Thank you Philip and Yuval. Thank you everyone. I am sure there will be a good solution whether it is a lag for earnings estimates, a FactSet data offering etc.

Is there an academic lesson here? Definitely I think.

This suggests that realtime access during the day to analyst earnings estimates would be profitable doesn’t it? After all, [b]the sims–as they are now–are somewhat similar to what one could do with live information isn’t it? Perhaps this is arguable.

And actually this just shows the potential power of realtime information on Monday. What if I could that every day?[/b]

I would love it if during the day I could find out when an analyst downgraded her recommendation or lowered her earnings estimate. I would not need to know which hot new stock to buy—just the dog to unload.

I’m not suggesting that P123 can get into this but if P123 could do that with little expense the sims as they are suggest it might be a game-changer. I’m not sure that P123 could do that at little expense. Anyway, are there any reasonable options for an individual retail trader to get some of this data?

Thank you for any ideas about data on realtime analyst downgrades and lowering of earnings estimates.

My experience (although not 100% certain) is that analyst upgrade / downgrade announcements are like earnings reports - either before open or after close.

EDIT: Just asking around, apparently it can happen during the day although that would be the exception to the rule.

So maybe I could rebalance a port with P123, and before buying a ticker, make sure there is no downgrade showing up before I buy the ticker. Make sure there is no downgrade (or perhaps lowering of the earnings estimate) made before the market open.

Would FactSet include any downgrades made after the market close the day before for sure? Probably I guess but that can be confirmed.

Maybe see if Fidelity or Yahoo updates to an analyst’s downgrade that is made before the open (on the same day) or find a service that does that.

It does not have to be perfect. I can start by not happily buying a dog, oblivious to what has happened since the market close yesterday and remaining in the dark for the next 24 hours.

I am not sure if anyone is interested in this still: although I would not understand why unless you just do not use earnings estimates or analysts recommendations.

I will say all of this has encouraged me. Summarizing: Philip helped me build a sim that I believe in.

Furthermore, the model I showed you is a true machine learning model using factor analysis to determine the weight of the factors in the ranking system (and eliminate overfitting). When we get the improvements in data that Yuval promises, my model is likely to be even better after redoing the weights in the ranking system. Or maybe I will just re-optimize the ranking system using accurate data with P123’s optimizer: that works too.

But can I do better than just following a P123 model blindly? Can I use new data that has come out in the morning before I buy a stock recommended by P123? After all, machine learning is really about finding arbitrage opportunities that do not last forever (not with RT around). It is not magic that does not have a rational explanation.

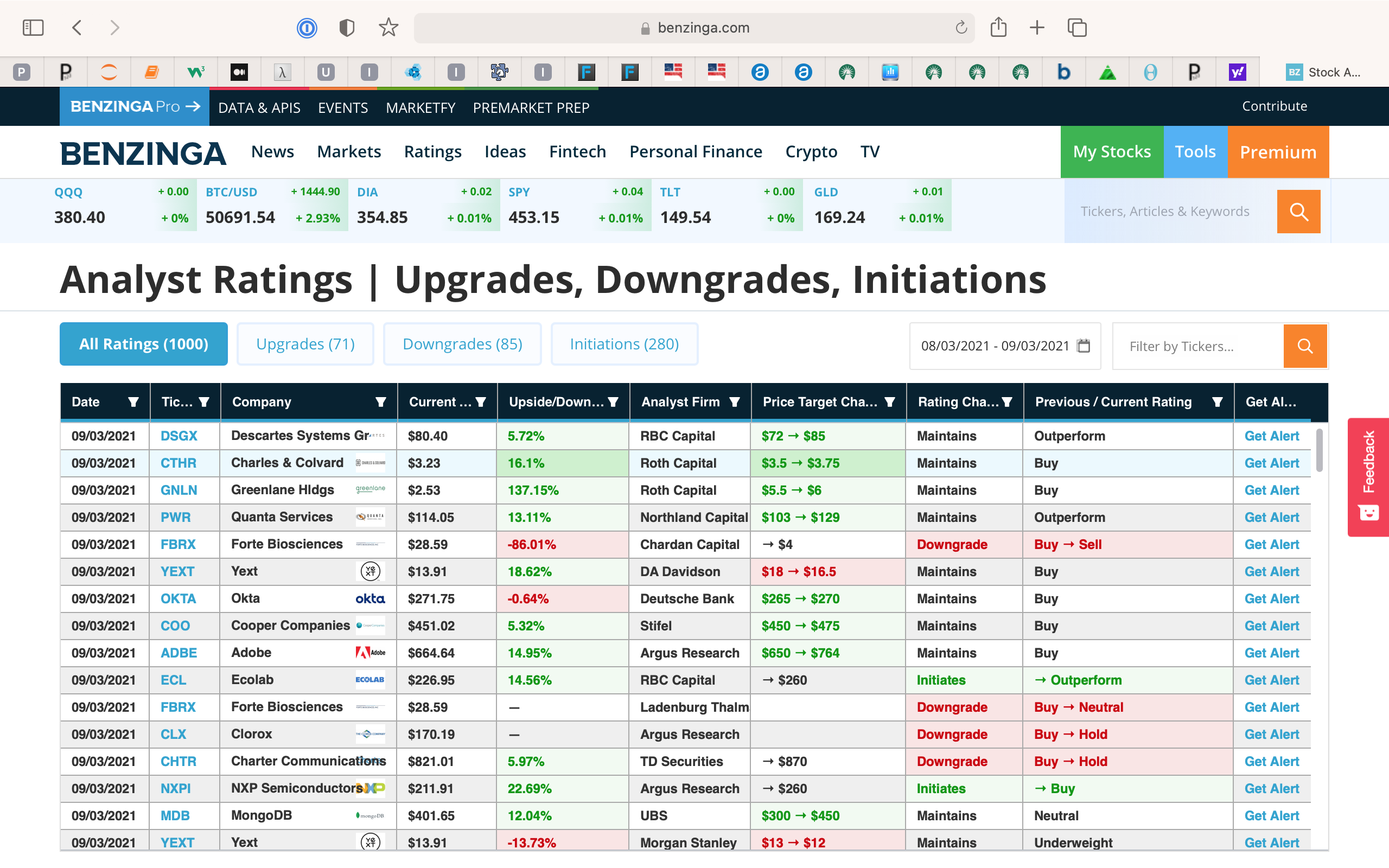

Maybe. For anyone interested, below is a screenshot from Benzinga.com/analyst-ratings. I have not done much with this site yet. But here a 9:17 am on 9/3/21 it looks like I can find some recent data from this morning at this site.

FWIW. Possibly of use for someone who uses analysts ratings and was not already aware of this (or other sites doing this).

You should. Andreas (who uses earnings estimates) owes you too–along with me and many others I think. For sure I greatly appreciate your willingness to go where the data leads you and telling us what you know.

Jrinne: “And actually this just shows the potential power of real time information on Monday. What if I could that every day?”

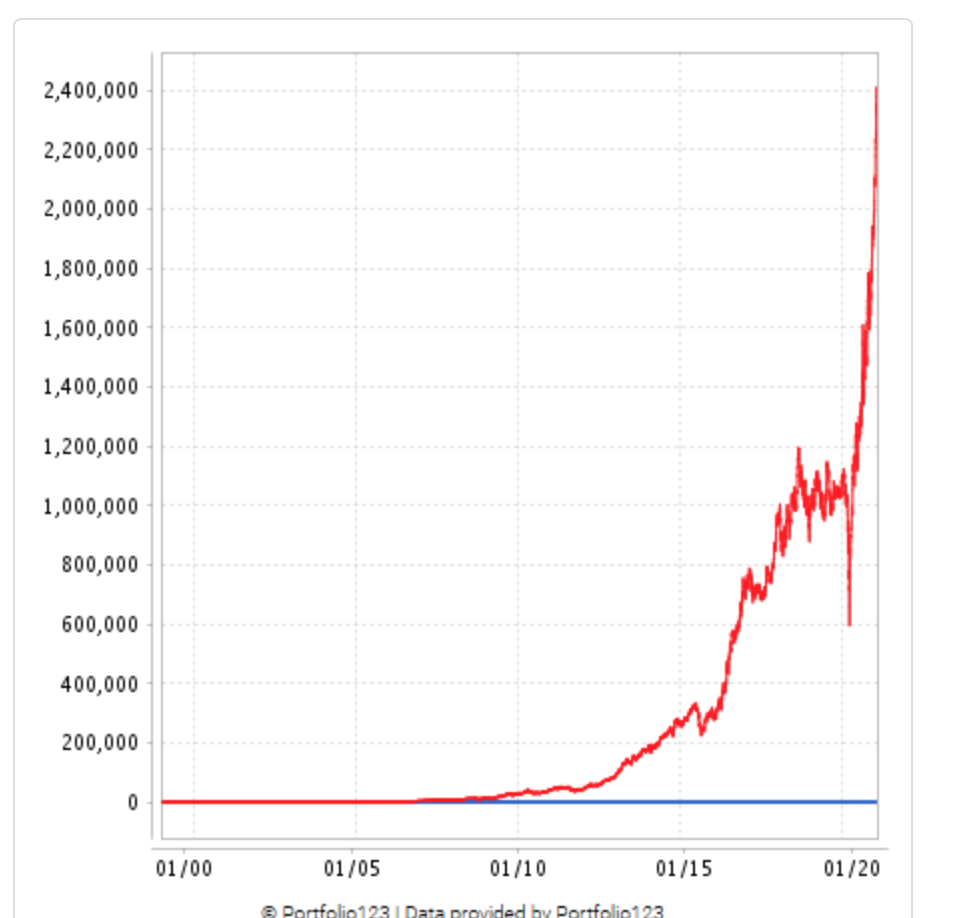

I cannot thank you enough for pointing out your research here, earnings estimates are a game changer. Once again, I had ports around 40-45%, with earnings estimates they go up north 80% (with weekday = 3 north 70%, so still a huge improvement).

I am also in the process of getting a bit more discretionary. I sold SBOW and for example GDP much too early, even they had good earnings estimates momentum (did it better with METC and that saved my performance the last 6 weeks, I had a heavily weight position on this stock) → Depending on the market regime (that is another subject). I will time the exits (and the entries) based on the earnings estimates.

So, if I can get them even in real time (for example with bezinga) that might be a big game changer too (for example in the pre and aftermarket).

The big thing about earnings estimates with small caps is they do not react directly look at GDP, earnings estimates were up, the rank was o.k., and it took days until the pop. Even if they pop (look at SBOW) the reaction is shallow and there is a ton of drift that can be used! It also works on big caps (Nasdaq 100 that is), but not as good as with small caps.

Very interesting is your approach to dynamically change the ranking system based on a ML System (I guess using the API of P123). In academic papers “Factor momentum” is a huge thing now (the biggest academic innovation the last 10 Years in my opinion) and it resonates big with research based on Darius Dale (42macro.com → no BS, everything back tested!). So, changing the factor ranking model dynamically (Based on factor momentum) has a big academic base!

I had a trader friend (a total programming wizard!) visiting yesterday and he does not use P123 so far and I showed it to him. He programmed his own ML / AI (it think based on neural networks) system, but he is struggling with the data (I think he uses data from google), since he can only use price data no fundamental data (google = non pit).

His first question seeing P123 was: Do they have an API and can I use it with my ML Software. I told him, yes and he was very interested.

So, that change (for which Jim and others laid in heavy and I was very skeptical!) makes P123 interesting to that camp of traders.

Thank you for that! We might join forces using my knowledge of P123 and his knowledge of ML. I keep you posted!

Also I thank you for pointing out Bezinga as a source of real time updates on earnings estimates.

You have been very generous in sharing you methods. I am not as generous as you are by nature: although Francois (Quantonomics) correctly points out that I talk (write) too much. I am probably sharing more than I set out to.

But I do have a rational purpose in much of what I share. You correctly point out that–for those interested in earning estimates and analysts recommendations–P123 should probably take every single customer Zacks has away from them. My one reservation is saying this is that I think Zacks rank is automatically PIT the way it is constructed.

Zacks rank is constructed with many similarities to FactSet’s PIT offering–making it PIT if it is constructed as advertised.

We all benefit if any of the discussions lead to an improved platform–including P123, I think. But certainly I do and I do not deny an element of selfishness in my posts. Maybe I will be proved wrong on this but I believe that when P123 can say it is as PIT as Zacks Ranks then the only reason P123 should not be taking over the world would be poor marketing.

As far as sims: I like sims. I like them so much that I found a way to do machine learning to inform me of the optimal sim settings. Not just removing overfitting for good in doing so but getting rid of multi-collinearity and mis-specification. But the backtest is done with a sim and day-to-day my buys and sells are managed–and kept track of–with a port. I like sims.

Anyway, for anyone else who like sims, you can expect me to be on your side if P123 ever tries to cut back on sims. With a wall-of-words in your support.

Anyway, I would love to work with you on this and with P123 or anyone who wants P123 to be widely know as the place to be for Zacks-like sentiment models, machine learning, and anything you could want to do with sims, rank performance tests etc.

That will require a guarantee of some minimum standard of PIT-ness and data quality, I think. Something that P123 is addressing.

Which data update is taken for sims? Sat or early Monday? (This sunday morning the Estimate Revision Data is 1 week old (8/28). Are they regularly updated not until Monday morning?)

Anyway, a sim should use the data which are / were available to every user via his port / screen immediately before the start of trading.

For the port you saw it is run Monday morning after the the full Monday morning update (all data updated including “MON Early Monday Final Weekend Data. Starts 3:00AM”). I think I am pretty good about checking that the data is updated before I rebalance and there are probably no exceptions to this for this port.

BTW, I run the same port every day of the week. Happily, Monday (the one I have shown you) has the median return of all 5 of the ports and it is a fair example. But the underperformance compared to the sim is true of all 5 ports. Making it a little less likely that it is a statistical fluke or a data entry problem on my part.

I don’t know if the last paragraph helps but I hope the first part is a direct answer to you question.

Thank you for your help and interest in this.

Summary of above without a wall of words: There is something wrong with this sim (with variable slippage). AND IT IS NOT OVERFIT IN THE USUAL MEANING OF THE WORD. Most discussion about overfitting make certain assumptions about the data including the assumption that there is no look-ahead bias. As much as I would like to believe it: I am not that good. And the out-of-sample port data supports the idea that I am a humble human after all.

P123 is fixing it I understand: unequivocally a good thing. It needs to be fixed whatever the problem is.

Perhaps, Francois’ post (Quantonomics) woke everyone up and we can just agree: sims with earnings estimates are fiction and wait to see how P123 plans to fix it.

The plan to fix it is pretty simple: we’ll be lagging all estimate data by one day, EXCEPT for today’s estimate data. In other words, the estimate data used for BACKTESTING (in simulations, screens, ranking systems, etc.) will all be lagged by one day so that it’s far closer to PIT. The estimate data you use to decide what to buy and sell today will not be lagged at all.

That’s the plan as I currently understand it (I may be slightly wrong about it, in which case I’ll edit this post). When it has been implemented later this week I will start a new thread about it (in the Announcements forum).

Thank you. That sounds like a good plan. Similar to what Quantopian did if I understand what Quantopian did adequately.

That would mean getting access to historical data from Fridays morning’s earnings estimate data back to 2000 for the sims, would it not? You have access to that data? Moving all the pricing data to Tuesday in the sim seems like a less-than-ideal solution.

You must have access to Friday’s Earnings estimates data. Has to be what you mean unless you think there is a problem with the fundamental data too.

Tnen that would be the perfect solution for getting rid of all look-ahead bias. Either way thank you.