking system updated!")

# Download ranks from a ranking system ------------------------------------

ranks = api.download_rank('Easy to Trade US', 'All-Stars: Greenblatt', '2023-05-04', ['Close(-1)'])

# Note that the (0) date is always the friday before the date given. (-1) is a Monday or the day after the Friday. The date you give does not matter!

print("Ranks from ranking system are:\n")

print(ranks)

# Download data from a universe ------------------------------------

universe_data = api.download_universe('Easy to Trade US', '2023-05-04', ['Close(-1)'])

# Note that the (0) date is always the friday before the date given. (-1) is a Monday or the day after the Friday. The date you give does not matter!

print("Universe data is as follows:\n")

print(universe_data)

# Calculate rank performance ------------------------------------

[perf, quota] = api.rank_perf('Easy to Trade US', 'All-Stars: Greenblatt', '2013-01-01', '2023-01-01', 0.25)

print("Remaining quota is: " + str(quota))

print("Performance plot below:")

perf.plot()

# Download ranks over multiple dates! Includes universe alpha calculated column

# Note that this function adds a universe alpha column that is based on Monday open to Monday open future returns!

weekly_ranks = api.download_weekly_ranks('Large Cap', 'All-Stars: Greenblatt', '2023-07-01', '2023-07-31', ['Close(-6)/Close(-1)-1'])

# Save to a pickle which is very fast to load, but not human readable

weekly_ranks.to_pickle('data.pkl') # This saves the data as a pickle. You can load it using: weekly_ranks = pd.read_pickle('data.pkl')

# Save to a csv, slow to load, but human readable

weekly_ranks.to_csv('data.csv', index=False) # To load it again use: weekly_ranks = pd.read_csv('data.csv')

print("Ranks from ranking system are:\n")

print(weekly_ranks)

Example of the prompts as you type (from the doc strings):

Thanks,

Jonpaul